Why the commodity boom cannot be counted on to see us through tough times

The past 40 years of global order and NATO-enabled peacetime trade have allowed intercontinental supply chains to flourish, facilitating worldwide growth and poverty reduction.

While the US-China trade war, Brexit, and even the COVID-19 pandemic sowed the seeds of doubt in such trade alliances, the Russia-Ukraine war has arguably tipped the scales even further in favour of both domestic protectionism and deglobalisation. Both forces are surely the enemy of low prices and have wreaked havoc in already-disrupted supply chains.

In part due to this trade disruption, global inflation has ventured into an inferno this year – and taken a host of commodity prices along for the bumpy ride as price increases invariably feed each other. In the first half of 2022, the prices of oil, gas, wheat and a basket of platinum group metals (PGMs) had each risen in excess of 60% at their respective peaks. For this, the Russia-Ukraine war alone cannot be blamed. While the war threatened to take two giants of the exporting industry out of the market, the fire of inflation had already been ignited in the last two years – in part by excessive offshore monetary and fiscal stimuli and a phenomenal rise in central bank balance sheets and money supply.

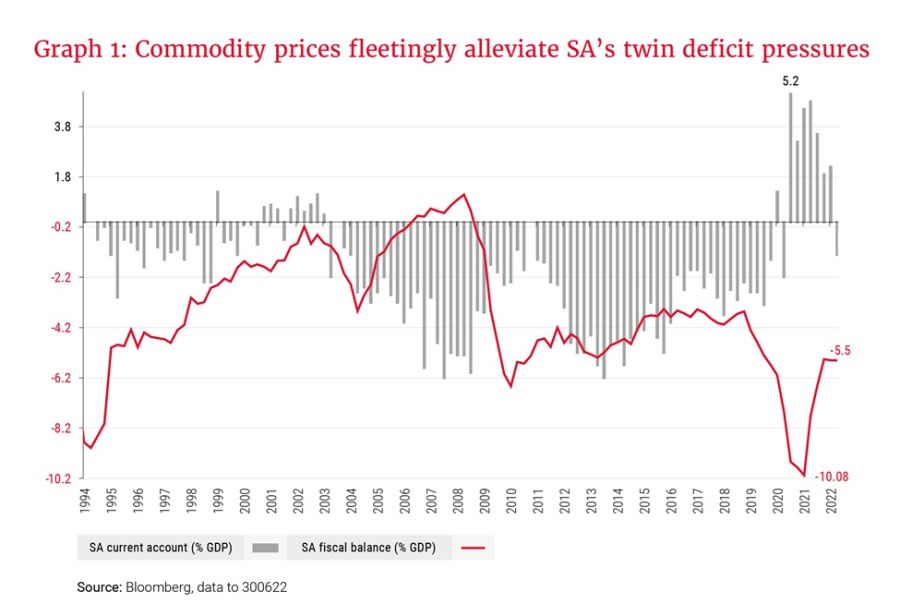

The commodity story has meant that South Africa’s trade balance soared for most of the last two years, as national exports exceeded imports owing to the robust prices of commodities like platinum. This allowed our current account to reach a record high surplus of 5.2% of GDP in 2021, as shown in Graph 1. Strong commodity prices have also provided some fiscal relief to the SA government via a bumper season of corporate income tax collections from SA miners and exporters. This additional revenue has resulted in a tightening of our fiscal deficit (i.e., an improvement in the fiscal balance metric measuring government’s spending in excess of their tax revenue), as seen in the same graph.

