What moved the markets – a round-up of 2020

Patrick Mathabeni, Research & Investment Analyst at Glacier by Sanlam

Global overview

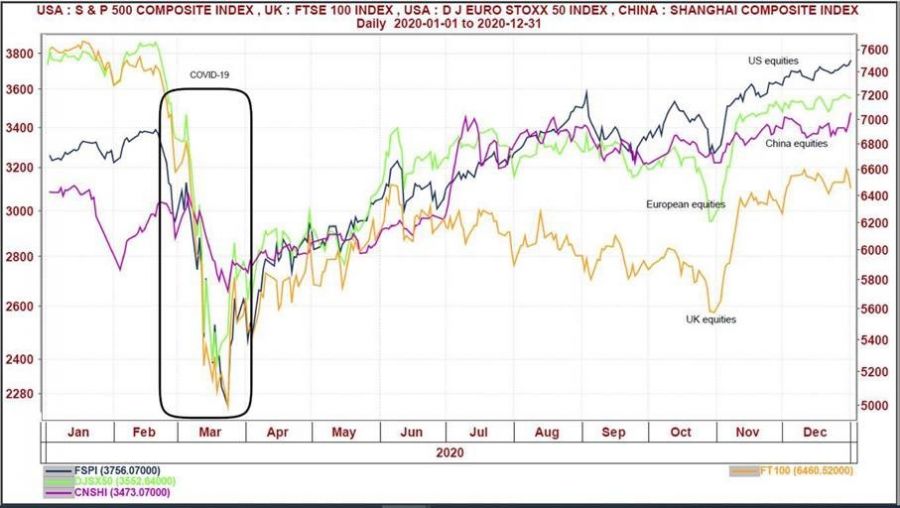

COVID-19 sell-off

The outbreak of the coronavirus shattered sentiment as volatility spiked to levels last seen during the Global Financial Crisis. The rapid spread of the virus saw the first quarter ending with cases having surpassed 1.3 million globally, most of which were recorded in the US, following Trump’s resistance to implement lockdown measures. US markets sold off sharply, exiting the longest bull market in history. US equities were down 20% in the first quarter of 2020 while developed market and emerging market equities lost 21% and 24%, respectively. UK (-29%) and European (-27%) equities suffered much deeper losses, however losses in Japanese equities (-11%) were less harsh. On the economic front, lockdown restrictions halted economic activity, leading to massive job losses across the globe. US jobless claims spiked to nearly 10 million in the last weeks of March before ending the quarter just above six million. Purchasing Managers’ Indexes entered contraction territory, across both developed and emerging market economies.

Source: iress

The oil crisis

Concerned about the oil demand shock emanating from the outbreak of the pandemic, OPEC (Organisation of Petroleum Exporting Countries) took a decision to cut oil production by an additional 1.5 million barrels per day so as to keep prices afloat and called on other non-OPEC countries to do likewise. However, the refusal of Russia to do so led to a price war wherein Saudi Arabia increased its oil supply significantly, creating a supply shock. Brent crude fell 30% in one day (the largest fall since the Gulf War) while the West Texas Intermediate (WTI) crude oil price suffered a shattering 306% decline to sub-zero levels at some point. While oil prices have seen a significant rebound following the subsequent agreement by OPEC (and its allies) to cut oil production by 9.7 million barrels per day and the re-opening of economies, they are still not at pre-pandemic levels. Brent crude closed the year at approximately $51/barrel (compared to approximately $65/barrel at the end of 2019), coming from a low of $19/barrel during the height of the pandemic.

Global economic stimulus drives

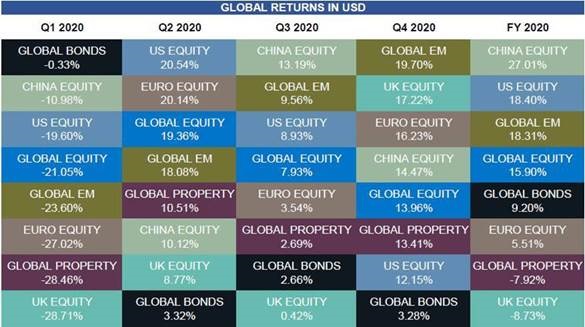

Markets speedily recovered in the second quarter of 2020, largely driven by unprecedented developed market fiscal and monetary policy actions from government and central banks. The series of interest rate cuts were coupled with other non-conventional methods such as liquidity injections (through bond buying programmes) and the easing of commercial bank liquidity and capital requirements. A massive $2 trillion stimulus package was unlocked by the US government - the magnitude of which was more than twice than that of the stimulus for the Global Financial Crisis. Other developed market central banks followed suit in implementing aggressive stimulus measures. The ECB (European Central Bank) announced an emergency bond buying programme of €750 billion while the BoE (Bank of England) continued to target a £745 billion asset purchase. The BoJ (Bank of Japan) also announced a stimulus package of $700 billion which was later increased to $1.02 trillion. In emerging markets, China’s central bank eased the liquidity requirements of commercial banks while also pumping $243 billion into the financial markets.

In the second half of the year, monetary policy remained loose across the board while the Federal Reserve shifted towards a flexible form of average inflation-targeting, aimed at achieving an inflation rate of 2% in the long run which, by implication, will extend the low interest rate environment. Developed economies exhibited signs of recovery following the wide re-opening of economies. As a result, US unemployment conditions improved steadily as economic activity trended upwards, despite the return of trade tensions between the US and China. Talks of additional stimulus remained a point of discussion as the Republicans and the Democrats struggled to reach consensus.

