Why don’t I just invest with my bank?

In 10X’s occasional series on understanding the building blocks as you rebuild your wealth, Kelin Pottier, of 10X Investments, answers a question that many investors have asked: Why would I choose to open a tax-free saving account (TFSA) with an asset manager rather than a bank?

The purpose of any tax-advantaged investment product such as a TFSA is to shield an investor from tax on the growth of their investments to maximise investment returns.

Following from first principles, there needs to be growth on investments and that growth needs to be taxable. If there is zero growth on your investment, there is no tax benefit from including such an investment in a TFSA. If there is growth, but that growth is not taxable, there is also no benefit from inclusion in a TFSA.

Thanks to a standard annual tax exemption, South African taxpayers under the age of 65 are allowed to earn interest income of R23,800 per year tax-free (more for those over 65, see below). This means investing in a fixed deposit or interest-bearing account – as you would frequently do with a TFSA with a bank – will receive no tax benefit at all unless the interest you earn exceeds these limits.

To illustrate: Assuming a fixed deposit at a bank pays 4% annual interest, you would need more than R595,000 in savings in order to earn more than the exempt R23,800 interest income.

If you are over the age of 65, this exemption increases to R34,500. In this case, you would need more than R862,500 in savings before you received a cent of tax benefit by including interest-bearing investments in your TFSA.

Therefore, a TFSA invested in interest-bearing investments will provide you a tax benefit only if you are already making full use of your annual interest income tax exemption.

So how should South Africans maximise the lifetime tax benefit of a TFSA?

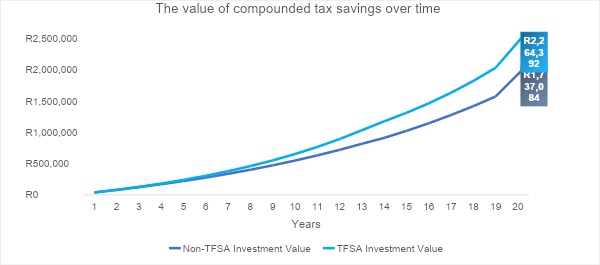

Tax savings increase over time as compound growth is earned on the tax saved. The longer you stay invested, the more tax you save. At the end of 20 years, tax savings account for almost a quarter of the total investment value, resulting in more than half a million rand more in a TFSA.

The example is based on a monthly TFSA contribution of R3,000 for 13 years and 10 months and a final contribution of R2,000 in the 11th month of year 14, when the lifetime contribution limit of R500,000 is reached. Investment in a high equity balanced fund with an annual return of inflation plus 6.5% before fees is assumed. Inflation is assumed to be 4.5%. An equal return split between income, dividends and capital gains is assumed, and a personal tax rate of 45%. Values presented are for illustrative purposes only.

Therefore, investors would be best served by investing their TFSA in a high growth fund, such as a 10X High Equity Index fund or 10X Top 60 SA Equity Index Fund, and remaining invested for the long-term.

As with any investment, one’s objective, time horizon and risk appetite must be considered to make investments that are appropriate and consistent with these factors.

A TFSA is an incredible way to turbocharge your investment growth and rebuild your wealth tax-free.