Why the value versus growth debate is defunct

Kyle Wales, Fund Manager at Flagship Asset Management

As the performance gap between so-called growth and value stocks has reached its widest on record, even wider than during the 1999 dot-com bubble, predictions of value’s resurgence have become increasingly insistent.

But Flagship Asset Management Portfolio Manager Kyle Wales believes this debate is a sideshow to what investors should really be considering.

The value versus growth debate centres around the fact that growth stocks have outperformed value stocks for several years, and many are expecting stock markets to enter a period where value-stocks play “catch-up” with growth stocks. Say Wales, “While this ideal is appealing, especially to value investors, I believe there are a number of structural factors why growth stocks have outperformed relative to value stocks, and I don’t see any of these reasons abating in the near future.”

According to Wales, these include:

(1) interest rates are at multi-decade lows, so market participants are using a lower discount rate to value future growth. This means future cashflow streams have a greater value than the yield an asset offers today.

(2) Disruption. Many businesses face shrinking profit pools, while technological disruptors have become the largest stocks in the index. Traditional value investors have not been exposed to these businesses.

(3) Today's global GDP growth is low, altering the growth paradigm from taking advantage of market growth to taking market share from other companies. This has widened the gap in performance between “winners” and “losers”.

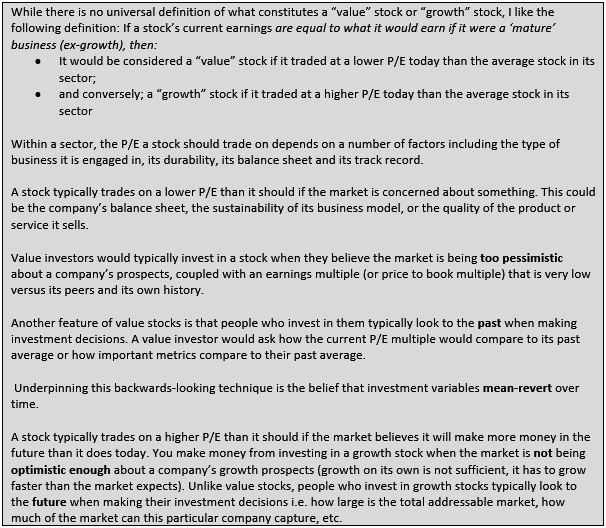

Traditionally, value investors expect to profit when other investors, as represented by the market, are being too pessimistic about a company’s future and that they will revert to their mean. Thus, a value investor would ask how the current P/E multiple would compare to its past average or how important metrics like a company’s margins compare to their past average. Underpinning this backwards-looking technique is the belief that investment variables mean-revert over time.

Wales points out the errors in this thinking. “Mean reverting during the creation of the automobile in the early part of the 20th century would have meant investments into horses, horse and carriage companies, and all their component industries. There are businesses facing similar futures today.”

Wales says another problem with “value” investing today is that the likelihood of buying a “value trap” has increased because of technological disruption and the transition in the growth paradigm from taking advantage of market growth to taking market share.

Instead of dividing the investment universe into “value” and “growth” stocks, Wales believes investors should instead be looking at the individual fundamentals driving each of the stocks in their portfolio as these will ultimately determine how successful they are. “This is especially true when the market as a whole appears expensive and categorizations like “value” or “growth” are becoming less relevant,” he adds.

“We are increasingly seeing index providers attempt to break down their constituents into ‘value’ and ‘growth’ as if it were a factor that can simply be distilled into a group of stocks, rather than a style of investing which is multi-faceted and often complex,” argues Wales.

He notes that a buyer of the MSCI Value Index, for example, is buying Johnson and Johnson on 25x earnings, and Intel on 10x earnings and Walt Disney on 132x earnings. “There appears to be little that draws these businesses together except for the fact that they aren’t growing quickly enough to warrant inclusion into a growth index. How can this form the basis of a sound portfolio?”

For Flagship Asset Management, these buckets of ‘growth’ or value’ don’t work at all, says Wales, and he believes that investors can make money both in “value” stocks and “growth” stocks. “If we use our portfolio as an example, in 2020 we made money both in stocks like Capri (owner of Michael Kors), which traded on 5X earnings at its lows, and delivered returns to us of 140%, as well as Zalando (a German online fashion retailer), which traded at very high multiples but still has many years of growth ahead of it, and delivered returns of 120%.”

Wales describes Flagship’s investment philosophy as valuation-based and says the portfolio managers invest in businesses like a business owner would, looking at its products and services, its culture, competitive advantages, its track record and its financial statements. “We believe that in the long run, earnings drive share prices, so we spend a lot of time understanding the earnings trajectory of the companies we own. The rate of growth is a part of this research process, as is the P/E multiple placed on the stock.”

As bottom-up stock-pickers, by far the most significant factor that has determined whether Flagship is “right” or “wrong” about a stock is its estimate of the growth rate in earnings and how this has compared to the delivered growth rate in earnings per share over time. Says Wales, “Where analysts often go wrong is by placing too much emphasis on their spreadsheet models and not placing enough emphasis on qualitative factors that ultimately drive returns.”

Looking forward, Wales says 2020 was a year in which a rising tide lifted all boats. However, this situation cannot endure forever (although it may endure over the short-term). He recommends that instead of dividing the investment universe into growth and value subsets, investors, even the most amateur of them, would benefit from following the fundamentals of a few great companies, and investing in them with a long-term mindset.