Fourfold increase in death claims against fully underwritten life policies during second Covid-19 wave

Four of South Africa’s largest life insurers reported increases of between 50% and 60% in death claims against fully underwritten new generation individual life policies between March last year, when the first Covid-19 case was recorded in South Africa, and the end of January 2021.

The increase in death claims was revealed by a new dashboard designed by the Continuous Statistical Investigation (CSI) Committee of the Actuarial Society of South Africa (ASSA) to track excess death claims against fully underwritten new generation individual life policies. The statistics exclude universal life policies and limited underwriting policies.

The ASSA Death Claims Dashboard tracks data submitted by four of the country’s biggest life insurers, representing around 70% of South African individual life insurance premiums.

Covid-19 impact on policyholders

Anja Kuys, chair of the ASSA CSI committee, says the aim of the dashboard is to provide life insurers with consolidated insights into the impact of the Covid-19 pandemic on policyholders as measured by excess deaths to help them with accurate pricing of future policy benefits as well as ensuring sufficient capital reserves.

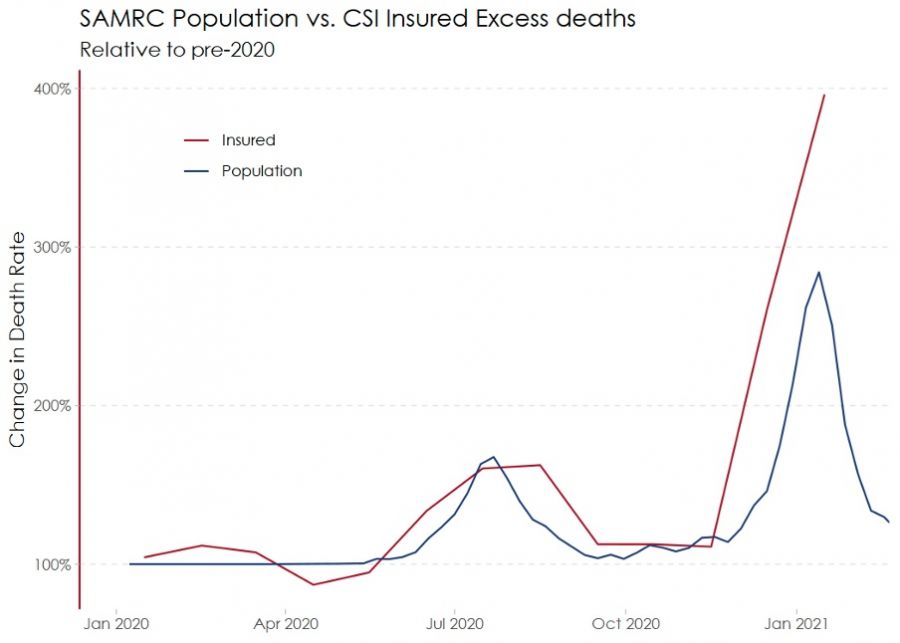

She says the ASSA Death Claims Dashboard shows, for example, that while life insurers had anticipated death claims to increase in line with the national death rate during the second wave, insured lives lost actually exceeded the expected death rate by four times at the peak of the second wave in January 2021. She adds that by comparison the country as a whole saw an increase in reported deaths of 2.8 times the expected death rate.

Kuys says this was a surprise finding given that policyholders with fully underwritten life policies tend to have fewer comorbidities and usually have access to better healthcare. She explains that fully underwritten individual life policies are pure risk products only issued to policyholders who have gone through the underwriting process involving a comprehensive assessment of their lifestyle, health and medical history. She points out that the mortality experience of these policyholders therefore differs significantly to that of the rest of the population. In addition, says Kuys, the death benefit values of these policies tend to be much higher than the benefits offered by funeral or credit life insurance.

“It’s difficult to determine why the change in death rates for insured lives deviated so significantly from the national death rates during the second wave. This does underscore the need for credible statistics that will enable life insurers to accurately price future risk and ensure that they have sufficient capital reserves in place.”

The graph below compares total population deaths (in blue) recorded from 2020 and beyond by the South African Medical Research Council (SAMRC) to the death claims (in red) experienced by four of South Africa’s largest life insurers.

