What to do when you don’t know what to do?

Roné Swanepoel, Business Development Manager at Morningstar Investment Management SA

The answer is simple: stay the course

In the words of Peter Lynch two years after the March 2020 Covid crash - “More money has been lost in crises trying to predict what is going to happen than actually in them”. As with all things unknown and uncertain, it is human nature to speculate how things will pan out. Although we have no actual control over the outcome, being mentally prepared for a certain outcome brings some sort of comfort – especially when it comes to our investments.

For most of us, success in difficult markets look a lot more like survival - surviving our own behavioural mistakes, avoiding timing the market and staying invested. Investors often hear that they should tune out the noise and not pay attention to market turbulence and panicked news headlines. This is a lot easier said than done when it comes to your hard-earned money.

What should we do, when we don’t know what to do?

1. Remember cash rarely outperforms over the long term

As investors, we are intrinsically loss averse which, simply put, means we hate losses more than we love gains. When markets are turbulent, we often see investors struggle with the “fight or flight” physiological response. Investors are left to choose between staying invested amid the volatility (i.e. fight) or fleeing (i.e. flight) to safe-haven assets and cashing out their investments. More often than not, the latter path is taken.

Global markets have proved to be brutal as we tiptoe into 2022. US equities (in real terms) are on course for their biggest annual loss since 1974 and global bonds have experienced their worst month in history (in April 2022). Investors are rightfully fearful and considering the safety that cash could provide.

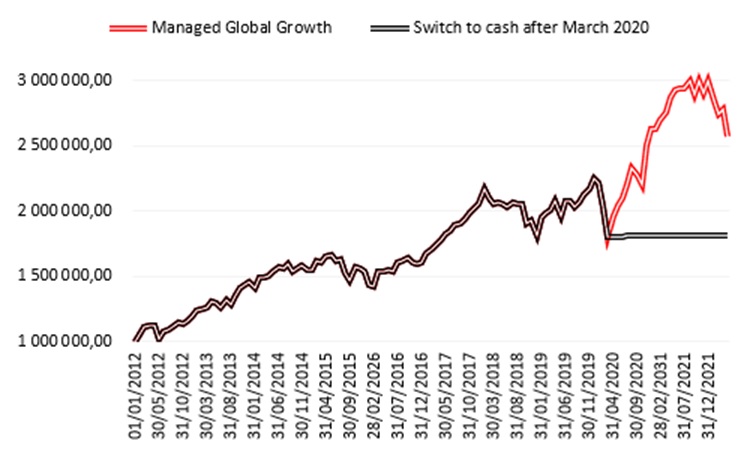

During March 2020 the global market fell by -13,23%[1] ( versus a -8,31% drawdown in April 2022). The below chart illustrates the path of an investor who invested $1 000 000 in the Morningstar Global Growth portfolio (a portfolio consisting predominantly of global equity) 10 years ago.

We considered two scenarios –

a. Staying the course: If the investor had stayed invested in the Morningstar Global Growth portfolio throughout the March 2020 drawdown; versus

b. A dash to cash: If the investor decided to disinvest from the portfolio and move the investment to cash.

There’s an adage among investors during market downturns: “Don’t catch a falling knife[2]”. Using cash as a flight mechanism when things get tough is detrimental to long term portfolio returns.

In this example, a panicked dash to cash would have resulted in a difference in ending value of more than $700 000.

Exhibit 1 | Dash to cash versus staying invested

Source: Morningstar Direct, data as at 30 April 2022. Past performance is not an indication of future results. For illustrative purposes only.

2. If you decide to dash to cash – how do you know when to buy back in?

The three most important words when it comes to predicting the future are most definitely “I don’t know”. Time in the market is generally superior to timing the market and even if you time getting out of the market and into cash perfectly, knowing when to get back in can be very difficult.

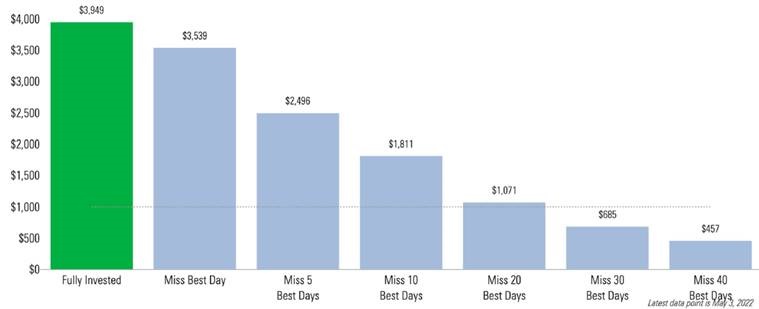

Let’s consider a recent example: at the end of February 2020 we saw the beginning of a historic decline in the S&P 500, the market finally reached the pandemic low on 23 March 2020 and a bear market (a decline of more if 10% in the market) became a reality. Historically, it has been observed that it could take an average of about two years for the market to recover from such a sell-off – except, this time it happened in just 149 days. By the end of August 2020, the index had regained its strength and reached record highs.

