Is the Active Investment Manager’s Performance Getting Worse?

It is a well-known characteristic of most stockmarkets, that have relatively high degrees of efficiency, for some 70% or so of active managers to fail to beat the performance of a comparable benchmark index, over time. This holds true for the South African equity market as well, which etfSA.co.za and other researchers have pointed out regularly.

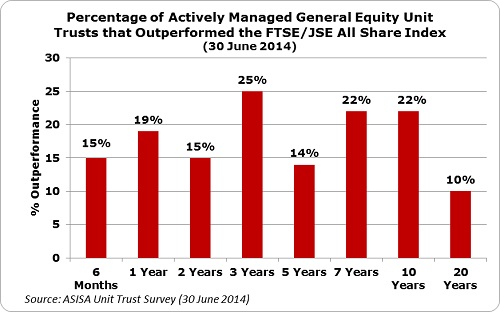

In fact, the case for active managers in South Africa is even worse than the global average. As Chart 1 shows, for the periods ending 30 June 2014, on average, 82% of active unit trust managers fail to beat the target benchmark FTSE/JSE All Share index, over periods ranging from the past 6 months to 20 years.

The reasons for this poor performance by active managers in South Africa is worth a study in itself, but there are some key factors involved.

• The “narrowness” of the SA equity market. 90% of all trades takes place in the top 40 shares on the JSE, so the average return of the market (Beta) is very accessible by purchasing a broad market index.

• The “scalability” of the SA market is a key factor. Outside of the top 40 shares on the JSE, there are few companies with sufficiently large free floats of issued share capital, liquidity and tradability, to accommodate the needs of the top institutional investors. Often value active investors can get “locked-in” to smaller companies that fail to perform or fail altogether.

• “Foreign” investment flows, which play such a large role in the SA equity markets, typically only target the major 10 to 15 shares in the market. These large capitalisation shares therefore make up the bulk of the performance in the market. They also dominate the index weightings. If you don’t hold these “core” shares in portfolios, you run the risk of significant deviation from the index.

• “Closet index tracking” is becoming endemic in South Africa’s institutional investment industry. But if you charge active financial management fees for “benchmark hugging”, you are bound to underperform the market.

But there is even worse news for the active fund managers. The number of active equity unit trust managers that beat the All Share index in the relatively short time periods, of 6 months to 24 months, is getting fewer and fewer.

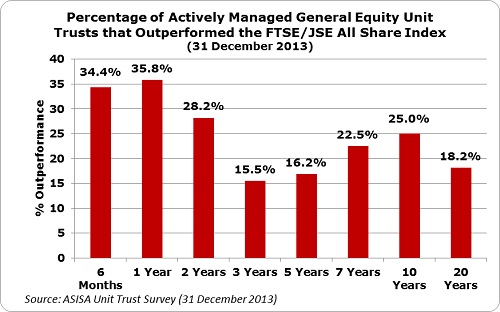

Looking at the outperformance tables, just 6 months ago, for 31st December 2013, 34,4% of active equity managers outperformed the All Share benchmark for the 6 month period; 35,8% for the 12 month period; and 28,2% for 24 months. Only 6 months later, in June 2014, these percentages of active managers that have outperformed over the periods under review, fall to 15%, 19% and 15% respectively. A staggering drop.

Chart 1

If this continues, the relevance of the active managers could be questioned. If Beta performance becomes so accessible through passive index trackers, by definition Alpha, (outperformance of the index) becomes more and more elusive.