Excess deaths

According to Kuys, the ASSA Death Claims Dashboard provides actuaries with the annualised mortality rate for each month starting from March 2020 compared to an estimate of the annualised mortality rate averaged over 2018 and 2019, providing an indication of excess mortality. This analysis is done separately for deaths due to all causes as well as for natural causes only.

In addition, an analysis is performed based on confirmed Covid-19 deaths as recorded by the contributing companies. Kuys notes that the actual number of Covid-19 deaths is probably higher than what was reported, since death certificates sometimes state the cause of death as “natural causes”, “pneumonia” or “organ failure” even if this was caused by Covid-19.

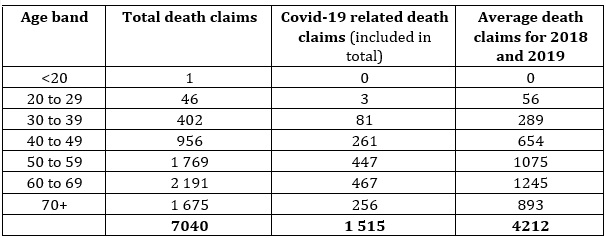

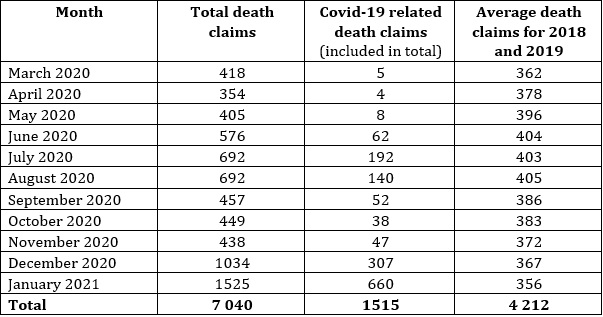

The dashboard shows that in the 11 months between March 2020 and the end of January 2021, four of the biggest life insurers received 7 040 death claims against a total of 1.49 million fully underwritten new generation life policies. Of these claims, 1 515 were for confirmed Covid-19 deaths. South Africa recorded the first Covid-19 death on 22 March 2020.

By comparison, South Africa had recorded 44 509 Covid-19 deaths between March 2020 and the first week of February 2021. Over the same period, however, South Africa experienced 137 731 excess deaths due to natural causes according to research by the SAMRC and the UCT Centre for Actuarial Research. The research estimates that 85% to 95% of the excess natural deaths are attributable to Covid-19.

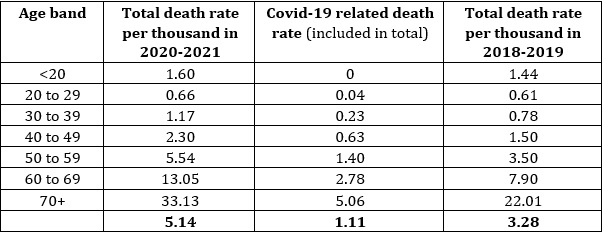

According to Kuys, when compared to consolidated claims averages for 2018 and 2019, the total death claims reported represent an excess death rate of 1.9 per thousand, bringing the total death rate for March 2020 to end of January 2021 to 5.1 per thousand. The average total rate for 2018 and 2019 was 3.2 per thousand, so this means that the number of deaths over the course of the pandemic is nearly 60% higher than would have been expected in a normal year.

Death claims against fully underwritten new generation individual life policies: March 2020 to 31 January 2021

Death claims per age band

Kuys says the dashboard shows an increase in death claims of between 50% and 70% in all age bands above 30 when compared to expected deaths.

According to Kuys, the highest number of Covid-19 related death claims was submitted for policyholders between the ages of 60 to 69 (467), followed closely by the 50 to 59 age band (447 cases). These two age bands also experienced the highest number of death claims between March 2020 and the end of January 2021. Kuys says it is not surprising that death claims in these age bands are higher than for the 70+ age bracket where there are fewer policyholders.

Death rates by age band (March 2020 to 31 January 2021)

Death claims by age band (March 2020 to 31 January 2021)