Your portfolio is not the same as gross domestic product

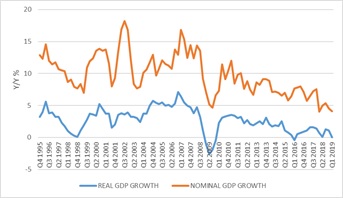

It was much worse than feared. South Africa’s economy contracted at double the rate expected by most economists in the first quarter. The -3.2% annualised decline in gross domestic product (GDP) from the fourth quarter means year-on-year growth was exactly zero. In real (after inflation) terms, the economy is no bigger than a year ago.

Low inflation nation

In nominal terms, adding back inflation, growth was 4.1% from a year ago, implying that the economy’s inflation rate (for consumers and producers) was around 4%. Nominal growth was the slowest since 2009. Nominal growth matters because it reflects the rand growth in incomes and spending. (Real growth gives an idea of the increased purchasing power of those incomes.) The economy’s nominal wage bill only grew 4.4% year-on-year, for instance, and the private sector’s operating surplus (a proxy for company profits) grew by 3.4%. Crucially, it means the government’s ability to generate tax revenue is much lower than thought. The Treasury’s forecast for nominal growth for this year was over 7%. Things would have to improve a lot for that to be realised, or inflation would have to accelerate. Government’s borrowing metrics, the debt and deficit ratios are expressed relative to nominal GDP. A smaller denominator implies higher debt-to-GDP and deficit-to-GDP ratios. Economists are adjusting deficit ratios to 6% of GDP, while government’s debt ratio is likely to breach 60% sooner than expected. All this puts pressure on credit ratings.

Chart 1: Real and nominal year-on-year growth in GDP

Source: Stats SA

Lights out

So what went wrong in the first quarter? Eskom is the main culprit. The Council for Scientific and Industrial Research estimated that the economy endured 770 gigawatt hours of load shedding in the first three months of the year, several times more than the whole of 2018 and half as much as the whole of 2015, the last time we had severe rolling blackouts. Fortunately, the second quarter has so far not seen a repeat. Load shedding clobbered the mining and manufacturing sectors, with the former also impacted by the extended strike at gold miner Sibanye. Fixing Eskom financially and operationally is the number one short-term requirement for an economic rebound.

Consumer squeeze

Consumer spending accounts for 60% of economic activity and is the ultimate driver of local economic growth. It suffered its first quarterly decline since 2016. Compared to a year ago, consumer spending was only 0.8% higher in real terms. While households benefit from low inflation, nominal after-tax income growth has also slowed, so there is almost no growth in real purchasing power. While consumer confidence remains surprisingly robust according to the FNB/BER Consumer Confidence Index, this is primarily a reflection of future expectations, not current conditions. The most recent indicator of consumer spending, May’s new vehicle sales numbers, indicate little appetite for big-ticket spending.

Policy uncertainty leads to low confidence

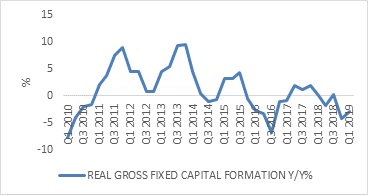

Depressed business confidence and constrained government finances mean fixed investment declined for the fifth consecutive quarter. Fixed investment growth by private businesses contracted for five of the past seven quarters. Fixed investment not only adds to current demand, but also to future productive capacity and a turnaround is therefore crucial for the economy’s growth prospects.

Chart 2: Growth in domestic real fixed investment spending

Source: Stats SA

Businesses invest in plants, equipment, vehicles, IT and more when they want to grow. This requires a sense of optimism about future sales and an expectation that the economy of the future will be well managed, according to consistent rules. A pick-up in consumer spending is therefore necessary, as well as policy certainty from government’s side. This is the main lever government can pull now, seeing as there is no room for fiscal expansion. (Bailouts for poorly managed state-owned enterprises have eroded its fiscal space completely.) Unfortunately, the announcement that the ANC wants to expand the Reserve Bank’s mandate to focus on growth and inflation and that it wants to study “quantity easing” (presumably quantitative easing, or QE) muddied rather than clarified the waters. Land expropriation and the possibility of prescribed assets are similar sources of uncertainty.The announcement, which needs to be seen in the context of the ruling party’s internal political battles, was later refuted by the Finance Minister (a former Reserve Bank governor and staunch defender of its independence) and President Ramaphosa. In any event, changing the South African Reserve Bank’s (SARB’s) mandate is unnecessary as it already explicitly includes ensuring price stability in the interests of balanced growth and development.

