Who let the dogs out?

The trend of interest rate cuts continued during the month of August. Australia, New Zealand, Indonesia, Mexico and the United Kingdom were among the large economies whose central banks lowered policy rates.

They are likely to be joined next month by the US Federal Reserve, the most important central bank of the lot. It faces a particularly difficult environment. Import tariff increases will put upward pressure on goods prices, though it is uncertain by how much, while at the same time potentially weighing on business activity and household real incomes. In other words, it risks pulling the Fed’s employment and inflation dual mandate in opposite directions. For central banks outside the US, it is a more straightforward story to which they can respond with rate cuts: tariffs will probably reduce exports to the US but not lead to inflation.

There are different interest rates in an economy, depending on the duration of the loan, the nature of the lender and the creditworthiness of the borrower. Picture a dog-walker taking a bunch of canines out to the park. Each dog is on a different length of leash, representing different maturities of rates. The dogwalker is the central bank. The dogs on the short leash will obviously walk right next to the central bank, meaning that short-dated interest rates will track more or less what the central bank wants. The dogs on the longest leashes will vaguely go in the same direction as the dogwalker, but run from one distraction to the other, sniffing everywhere to make sense of the environment. Long-bond yields will have the central bank’s interest rate as a reference, in other words, but also respond to changes in the growth, inflation and fiscal outlook. The farther out in the future we go, the more uncertain things are. Investors need compensation for the fact that today’s interest rate is not going to hold steady for 10 years, and that a borrower’s ability to repay debt might deteriorate.

In the dogbox

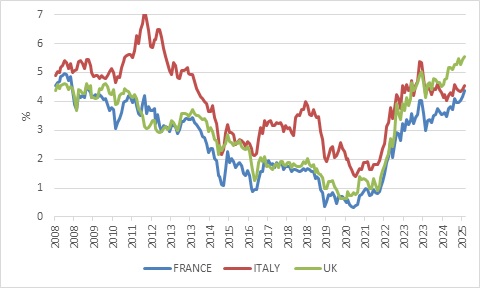

Despite the current and expected interest rate cuts by central banks, long bond yields have increased in several important countries. France is a case in point. The sharp increase in its long-bond yields – despite European Central Bank interest rate cuts over the past year – is mainly due to concerns over its fiscal sustainability. The prime minister faces a confidence vote in Parliament next week, and should he lose, which seems likely, it will be a major setback for efforts to narrow the massive 5.8% of GDP budget deficit. France has the third-highest debt-to-GDP ratio in the Eurozone at 113%, behind only Greece and Italy.

Chart 1: 30-year European government bond yields

Source: LSEG Datastream

Its 30-year bond yield now trades within a whisker of Italy’s, the smallest gap in 25 years. While Italy still has a higher debt ratio, it has made efforts in recent years to stabilise things by running a primary surplus, meaning that tax revenues exceed non-interest spending, the first step in stabilising debt levels. France still runs a primary deficit.

The United Kingdom also runs a primary deficit, though it is smaller than France’s. The UK’s 30-year bond yield has also increased in recent weeks despite a Bank of England rate cut. It has been hovering around 5.6%, close to a 27-year high. Britain’s fiscal problems are largely due to slow economic growth, worsened by the 2016 Brexit vote. As in France, stabilising government borrowing levels is politically tough, since it requires a combination of higher taxes and spending cuts against the backdrop of an ageing population.

Unlike France, British inflation has been sticky of late, limiting the room for the Bank of England to cut interest rates.

Japan’s long-bond yields have also been grinding higher, but for different reasons, and with a very different backstory. Japan has the highest debt-to-GDP ratio of all, but this has been the case for a long time. The driver of the rising yields over the past three years is the central bank raising interest rates, unlike in other developed countries. The Bank of Japan is moving very gradually, having only hiked three times, but it is moving nonetheless since it appears that inflation is finally becoming entrenched after three decades of hovering around zero.

Japan is probably the largest funding source for carry trades, where investors borrow cheaply (virtually for free) in Japan and invest elsewhere where prospective returns are higher, including in foreign equities but largely in higher-yielding currencies. As Japanese short-term and long-term interest rates rise, these carry trades could come under pressure. There was a major market wobble in August last year that was blamed on such an unwind though the spike in risk aversion proved short-lived.

The Big dogs

Then there is the US, where expectations for interest rate cuts have been ramped up due to the Trump administration’s pressure on the Federal Reserve. While the Fed was likely to lower rates somewhat anyway, by mid-next year the institution’s policymaking body will likely be staffed by several Trump-friendly officials, including Jerome Powell’s replacement as chair. Though this will not necessarily lead to a dramatic reduction in interest rates, the marginal decision is likely to be made in favour of easing.

Despite the market pricing in 120 basis points of cuts by December next year, the 30-year US Treasury yield is still hovering near 5%. If Trump’s intention with his pressure on the Fed is to lower the US government’s borrowing costs, it is not working. The fiscal position of the US was already worrying before Trump took office, but his tax-cutting agenda (the One Big Beautiful Bill Act) will make things worse, even if additional tariff revenue will help somewhat. The US government will be borrowing trillions in the years ahead, adding to the $37 trillion already outstanding.

The government borrows in the bond market, not at the Fed’s short-term rate. Similarly, mortgage rates are linked to the 30-year bond yield, unlike in South Africa where they are based on the Reserve Bank’s repo rate. Corporates also borrow more heavily in the bond market, compared to Europe where they are more reliant on bank funding.

In some countries, in other words, the most important interest rates in the economy are on a short leash. In the US, they tend to be on longer leashes. This was helpful when the Fed aggressively hiked interest rates in 2022 and 2023 but means that rate cuts might have less of an impact now.

Higher yields have historically led to a stronger dollar. The past few months have seen the dollar fall instead, even though economic theory predicts that a country imposing high tariffs would see a stronger currency. It seems that concerns over US government debt, Fed independence, institutional strength and the rule of law in general is showing up in the foreign exchange market too.

Click here to read more...