Where does the buck stop?

Dave Mohr Chief Investment Strategist at Old Mutual Multi-Managers

Izak Odendaal Investment Strategist at Old Mutual Multi-Managers

A frequent topic of both serious investment commentators and some of the darker corners of the internet is the future of the US dollar as the dominant global currency. While some believe its decline is imminent (and has been for many years), evidence suggests that it is still very much in a dominant position. As the US Federal Reserve (the Fed), the ultimate guardian of its price and purchasing power, is about to cut interest rates, the debate is topical again.

Reserved

Exactly 75 years ago this month, the Bretton Woods conference resulted in a global fixed exchange rate regime that saw most currencies pegged to the dollar, and the dollar was pegged to gold. This was a direct outcome of the relative economic and military strength of the US after the World War. This system ended in 1971, and most currencies float freely today, but the dollar remains the “reserve currency” of the world as it is the first choice of central banks, accounting for two-thirds of global forex reserves.

The dollar’s importance in global trade and finance goes far beyond this, and largely derives from the size of US capital markets. US equities account for half of global market capitalisation according to MSCI, while the US economy is only a fifth of global GDP. The dollar accounts for 60% of international debt and 80% of foreign exchange turnover, according to the Bank for International Settlements, the central bank for central banks. Most commodities, from gold to oil, are priced in dollars. Research from the International Monetary Fund’s current chief economist, Gita Gopinath, has also shown that most global trade is conducted in dollars. For instance, even though only 6% of Turkey’s imports are from the US, 60% of its trade is invoiced in dollars. She also notes that non-US banks hold as much dollar deposits as US banks (about $10 trillion), while corporates outside the US borrow more in US dollars than any other currency. Many economists have argued that the US government enjoys an “exorbitant privilege” because of the status of the dollar since it can borrow more cheaply, and is less constrained by the need to balance its books. Moreover, in a crisis, the world turns to the dollar. We saw this in 2008 when, even though the US was the epicentre of the 2008 credit crunch, investors fled to the safety of the dollar. Gold’s supposed safe-haven status was downgraded.

Chart 1: Real trade-weighted US dollar

Source: Refinitiv Datastream

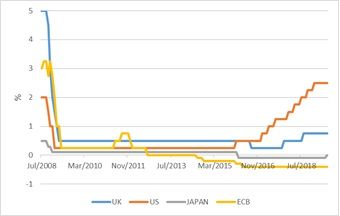

The above factors provide structural support for the dollar, but it has also been strong on a cyclical basis since 2011. Chart 1 shows the US currency relative to a basket of its main trading partners, adjusted for inflation. Since President Nixon broke the gold peg in 1971, there have been three big cyclical bull markets, including the current episode. The reasons behind the strength or weakness of a currency are multifaceted, since people buy or sell it for different reasons: importing, tourism, hedging or simply for speculation. The dollar rally since 2011 is broadly ascribed to the strength of the US economy relative to its trading partners (particularly the sclerotic Eurozone), which in turn gives rise to higher interest rates. The Fed’s policy rate is almost 2.5%, while that of the Bank of England is 0.75%, the Bank of Japan’s is -0.1%, and the European Central Bank’s is at -0.4%. In theory, an investor can earn a decent spread borrowing in Europe and Japan and buying dollars (known as a carry trade).

Chart 2: Central bank policy interest rates

Source: Refinitiv Datastream

This picture might now be changing, as the Fed aims to reduce rates to pre-empt a slowdown. Though US interest rates would still be higher than in Europe and Japan, the fact that the gap is likely to narrow instead of widen reduces carry trade support for the dollar. One vocal individual who would welcome this is US President Trump, who has frequently bemoaned the strength of the buck since it renders US exporters less competitive, while US companies have to contend with cheaper imports in their domestic markets. (Ironically, the tariffs he has slapped on imports in response have only served to strengthen the dollar further.)