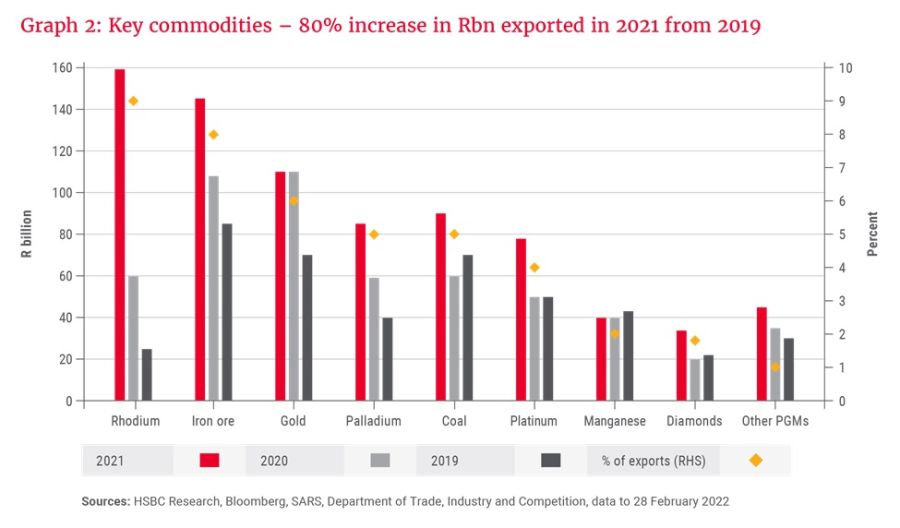

SA’s total exports registered R1.8tn in 2021, representing a 40% increase from 2019. Rhodium suddenly found fame among SA bond investors, who welcomed its price gains as the revenue spill-over lowered government’s borrowing requirements in fixed interest markets.

Within the broader export basket, Graph 2 unpacks the rand value of SA’s key commodity exports of rhodium, iron ore, gold, palladium, coal, platinum, manganese and diamonds in 2021, which registered an 80% increase from 2019. Business is booming – or is it?

The fable and the foibles

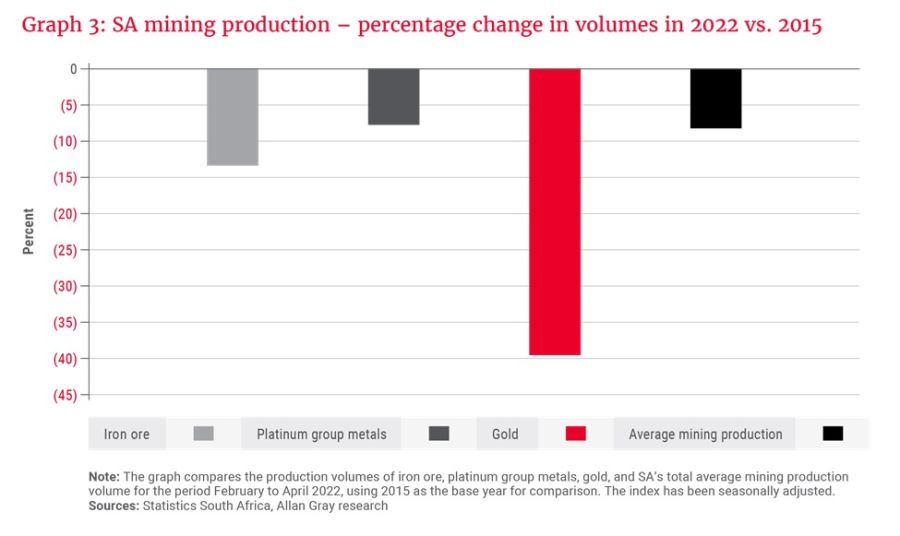

The rand value of exports tells an excellent story, but it neatly banishes another narrative to the footnotes – the story we get when we strip out prices and only look at production and export volumes.

Graph 3 contains the percentage change in mining production volumes in 2022 versus 2015. It is looking far from healthy, recording declines in major categories over the last several years. Loadshedding, strikes and weak port and rail infrastructure are undoubtedly weighing on mining production and also raising the barriers to get contracted volumes offshore. Transnet’s rail network has been crippled by copper cable theft and locomotive failures. The theft of metal and even electricity pylons is well documented by Eskom and Transnet, given the rising global demand for copper scrap and steel. In short, SA cannot take full advantage of the commodity boom.

SA’s largest imports are mineral products (23% of imports – mainly oil) and machinery (20% of imports), followed by chemicals (12% of imports – mainly pharmaceuticals, raw chemicals and fertilisers). Thus far in 2022, an escalation in the price of imported goods is seeing the positive trade balance erode. The rising cost of oil and disappointing mining production volumes have wiped out the current account surplus, taking it from a record 5.2% of GDP to a dismal -1.3% of GDP deficit at the end of the second quarter of 2022. Additionally, the SA fiscus is under enormous pressure due to a struggling municipal model, the growing social requirements for poverty and relief grants, and a structural shortage of energy. The debt of embattled state-owned entities like Eskom will likely need to be taken onto the government’s balance sheet imminently.

Ultimately, debt stabilisation rests on sticking to the spending plan and reducing wasteful expenditure. Fiscal sustainability rests on implementing growth-enhancing reforms and allocating capital to its most productive economic use.

For South Africa, a commodities boom alone cannot work wonders. The heroes in this story can only emerge when they strive to achieve sustainable growth beyond a short-term pricing cycle.