So what would have happened if an investor missed the best days? (If an investor was sitting in cash, and didn’t know when to buy back in…)

Let’s look at an example of Investor A who invested $1 000 in the S&P 500, 25 years ago.

If Investor A had left the investment (and stayed the course), it would be worth $3 949 today but had Investor A missed only the best 10 days in the market over the 25-year period, Investor A would be left with just over 50% of what he/she would have had (if the investor stayed invested).

Exhibit 2 | 25 years, initial $1 000 invested, S&P before fees

Source: Clearnomics, Standard & Poor’s. Dara as at 3 May 2022. Past performance is not an indication of future results. For illustrative purposes only.

If history has taught us anything it is that the best days do come after the worst.

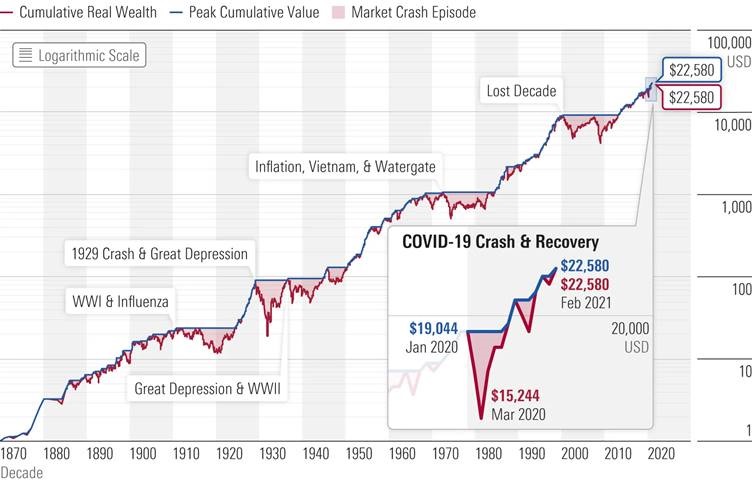

3. Zoom out and consider the long term

Looking at any long-term historical chart of the S&P 500, the performance line climbs over time. Research[3] has indicated that when shown a track history of 1-year returns, investors allocate 10% to equities, however, when shown a track history of 30-year returns, investors allocated 90% to equities.

Long-term thinking can, to some extent, be a deceptive safety blanket that investors assume allows them to bypass the painful and unpredictable short run. Unfortunately, this is very rarely the case. As can be seen in the below graph, it is quite the opposite - the longer your time horizon the more calamities, geopolitical events, inflation scares, tech bubbles, great depressions, financial crises, and disasters you’ll experience.

The graph below illustrates two important points:

a. Despite numerous severe drops, the cumulative wealth line shows that $1 grows to $22,580 over this period of 150 years. In other words, staying in the market and weathering the short-term movements have paid off for investors.

b. The range in shaded areas shows that some declines are worse than others — and how long each will/can last is unpredictable.

Exhibit 3 | Market crash timeline: growth of $1 and the U.S. Stock market’s real peak values

Sources: Data as at 28 February 2021. Kaplan et al. (2009); Ibbotson (2020); Morningstar Direct; Goetzmann, Ibbotson, and Peng (2000); Pierce (1982); www.econ.yale.edu/^shiller/data.htm, Ibbotson Associates SBBI US Large-Cap Stock Inflation Adjusted Total Return Extended Index. Past performance is not an indication of future results. For illustrative purposes only.

In closing - what do you do when you don’t know what to do?

1. Remember that cash has not (historically) managed to outperform equities and bonds over the long term.

2. Returns don’t happen in straight lines, and it seldom occurs when one expects them to, it really is about time in the market and not timing the market.

3. The long term is just a collection of short runs and having a long-term strategy does not exonerate investors from short-term setbacks in markets.

4. It is vital to separate emotion from an investment portfolio. Often the most beleaguered investments turn out to be a great opportunity for future returns, as investors can access these investments at a good price.

5. Volatility creates opportunity and short-term underperformance can translate into a solid, longer-term upside.

The bad news - markets are volatile right now and it’s all being driven by interest rates, inflation, and the fear of a slowing economy. The good news is that very few investors are bullish, and good things tend to happen when most investors think they won’t. Staying the course does not necessarily mean sitting still. It means avoiding bad behaviour, remembering your goals and ensuring your approach is applied with discipline. If your goals have not changed, then your investment strategy shouldn’t either.