Slow structural decline

Taking a longer-term view, the role of the dollar is likely to decline over time but not disappear. Central banks are expected to continue diversifying their reserves, but as long as their economies have dollar liabilities, it makes sense to have dollar reserves. Another frequent argument is that investors will eventually lose trust in the dollar because of persistent current account and budget shortfalls (the “twin deficits”). After all, money is all about trust, and you and I and everyone else believe this metal token or piece of paper or digit on a computer screen denotes a certain value and can be freely exchanged for goods and services of that value. It is one of the great social conventions that makes modern civilisation possible. Trump’s tax cuts have further widened the budget deficit, and his trade wars are unlikely to have any success in narrowing the current account deficit, which is largely the mirror image of investors’ demand for US assets. But apart from a few years in the late 1990s, the US government has run budget deficits persistently since 1974. So it is also not clear why the trust will suddenly break. Perhaps when the independence of the Fed, currently under attack from Trump, is fatally eroded.

What is clear is that other countries are taking deliberate steps to de-dollarise. The widespread use of the dollar in global payments gives the US extraordinary power. It basically claims jurisdiction anywhere a dollar is used, even if Americans are not involved. Famously, a New York court fined a French bank $9 billion dollars in 2014 for violating sanctions against Cuba, Sudan and Iran. Most recently, the US unilaterally slapped sanctions on Iran. Even though Europe, India and China do not have sanctions on Iran, companies from these countries cannot import Iranian oil since the US would block them from accessing its financial system. America’s allies in Europe are unhappy about this overreach; its opponents in China and Russia even more so. But they are powerless as long they are all dependent on the dollar. The previous handover of dominant currency status from the pound sterling to the US dollar had the First World War as its immediate reason, but it would probably have happened anyway, given that the US had overtaken the UK as the world’s largest economy and financial sector. China will someday overtake the US economy in size, but China is far away from being the world’s financial leader. It maintains strict capital controls, its markets are not as deep and liquid, and crucially, property rights not as strongly enforced. For this reason, the yuan is still far from being a global currency. A dollar can be spent anywhere in the world, while trying to buy a Coca-Cola with yuan in Bulawayo, Brazzaville or Buenos Aires might get you funny looks. In fact, the ultimate proof of the status of the dollar is that it is the preferred currency in currency black markets globally. For a while, the euro was seen as a credible alternative to the dollar, but the 2011/12 fiscal crisis exposed its flaws, leaving a permanent question mark over its future.

What about the crypto-currencies? Bitcoin has surged again this year, but the fact that its value is expressed in dollars says it all. At any rate, Bitcoin and its peers cannot be thought of as proper currencies, since they are too volatile, and are mostly instruments for speculations (with the ability to buy stuff a side benefit). The Facebook-led new digital currency, Libra, promises to solve some of Bitcoin’s most obvious shortcomings (it is pegged to a basket of currencies). But it has been almost universally criticised, and not only because of Facebook’s poor reputation for managing its members’ data. The lack of a central bank backstop in case of a crisis is one fear (what would happen if millions of people fled Libra at the same time?). The other is the possibility of it being used to hide ill-gotten funds. For this reason, Bank of England Governor Mark Carney spoke for many regulators when he said the Bank would approach Libra with “an open mind but not an open door”. It is very unlikely that any version of private crypto-currencies can replace the dollar. Digital currencies issued by central banks, on the other hand, are more promising, but it would still be the “digital dollar” that starts in poll position.

Down south

What does all this mean for us? Chart 3 below shows that if the US dollar is stronger against other currencies, it tends to be strong against the rand too. A strong dollar implies a weak rand, in other words, which in turn puts upward pressure on local inflation and interest rates. In fact, it is a double whammy, since a stronger dollar tends to put downward pressure on commodity prices too, South Africa’s main exports. However, since South African companies and investors have substantial foreign assets, a weaker exchange rate increases the rand value of these assets.

Chart 3: Rand-dollar exchange rate and US dollar index

Source: Refinitiv Datastream

A short to medium-term cyclical decline in the dollar would likely lead to a firmer rand, ignoring domestic economic and political uncertainty. While nobody expects the rand to surge to overvalued territory (as it was last in 2011), investors in interest-rate sensitive assets would still benefit, while the rand value of offshore assets will come under pressure. However, the rand is never a one-way bet, and it makes sense to be diversified. What a long-term decline in the dominant status of the dollar means for local investors is uncertain, but based on current trends, it is not something that is likely within the next few years.