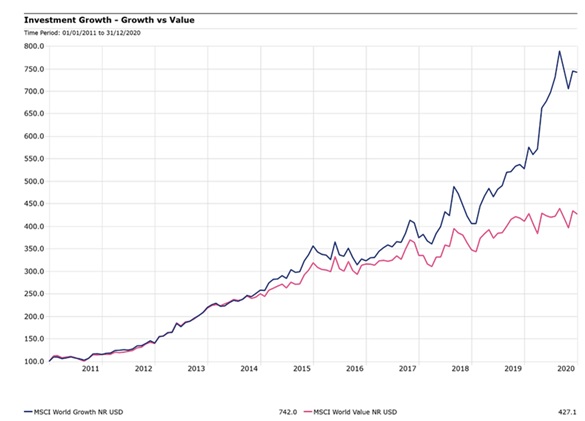

Growth vs Value

Growth pockets of the markets, particularly US technology stocks, saw an incredible rally that stemmed from tailwinds provided by lockdown and work-from-home measures. Technology names such as Facebook, Apple, Amazon, Alphabet, Netflix and Microsoft climbed to historic highs, leading to the widest divergence seen between growth and value stocks. To put this into context, if these five technology stocks (which account for roughly 23% of the S&P 500) are removed from the S&P 500, its performance would be flat over the last five years. In addition, the aggressive upswing in global equities was neither supported by earnings nor by economic fundamentals, but rather by sentiment propelled by the stimulus. However, an intermittent rotation into value (or cyclical) pockets became a dominant feature in the last quarter, as investors remained concerned about lofty prices of technology stocks while also keeping an eye on a potential cyclical rebound which may be supportive to value stocks.

Source: Morningstar

US elections and the race for vaccines

The resurgence of COVID-19 cases in Europe and the UK weighed negatively on sentiment alongside the run-up to the US presidential election which saw Joe Biden elected as the 46th US President. While volatility was not entirely off the table, news of potential vaccines provided a much-needed backdrop for the global economy.

Source: Morningstar, Glacier Research

Local overview

SA economic backdrop

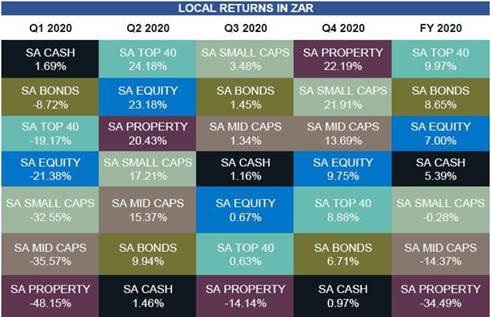

By the time COVID-19 hit our local shores, the SA economy had already been on a fiscal backfoot for a while and growth was elusive. State-owned enterprises (particularly Eskom) and the ballooning wage bill remained the biggest burden on the fiscus. Following the market-friendly budget speech, the country went into a national lockdown, bringing an already ailing economy to a grinding halt. Consequently, a ratings downgrade came into effect, debt levels worsened, business and consumer confidence plummeted, unemployment deteriorated, and the budget deficit widened. The local economy declined by 16.6%% in Q2, driven mainly by the national lockdown as all sectors suffered a contraction except the agricultural sector. Tourism, travel and hospitality were amongst the sectors extremely hard hit. On the back of easing lockdown measures in the second half of the year, GDP grew 13.5% in Q3, albeit from a low base. Business confidence and economic activity steadily resumed.

Government and central bank policy response

In line with global fiscal and monetary actions, the SA government announced a COVID-19 stimulus package to the tune of R500 billion, which mainly comes from credit guarantees through banks, the reprioritisation of the existing budget and borrowings from international finance institutions (part of which was the rand-denominated $4.3 billion from the IMF). On the one hand, the SARB cut rates by 3% in total for the year while it also bought government bonds through the crisis in order to create liquidity in the market, following the bond yield spike and currency shock.

COVID-19, the rand, the JSE and commodities

In the first quarter of 2020, the JSE plummeted over 21% with property (-48.15%) and financials (-39.48%) hardest hit while all other sectors were also down, leaving no place for equity investors to hide. The rand blew out in March, suffering a 14.04% depreciation as bonds sold off in tandem with equities. The gold price, however, was experiencing a rally due to the risk-off environment which tends to increase demand for the precious metal, given its safe-haven perception. As a country that exports gold and imports oil, the rally in the gold price coupled with the lower oil price was supportive of local economics. Markets rebounded in the second quarter as the JSE advanced 23.18% with resources rallying 41.20% in the second quarter.

The gold price remained quite elevated throughout the year even though it weakened slightly in the fourth quarter as risk-on sentiment returned towards the end of the year. As a result, gold mining shares such as Harmony Gold (+39.84%), Sibanye (+67.18%), DRD Gold (+139.60%) delivered stellar returns for the year. JSE heavyweights, Naspers (+31.80%) and Prosus (+52.39%), also posted double-digit gains for the year.

Overall, the JSE ended up 7% for the year, mainly driven by resources which were up 21% for the year. SA industrials (rand hedges) were up 12% while financials were down almost 20%. Bonds outperformed local equities, gaining 8.65% while cash was up 5%. The Top 40 ended 10% up while property remained under pressure, suffering a loss of 35% for the year.

Source: Morningstar, Glacier Research

In conclusion

Growth and market performance will depend largely on how the pandemic plays out and how soon economic activity will revert to pre-pandemic levels. The roll-out of the vaccine is also seen as an important factor. While many investors had a knee-jerk reaction in the COVID-19 sell-off, staying the course of your long-term investment plan is crucial to weathering any market storm. Therefore, we urge clients to consult with their financial advisers before making any investment decisions.

Glacier Financial Solutions (Pty) Ltd and Sanlam Life Insurance Ltd are licensed financial services providers