Why the rise in passive investing may benefit active managers

Greg Hopkins, Chief Investment Officer of PSG Asset Management.

Proponents of passive investing advocate low-cost returns, guaranteed to closely match those of the market. In contrast, many active managers globally have had a tough time achieving index returns. Will the next five years be any different?

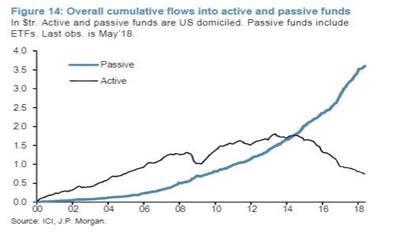

Passive investing has seen a meteoric rise over the past decade, with passive products in the US – the world’s largest passive market – now receiving substantial inflows, while their actively managed counterparts are experiencing outflows (cumulative flows are shown in Graph 1).

Graph 1: Overall cumulative flows into US active and passive funds ($ trillion)*

*As at May 2018. Passive funds include exchange-traded funds.

Sources: ICI; J.P. Morgan

However, the surge in passive strategies has resulted in market distortions.

By its nature, most passive investing is not price sensitive. “We believe that this has contributed to popular, expensive stocks leading the pack in recent years – and in turn, to the tough environment price-sensitive managers have faced,” says Greg Hopkins, Chief Investment Officer of PSG Asset Management.

Market areas that are dominated by passive products are also susceptible to large and sudden in- and outflows, which have the potential to create significant price distortions. Emerging markets are a case in point, and experienced significant outflows in May and June this year as passive portfolios down-weighted exposures on the back of poor emerging market sentiment.

Could the pendulum have swung too far?

Fidelity launched the world’s first zero-fee index funds earlier this month; a move that lends further weight to the case for passive investing and which could spur competitors to follow suit.

“While investors seeking passive products stand to benefit, we would caution – as we always do – that when sentiment or expectations shift too far, there is the risk that results could fall short. Conversely, pervasive negativity often proves to be unfounded,” Hopkins says.

The past five years have not been supportive of price-sensitive active managers, as passive flows have been driving most prices higher. However, Hopkins says that passive market distortions can create opportunities for active managers. “If we look to the next five years, we’re quite positive on the opportunities astute active investors are likely to be presented,” he says.

“We believe that the market distortions passive investing causes create fertile ground for active managers to capitalise on mispricing. Sustained inflows into popular market areas tend to drive the prices of expensive assets higher, while broad shifts in sentiment can result in abrupt and significant outflows that push prices down. This creates opportunities for active managers to sell high and buy low.”

In addition, Hopkins says that in the current environment, passive strategies may pose risks.

“While we believe that passive investments have their place, we would caution that an indiscriminate passive strategy currently carries significant risk, as the bulk of passive capital is being allocated to expensive stocks.”

This is especially true for US-focused passive products, as the US market is currently the most popular (and one of the most expensive) globally, while also being the strongest passive foothold.

“We see far more attractive opportunities in the stocks that are being left behind, and in uncrowded market areas that haven’t enjoyed the benefit of considerable passive flows.”

Given the pronounced impact passive investing has had, Hopkins believes that opportunities for active managers on both a regional and stock-specific basis are improving. But to generate the alpha the market’s so long been waiting for, an active strategy must be sufficiently differentiated from the passive alternative.

“We believe that if we stick to choosing wisely from uncrowded and unloved parts of the markets, our clients will continue to be rewarded with benchmark-beating returns over the long run.”