World Cup special : Which stockmarkets look ‘cheap’?

Duncan Lamont, Head of Research and Analytics at Schroders.

As the world’s football teams have been battling out for supremacy at the World Cup, Duncan Lamont, Head of Research and Analytics at Schroders, says so have the major equity markets been jostling for the position. However, Lamont says that in both cases, results have not gone entirely to form.

While many other markets had been posting double-digit gains in the 12 months prior to the second quarter, Lamont says the UK was a serial underperformer, much like the English football team. “Investors had been left nursing losses. However, in a reversal to the form guide, the UK was the stand-out performer in the second quarter, matching the England football team’s good run of results.”

Paradoxically, Lamont says that concern over Brexit and weakness in the UK economy have helped UK equities by pushing down the value of the pound. He explains that this helps as over 70% of UK-listed company revenues come from overseas, so a weak pound raises their value when converted into pounds.

He explains that a soaring oil price also helped, given the market’s large exposure to the energy sector. “The UK returned close to 10% over the quarter, trouncing the opposition in a similar manner to the English football team’s 6-1 demolition of Panama. None of the US, European, Japanese and emerging equity markets managed to deliver even half that.”

There have been some disappointing performances from emerging market teams at the World Cup (Argentina’s whimper out of the tournament being a particular lowlight) and Lamont says that emerging markets themselves have also had a torrid time of late – down 3.4% in local currency terms, 7.9% in dollar terms over the quarter. “US aggressive tactics on trade have had a major impact.”

Markets

On the football front, Lamont says that fans are being forced to constantly revise their expectations. Before the tournament, he explains that not many would have predicted that at the quarter-final stage, one of Sweden, England, Russia or Croatia would be a guaranteed finalist.

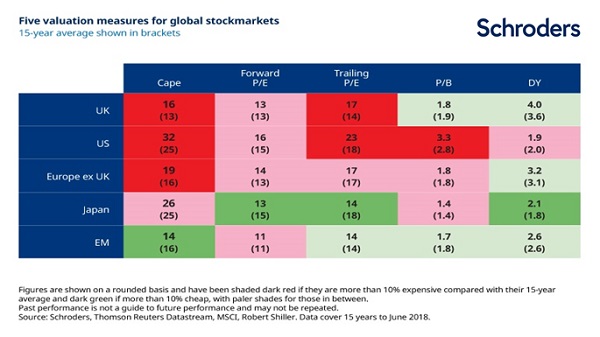

However, he explains that in the investing world, the recent swings have actually had relatively little impact on the relative valuations of global stockmarkets.

“Our valuations show the UK is marginally more expensive than previously and emerging markets are marginally cheaper. But neither by much. Price moves have been broadly matched by changes in fundamentals. There have also been minimal changes to any of the other major markets.”

Lamont says that the US continues to be more expensively valued but also has the strongest earnings growth outlook. “Valuations for European and emerging market equities are close to their 15-year averages so look neither especially cheap nor especially expensive.

“Being cheap on some measures but expensive on others, we have found the UK valuation picture to be as inconsistent as the English football team’s performances at recent major tournaments. The resilience of both will soon be tested.”

He explains that while the UK and European markets look expensive on a cyclically-adjusted price-to-earnings basis over the past 15 years, longer-term analysis makes them look more fairly valued. Japan is the one market which could arguably make a case for being attractively valued.

“However, stockmarkets, as with football teams, do not always perform as expected. History would tell us that the better-rated teams tend to perform better at World Cups, so favouring them is a sensible long-term strategy. However, Germany and Argentina’s poor showings highlight that backing teams (and stockmarkets) that look good on paper does not always work out.

“A degree of humility is warranted. While football fans might find it hard to limit their risk of disappointment by backing several teams to win, investors might be wise to take this approach in their portfolios. Diversifying exposure across a number of countries may lack the excitement and potential gains from backing a single one, but it is also likely to result in less of a fall should one country or region perform badly. Football fans get a fresh shot at glory every four years, but it can take far longer for an investor to recover the losses from a misplaced investment strategy.”