Time to Take Interest

Michele Santangelo

When investors contemplate market crashes or bear markets, the narrative is typically around the precipitous fall in the stock market's value.

However, this year has seen one of the worst bear markets in history, but instead of stock markets collapsing, it has been global bond markets. This is out of character for the asset class, which is seen as one with the lowest risk profile. Importantly, the global bond market capitalisation is significantly larger than the world’s stock market capitalisation. The health of bond markets is vitally important to the functioning of capital markets.

Central to this paradigm shift of higher interest rates are the actions of central banks, whose policies have come under scrutiny as economic and financial principles have begun to exert their influence. Since the Global Financial Crisis in 2008/2009, central banks have kept an ultra-low interest rate policy coupled with bouts of quantitative easing and massive increases in money supply during the Covid pandemic. At the peak of central bank stimulus, Japanese and EU bonds traded at negative yields, indicating that investors would pay these governments to safeguard their capital.

High prices and exceedingly low yields have characterised bond markets over the last decade, reflecting the inverse relationship between bond prices and yields. This created an unfavourable asymmetric return profile in a bond market context, setting up bond investors for negligible returns while shouldering significant capital risk. The status quo has persisted for some time, and only since inflation has spiked in the last two years have central banks been forced to increase interest rates to combat inflation. The increase in interest rates has been one of the fastest rate-rising cycles since the 1980s. As such, the price of bonds and other asset classes sensitive to interest rate changes have fallen dramatically while their yields have increased. This has resulted in bond investors taking significant capital losses.

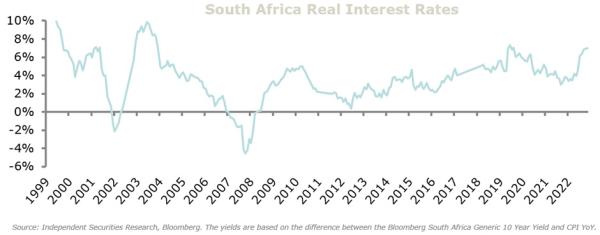

Global interest rates, including those in South Africa, have reached approximately 15-year highs. This escalation increases borrowing costs for governments, businesses, and consumers. Utilising the 10-year government bond benchmark rates as a reference, U.S. bond yields hover just above 4.5%, while South African benchmark rates exceed 10%. The Global Aggregate Bond Index, a proxy for global bonds, has fallen by over 20% from its 2020 peak. Longer-dated bonds exhibit even greater sensitivity to interest rate fluctuations, with the long-dated iShares 20+ Year Treasury ETF witnessing a decline of approximately 45% from its 2020 highs, a noteworthy departure from the traditionally perceived safety of U.S. treasuries.

Higher interest rates are an impediment to economic growth and various asset classes. They are painful but necessary, as the pain of higher rates is usually temporary. At the same time, inflation is far more enduring and devastating, especially for consumers whose incomes rarely recover their purchasing power lost to inflation.

The global investment environment has changed dramatically, but with the seismic shift in interest rates, opportunities have arisen for investors. The trajectory of inflation across developed and emerging markets has moderated. Inflation is declining towards central banks’ target levels, and the probability is high that interest rates have or at least are close to their peak for the current hiking cycle.

The peak of the interest rate cycle has created an investment opportunity for various investors. Investors seeking lower volatility investments with positive real yields (the interest rate less the inflation rate) are now spoilt for choice across the bond and money market spectrum in both a global and South African context. South African government bond investors can now achieve yields of more than 6% above inflation, while real rates in the US are closer to 1.5% above U.S. current inflation rates. This can also be achieved with a margin of safety, given that interest rates have peaked and further pressure on bond prices has abated.

The current yield environment further provides a tactical investment opportunity whereby investors can collect high yields while potentially benefitting from capital appreciation once interest rates begin to fall. Currently, the bond market is pricing in the first U.S. interest rate cut in June 2024, with South Africa likely to follow suit. This setup could produce equity-like total returns for bond investors.

Investors can also explore opportunities in assets that act as bond proxies whose values have also plummeted in conjunction with rising interest rates. Sectors such as real estate stand out where listed real estate values have fallen, and their dividend yields have spiked to historically high levels. As the interest rate outlook improves, listed real estate values are set to recover. Similarly, preference shares will likely react positively to moderating interest rates and disinflation.

Bond markets historically were solely the realm of institutional investors who could deploy substantial capital that would allow them to access the large minimum requirement to buy individual bonds or shorter-term money market instruments. The financial markets have evolved, and many high-yielding securities are available within a retail JSE or global investment account. On the JSE, a wide array of South African bond ETFs are available, with variations in their portfolio composition. Access to global bonds via the JSE is also simple, with a couple of ETFs easily accessible. Global trading platforms are also laden with bond and other fixed-income ETFs or managed funds, with varying composition, duration, and regional exposure. Individual fixed-income securities are also available but do come with minimum investment requirements.

Our conviction remains that equities are the primary vehicle for wealth creation over the long term. However, there are merits of incorporating high-yielding investments into portfolios, particularly when optimising for specific income or risk requirements.