What matters most

"No one to hear, no one to mourn / Destroyed the forces of the Crown / With thirteen thousand they started / Just one returned from Afghanistan."

So ends the 1858 ballad The Tragedy of Afghanistan about the disastrous 1 842 retreat from Kabul, Britain’s biggest military defeat in Asia before the Second World War. The recent withdrawal of US forces from Afghanistan was much more peaceful from the Americans’ point of view, but the lightning speed with which the country has been taken over by the Taliban is surely no less horrifying.

President Biden emphatically promised there would be no evacuation from embassy rooftops, as during the fall of Saigon in Vietnam in 1975. And yet the images were eerily similar. Strictly speaking, the failure belongs to the Afghan and not the US government, but it is the latter whose reputation is tarnished.

These events put a major question mark against any future American intervention in the region and elsewhere, potentially emboldening terrorist groups and even other states. The idea of the Pax Americana or the ‘liberal international order’ continues to fade, in geopolitics as well as in the economic sphere.

President Trump’s assault on economic globalisation has only partly been reversed by his successor, with tariffs against China remaining in place. Global cooperation and integration are by no means dead, and we certainly need it to effectively deal with the pandemic and the much more existential threat of climate change. But increasingly we seem to be leaving the era of American hegemony behind and entering a much more uncertain Post-American world. We will only know the full consequences over time.

In the meantime, we can ask how investors should interpret the events in Kabul? Here are three broad learnings: on the nature of uncertainty, the true drivers of global markets, and what it really means to be a failed state.

Life is full of uncertainty

Firstly, things change quickly. British Prime Minister Harold Macmillan was once asked to identify the greatest challenge to his administration, to which he famously (though possibly apocryphally) replied: “Events, dear boy, events.”

Incidentally, Macmillan’s advice to his successor Alec Douglas-Home in 1963 was “you’ll be fine as long as you don’t invade Afghanistan”.

‘Events’ are a problem for investors too. Sometimes they genuinely change the landscape, such as the fall of the Berlin Wall or the ‘Nixon shock’ when America ended the convertibility of the dollar into gold 50 years ago this month. Usually, though, events add to the noise. It is hard to know how significant they are for sure at the time they are occurring. For instance, the past two decades saw a number of serious disease outbreaks – SARS, MERS, H1N1, Avian Flu, Ebola – that faded away. When the ‘big one’ eventually hit in 2020, it was initially believed it would also be short-lived.

For investors, the most damaging events often emanate from within the financial system itself, as was the case with the 2008 global financial crisis. It did far more damage to global portfolios than any one of the many coups, civil wars, invasions and terrorist attacks that have taken place since (unless of course you live in one of those affected countries).

Indeed, the biggest damage ‘events’ do to portfolios is often urging action when doing nothing would have been the best course of action. Since it is not always clear at the time whether action is needed or not, sitting tight should be the default option.

The reality is that predictions, even from experts, are often wrong. Even the lauded American intelligence services did not foresee how quickly the Afghan army would melt away as the Taliban overran the country. And if they did, they failed to properly communicate this to their political leaders.

After the fact, things seem obvious. One event leads to another and the eventual outcome seems inevitable. Hindsight is 20/20 vision, after all. But virtually nothing in history was inevitable. The future then, even the near-future, can evolve in many different directions.

It can feel a bit trite to be reminded week in and week out how important diversification is to an investment portfolio, but it is fundamentally important. We simply do not know what tomorrow holds. Being appropriately diversified is the best way to manage risk and broaden opportunities. Unloved investments can quickly turn around, while a high-flying investment can be unexpectedly brought down by anything from regulatory changes to technological disruption to the revelation of fraud. And of course, to this list we can now add a global pandemic.

Monetary policy in focus

Afghanistan is unimportant in terms of the global economy and barely has any financial markets to speak of. Turmoil in other countries in the region usually sees the oil price increase, but unlike its neighbour Iran, Afghanistan is not a significant oil producer. The events of the past week have made for riveting viewing and have rightly dominated the headlines, but they are unlikely to move markets in the short or even longer term. The real market mover is economic policy in the major economies, particularly the US.

Chart 1: Brent crude oil, $ per barrel

Source: Refinitiv Datastream

If American voters blame President Biden for this debacle, rightly or wrongly, it could present an obstacle to his ambitious multi-trillion dollar spending plans. If Republicans retake Congress in next year’s mid-term elections, it would render Biden a lame-duck president for the remainder of his term.

