What should investors make of this year’s emerging market election results?

Andrew Rymer

While they are just getting underway in developed markets, scheduled elections for 2024 in emerging markets are now complete.

Late May and early June saw a pick-up in market volatility in several emerging markets (EM) in the wake of key national elections – including here in South Africa.

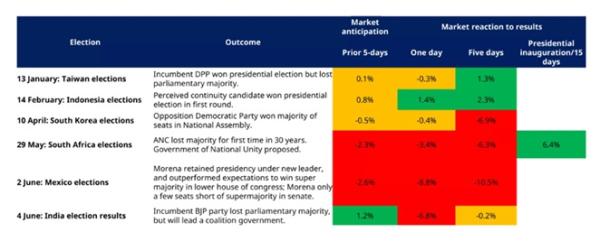

There have been elections held in markets totalling over 50% of the MSCI Emerging Markets index, with mixed results, as the table below summarises. We assess the outcomes, market reaction and long-term implications for policy in these markets.

2024 MSCI EM elections complete – results mixed

Past performance is not a guide to future performance and may not be repeated.

Prior 5-days and market reaction date assessed relative to election result announcement. E.g. Indonesia based on initial ‘quick counts’ on 15 February (official results announced on 27 March). *India elections held 19 April to 1 June, results announced on 4 June. 15-days shown for South Africa to capture period permitted to form coalition. Traffic lights to show market reaction: Red = < -1%, Amber = -1% to 1%, Green = >1%. Source: Schroders Strategic Research Unit, as at 10 June 2024. USD total return.

South Africa

South Africa held its general election on 29 May. Opinion polling had indicated that the African National Congress party (ANC), which has governed South Africa since 1994, would see a decrease in its share of the vote but win sufficient support to remain in power. In fact, the ANC’s vote share fell from 57% in 2019 to 40%, far worse than expectations. The main opposition Democratic Alliance (DA) attained 22% of the vote, up slightly versus 2019. The vote share primarily moved to the MK Party (15%), founded only six months ago and led by former ANC leader and president, Jacob Zuma. The Economic Freedom Fighters (EFF) finished fourth with a 10% share. These results reflect a splintering in the ANC vote: these two parties are led by former ANC members and combining their vote share with the ANC would reach 65%, close to the historical vote share of the ANC.

With the ANC losing its majority, uncertainty increased post the election result. The equity market fell over 3% in US dollar terms on the day after the election as the results began to filter through, and the rand fell 2%. Five days post the election the market was down 6%. The indecisive results ushered in a period of elevated uncertainty, though financial markets were somewhat resilient in the circumstances and did not reflect the most negative scenarios. Under the constitution, the ANC had two weeks after the election to agree a coalition or confidence and supply agreement with other parties. Various permutations were possible, but with very different implications for the policy trajectory.

President Ramaphosa proposed a ‘Government of National Unity (GNU)’, inviting all parties to the table. The EFF rejected the plan, given the inclusion of the DA, and the MK has indicated it would not work with the ANC whilst it is led by Ramaphosa. This left the ANC, DA, and smaller parties to form the GNU. It appears a shrewd move by the president as the optics show MK and the EFF rejecting the GNU, as opposed to the ANC opting to go into a coalition with the DA. Ramaphosa has since been re-elected president by parliament and inaugurated as president.

This outcome is market positive and should ensure continuation, and potentially an acceleration, in structural reforms. However, risks remain elevated. This is the first coalition in South Africa in the modern era, and the ANC and DA have some significant policy differences to overcome. The risk to the outlook is political gridlock, and in a worst case a collapse in the GNU, potentially opening the door for parties with significantly different policy agendas to come into a coalition government. There is also key man risk as, should Ramaphosa lose sufficient support within the ANC, he could be replaced at the next National Conference of the ANC, due towards the end of 2027.

The equity market and the rand have picked up after announcement of the GNU and President Ramaphosa’s inauguration. The MSCI South Africa is now up 2% in US dollar terms year-to-date (as at 27 June 2024). The rand has also recovered, and the 10-year government bond yield is down to 10.2%.

Click here to read more...