Quantitative easing, which involves a central bank buying assets from the banking system by creating reserves (not by printing money, as it is often described), has been tried in Europe, the US and Japan. It primarily aims to combat the threat of deflation, which is not a condition the local economy suffers from. It has had mixed results. Banks mostly did not use the excess reserves to boost lending, because growth in credit requires an increase in risk appetite from lenders and borrowers (which is how money is created). The initial round of US QE was probably the most effective, as it helped remove toxic mortgage-backed securities off banks’ books in 2008. The version applied by the European Central Bank (ECB) was a bit upside down, as it bought more German bonds (driving yields to negative territory) rather than buying the bonds of crisis-hit Greece. Last week’s ECB meeting raised the possibility of restarting QE, a sure sign it did not work the first time. Direct funding of government spending by the central bank is something completely different and has in the past led to hyperinflation, with Zimbabwe and Venezuela being the most recent examples. The Reserve Bank would not allow this as it is mandated by the Constitution to protect the purchasing power of the rand.

Rate cut a possibility

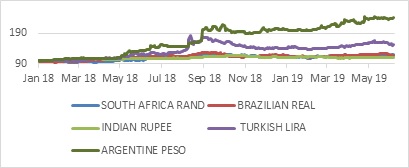

This is not to say that the SARB always gets it right. Interest rates have been too high for some time and it is likely that the shock first quarter growth numbers will mean a rate cut is on the cards in July. Inflation is under control and close to the midpoint of the 3% to 6% target range, and global central banks are cutting. The Reserve Bank of Australia joined the party last week, and reduced its policy rate to 1.25%. Not too long ago it was still talking about rate hikes. The Reserve Bank of India also cut. Similarly, the US Federal Reserve was still projecting several rate hikes six months ago, but its officials (including its Chair Jerome Powell) are now talking about the possibility of rate cuts, given slowing global growth. The market is already pricing in rate reductions. The SARB has correctly emphasised that it cannot address the structural factors constraining economic growth. It cannot generate electricity, for instance. Its scope to cut rates is also not unlimited. But a 1% rate reduction over the next year is feasible – real rates would still be positive - and could ease pressure on consumers by reducing interest payments. A rush of new borrowing in this climate is unlikely. Ironically, the announcement of the ANC’s national executive committee (NEC) might raise the hurdle for a cut, as the SARB will be wary of being seen as caving to political pressure. A quick glance at Argentina and Turkey’s currencies over the past 18 months reveals what can happen when the credibility of the central bank of an emerging market is questioned. The SARB’s legal and de facto independence has been one of the reasons why South Africa’s credit rating has not fallen faster over the past few years. It was thankfully never subject to state capture.

Chart 3: Emerging market currencies against the US dollar, rebased to 100

Source: Refinitiv

Your fund is not the same as GDP

With the local economy in the doldrums, and political uncertainty still a reality despite the election, it is tempting to make the argument that investors should externalise their entire portfolios. This would be an extreme reaction and go against the principle of diversification (never mind the tax implications). The point is that a typical South African balanced fund has a much smaller exposure to domestic economic growth (or lack thereof) than most realise. Most already have 30% direct offshore exposure, while the JSE-listed shares tend to be more global than local. The JSE All Share Index actually rose after the GDP announcement, since the weaker rand boosted the JSE’s global shares, and global markets rose. Shares exposed primarily to the local economy have predictably struggled. High local interest rates constrain the local economy, but they are a fantastic source of low- volatility real returns for local investors. While it is important that policymakers in Pretoria act quickly to stabilise confidence for the economy to recover, what matters most for your portfolio happens in Beijing, Washington and New York. The global economy is facing a period of uncertainty (mostly around trade) and slower growth, but this does not imply a repeat of the 2008 global recession. With the benefit of lower rates, lower oil and hopefully a thawing of global trade relations, growth could pick up again later this year into next year. While equity volatility is likely to remain elevated for some time, investors are again being confronted with the prospect of zero to negative real yields in fixed income in the developed world, making reasonable-priced equities attractive even in a moderate growth environment. Emerging markets are also likely to stand out for yield-starved investors.