For now market focus is on monetary policy. The minutes for the US Federal Reserve’s July monetary policy meeting were released with the usual three-week lag. These show a growing consensus among policymakers that it will soon be appropriate to taper the $120 billion per month asset purchase programme. Its policy stance will remain extremely accommodative even as quantitative easing is slowly wound down. Interest rates look set to remain at zero for some time, and the Fed seems very careful not to overdo things.

Still, the prospect of somewhat tighter US monetary policy, coupled with recent data showing a loss of growth momentum in China, increased investor anxiety. Shares and commodities sold off, and as usual, the rand-dollar exchange rate has been a reliable barometer of global market risk appetite. It fell through R15 per dollar for the first time since March.

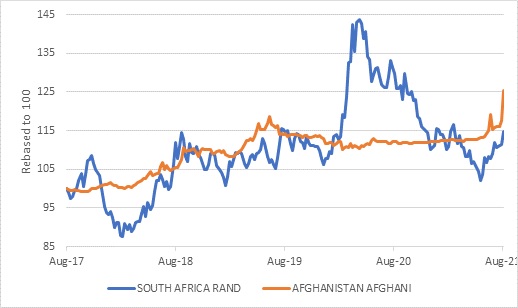

As an aside, despite being a much more stable country, South Africa has a substantially more volatile currency than Afghanistan. Its currency, the afghani, has fallen only 12% against the US dollar since President Biden announced the US withdrawal in April. This points to a currency that is hardly traded in foreign exchange markets (its value probably fell much more in the black market on the streets of Kabul).

By contrast, the rand is highly traded, often used to express a view on global risk appetite and sentiment towards emerging markets as a whole and therefore substantially more volatile. The biggest moves in the rand tend to happen when there is a global event, such as the early 2020 Covid panic, and not when there is a domestic disturbance such as the July unrest and looting.

Chart 2: Rand and afghani against the US dollar

Source: Refinitiv Datastream

Failed states and floundering states

Finally, speaking of the unrest and looting, Afghanistan is hopefully a reminder that things are not all that bad here in South Africa. Afghanistan has been in a state of war, on and off, since 1979 when it was invaded by the Soviet Union.

When the Soviets left, it descended into civil war, with the Taliban eventually taking over and ruling with an iron fist for seven years. The American-led invasion of 2001 brought hope of peace and prosperity, but violence was ever-present, especially in the outlying provinces. As a result, Afghanistan has been high on any list of failed states for many years.

Compared to this, South Africa is merely an underperforming state. We should expect much more from our government in terms of security, health, education and so on. But this is still a constitutional democracy where the will of the people, not the will of the warlords, counts and where political elites are constrained by laws and norms. In the past fortnight we had a sitting president submitting himself to public questioning in a judicial enquiry, something not often seen in other developing economies.

Crucially, despite high levels of crime, recurring public violence and the recent unrest, South Africa is sufficiently stable. Peace and stability are the most basic ingredients of economic development. No one has an incentive to start a business when there is a good chance of it being blown up or taken away by force. Although that risk unfortunately exists in South Africa, it is small. Needless to say, if corruption, crime and violence could be reduced, our economy would perform even better.

And unlike Afghanistan, South Africa is deeply integrated in the global economy and global financial system. This sometimes causes problems, such as volatile capital flows, but ultimately acts as a source of discipline. The market talks, and policymakers listen whether they want to or not. This is what we saw when then-President Zuma was forced to reverse his appointment of Des van Rooyen as finance minister in 2015.

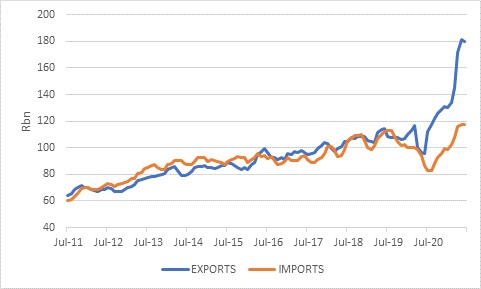

It also means that South Africa directly benefits from stronger global growth, particularly when it comes to exports of minerals and metals, but also cars, food and chemicals. One day, overseas tourists will also return in numbers.

Chart 3: South African exports and imports in US$

Source: Refinitiv Datastream

Eggs and history books

In conclusion, the scenes we witnessed in Kabul this week may one day feature in history books (if there are still books years from now) in the same way that the Vietnam War or the 1979 Iranian Revolution do today. But from a purely investment point of view, nothing much has changed.

The global economy is in recovery mode even though the coronavirus is a wily foe, but recovery does mean that the extraordinary stimulus of the past year or so will be gradually pared back. This is causing a recalibration of market expectations to some extent, but on balance it remains a positive backdrop for long-term investors. Once again, we have all been reminded that things can change quickly, and it is therefore best not to have all your eggs in one basket.