Navigating the labyrinth of unit trusts

Andriette Theron, Senior Investment Analyst at PPS Investments.

Fifty years after the first unit trust was launched in South Africa, investors now have more than 1500 to choose from. Unit trusts were introduced to make investing in the financial markets easier and simpler for those who aren’t experts in the field. Ironically, with so many different options to choose from, investors are now faced with an even greater challenge of selecting an investment vehicle that would best suit their long term financial needs.

Selecting a unit trust is a complex decision, which involves far more than simply considering the past performance of the unit trust. Even if an individual were to focus on a fund’s performance over ten years (which is considered an adequate period to judge by) it may not give them an accurate picture as there may be pockets of good performance in certain asset classes during that specific period.

This was certainly the case in the South African market over the past decade. Over this period, listed property was the best performing asset class, outperforming equities by an average of 4% per year, while the domestic equity market was mainly pushed higher by a handful of multi-national industrial stocks, led by Naspers.

Unit trusts that had a large exposure to these pockets (property and multi-national industrial stocks) of the market generally performed well. However, this raises the question of whether it is appropriate to assume that the best performing unit trusts of the past will continue to be the best performers in subsequent periods.

Understanding what drove past performance and assessing whether a unit trust is appropriately positioned to benefit from subsequent market cycles is significantly more important than selecting a unit trust solely based on its past performance.

Some unit trusts invest in specific markets or sectors while some invest across a range of different markets. The returns from various unit trusts can differ substantially depending on the risk profile of the unit trust, its investable universe and the investment style of the manager.

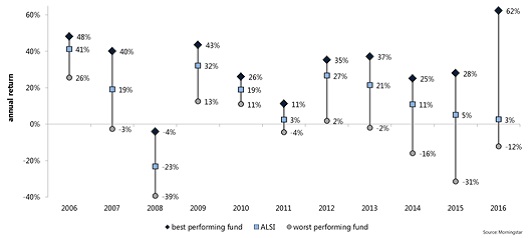

The graph below shows the returns of the best and worst performing South African General Equity unit trusts for each calendar year over the past 10 years. The graph clearly demonstrates that fund selection could have a significant impact on investment returns.

The divergence in the returns of unit trusts could be attributed to a myriad of factors, such as an allocation to global equities (beneficial in periods of Rand weakness), allocation limits on specific shares or sectors, or simply following a particular investment style.

Understanding what drove past performance and assessing whether those factors could also be the main drivers of future performance is critical.

The average person does not have the resources, the time or the willingness to perform a detailed analysis in trying to understand the link between past and future performance and assess the investment risks various unit trusts take to deliver their returns. This is where a multi-manager can add considerable value for both advisers and investors.

When selecting a unit trust, it is important to partner with a multi-manager team of investment professionals that is focussed on analysing and understanding asset managers and their unit trusts’ performance profiles over time.