What to Worry About

Every now and then markets hit a serious wobble that forces the question: What is going on? And what should we do about it? The past week was one of those occasions.

Geopolitics and politics

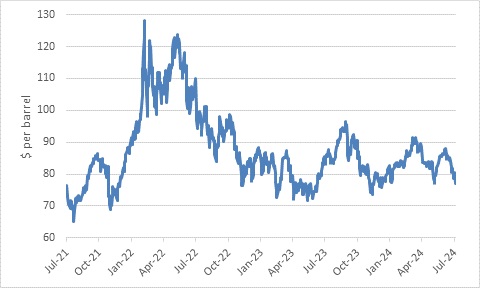

It was a week where Russia launched a massive drone attack on Kiev, and Israel killed a Hezbollah leader in Lebanon and (allegedly) a Hamas leader on Iranian soil. While the war in Ukraine seems to have ground to a bloody stalemate, the fear of an escalation in the Middle East remains real. Wars are tragic and doubly as people in other parts of the world quickly forget about them when they are not directly impacted. This conflict affects the oil price which can impact the global economy negatively. However, it remains within its trading range of the past few years and does not pose a big risk at current levels.

Chart 1: Brent crude oil price

Source: LSEG Datastream

Recession risks reappear

While politics and geopolitics hog the headlines, the biggest concern of any investor with an equity-heavy portfolio is a global recession, more specifically a US recession. (US equities make up 60% to 70% of global equity market capitalisation.) In a recession, company profits fall, which drags share prices lower, but the market also usually suffers a multiple contraction. In other words, not only do earnings fall, but the price: earnings ratio also declines. People lose their jobs and must sell their most liquid investments to make ends meet. The dollar also tends to strengthen in a flight to safety, which further depresses non-US returns. With one exception (1987), the major global equity bear markets of the modern era have coincided with recessions in the US.

Unfortunately, despite the best efforts and collective brain power of thousands of economic forecasters worldwide, spotting recessions in advance remains a tough job. And as per the punchline of many a joke, put five economists in a room and you will likely end up with six or more predictions. One of the reasons recessions are so feared is because they often appear unexpectedly.

The best we can do is to see if the conditions that gave rise to a recession in the past are present today. A simple way of thinking about it is that the bigger the party, the more severe the hangover. Often when economies experience rapid growth, all kinds of imbalances build up that are prone to a vicious reversal. This usually means households taking on too much debt to fund their lifestyles and companies overinvesting for a rosy future that never materialises. A real estate boom is often at the heart of such problems. In the case of developing countries, the problem is often that hot money flows in during the good years and fund unsustainably high levels of imports. When the hot money leaves for whatever reason, these countries find themselves desperately short of hard currency and the economy is forced into contraction. (Similarly, when a particular trade becomes very popular among investors, it is also prone to a violent reversal. If everyone sits on one side of a canoe, it can tip over. That seems to be the case with the sharp rally in the Japanese yen and decline in Japanese stocks following Bank of Japan’s rate hike).

Back to the present, US household and company balance sheets are generally in good shape and there has been little by way of reckless private borrowing. This is a source of strength. Confidence surveys, for example, have remained subdued, not pointing to a mood of excessive risk-taking on the part of consumers and companies.

However, there are pockets of weakness in the US where high interest rates have really put on the squeeze, however, notably smaller businesses, commercial real estate, and low-income households. Manufacturing has also been soft, and the latest data points to fresh weakness in the US and elsewhere.

The main concern is that American job growth slowed notably in July, with only 114,000 jobs added, below expectations. Moreover, the unemployment rate ticked up to 4.3%. While still low, it has increased in recent months. Wage growth slowed to below 4% year-on-year. The labour market is clearly cooling (“normalising” is probably a better description, following pandemic and aftershocks) though the current pace of growth can still sustain a decent, if slower, expansion in consumer spending. Moreover, the labour market is increasingly unlikely to be a source of upside inflation pressure, i.e. a wage-price spiral. The big question is whether it goes from cooling to cold. Rising joblessness would put pressure on consumer spending, which would in turn lead to companies cutting jobs to preserve margins. Things can snowball quickly.

Click here to read more...