When will growth make a comeback?

Gerrit Smit, Head of Equity Management at Stonehage Fleming

Gerrit Smit on the great style rotation

The much reported ‘great rotation’ towards value investing this year has seen investors drastically reduce their positions in growth stocks – those companies expected to grow sales and earnings at a faster rate than the market average. As manager of a growth fund, Gerrit Smit has “felt the same pain”. Nevertheless, he believes there are some early signs that value’s most recent good relative run may not continue for long.

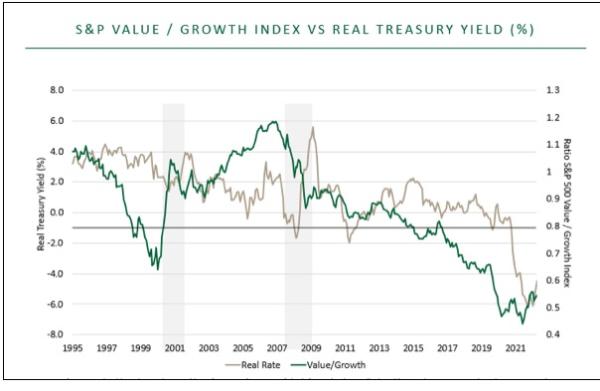

“The correlation between the relative value/growth index and the real treasury yield (see Chart 1) clearly demonstrates value’s ‘need’ for positive real rates”, he told guests at a Now and for future generations webinar, hosted by Stonehage Fleming recently.

Chart 1

Source: Bloomberg. Stonehage Fleming. October 2022*

“In the period between 2001 and 2007, real rates were positive and value had a relatively longer period of outperformance,” noted Gerrit, who manages a concentrated, high conviction portfolio of 20-30 best in class holdings in the Stonehage Fleming Global Best Ideas Equity Fund. “Currently, however, real rates are in deeply negative territory. As inflation drops, that may change but it is likely to take quite a while before it goes back into high positive levels. That’s a situation which, I would argue, rather favours the growth style of investing.”

Furthermore, Gerrit argued, the continuing period of economic weakness may also prove to be a more positive environment for growth than for value stocks (see Chart 2). “During times of low economic growth or even a recession, growth becomes more difficult to achieve on a sustainable basis. The result is that companies that continue to grow during a downturn outperform value as investors are then more willing to pay more for it on a relative basis.”

Chart 2

Source: Bloomberg. Stonehage Fleming. October 2022*

A look at the three previous US recessions bears out this theory. “In all the three most recent recessions, growth stocks’ outperformance has come out at about 20%. Should that happen again, (and odds for a recession are growing), growth managers may catch up materially, and their shorter-term track records be restored.”