What is happening in global markets and why are equity markets so expensive?

Victoria Reuvers, Managing Director of Morningstar Investments Management SA

Three main drivers have pushed global equity markets to extreme levels:

1. enormous fiscal stimulus from central banks,

2. interest rates are at all-time lows, and

3. the dominance of tech stocks on the back of covid resilience.

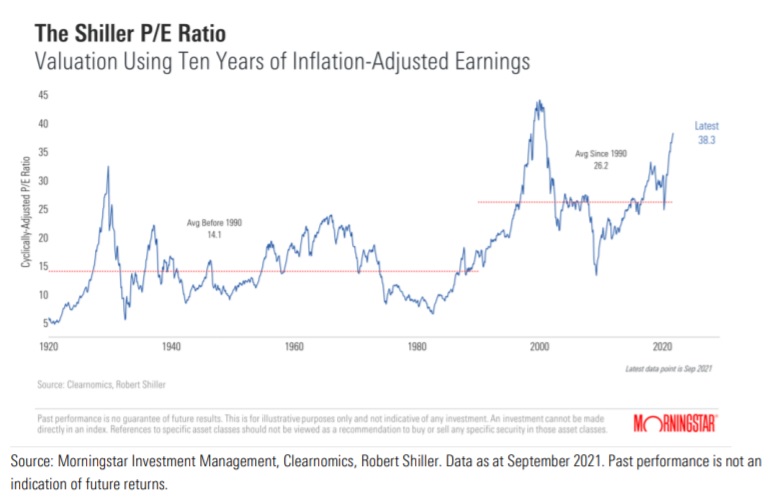

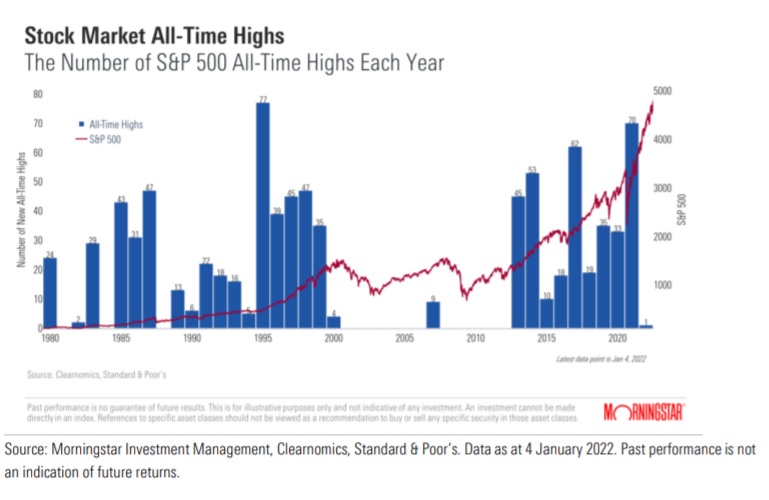

This has resulted in US stock markets reaching all-time highs and trading on valuations last seen in the early 2000’s/dot.com bubble.

Against the backdrop of low interest rates, is the overwhelming narrative that "there is no alternative” (also dubbed the "TINA” theory"). For a while now, “TINA” has been floated as an underlying reason for why the current bull market won't quit.

The fact that both very low cash yields and very low bond yields are the status quo, has meant that investors have been pushed towards riskier assets such as stocks, which seemingly continue to go up…and up…and up.

Let’s not forget that (from a lot of standpoints), equity markets looked pretty expensive going into 2021 — and many key markets, again, look expensive going into 2022. Understandably, these eye-watering valuation levels have got some investors worried - and rightfully so.

There is a cost of capital

The first three weeks of 2022 have seen global equities, in particular the US large cap tech stocks, experience sharp drawdowns. This is a result of rising US bond yields, and the expectation of rising interest rates this year (on the back of high inflation).

The area of the market that is most sensitive to the rise in bond yields is the large cap tech stocks. In essence, a rise in bond yields reduces the valuation of growth like shares (given that they have larger future cash flows than a more cyclical company and a higher discount rate means a lower present value). Given that these stocks are trading on stretched multiples, these stocks are very sensitive to changes in interest rates.

The effect of rising bond yields has led to (already) very expensive stocks looking extremely expensive, and this has caused the recent fall in share prices. In essence, growth stocks love a low interest environment and thrive when the expectation for lower-for-longer rates exist.

Valuations matter

We do caution investors for a potentially turbulent 2022. Central bank policy mistakes remain a possibility alongside heightened geopolitical risk, accentuated by the polarization of vaccination mandates and the already prevalent deglobalisation trend. All the latter is also against a backdrop of higher than anticipated global inflation and, possibly, a step closer to a US equity market correction.

Whilst growth shares have driven returns for the past decade, we are likely to see a reversal of this trend should interest rates rise. The headlines will highlight large drawdowns and losses however this is dominated by the impact of the popular tech shares that comprise a large proportion of US indices. While there will certainly be contagion across markets, cyclical shares and undervalued areas of the market are likely to fare better. The impact of rising bond yields has a lesser impact on fair value and when starting valuations are low, there is limited sensitivity to panic selling.

As uncomfortable as market corrections are, we would encourage investors to remain invested as market corrections allow active managers to invest long term capital at a discounted entry point. Volatility and short-term share price movement is only real should investments be exited, and prices locked in on sale. If you own equities and your time horizon hasn’t changed, we encourage you to remain calm in these current market conditions.

As we look ahead, it is important to remember that the future holds a wide range of possible outcomes and is characterised by unyielding complexity that continually defeats those who seek to make confident forecasts. Fortunately, our role as investors is not to forecast the future, but rather to construct portfolios that empower people to reach their goals whatever the economic and market conditions.

A fundamentally attractive asset can become an unattractive investment when purchased at a high price and, equally, a fundamentally weak asset can provide the most attractive returns when bought at a sufficiently low price. The importance of this dual focus when undertaking investment analysis tends to be lost in markets characterised by excessive optimism or pessimism. As investors become increasingly focused on the future path of prices, confident of either a continuation of the past or a sharp reversal, many forget that most paths lie between these two outcomes.

It is for this reason that we adopt a granular, fundamental and valuation-driven approach to investing, acknowledging that expensive markets can provide opportunities, and cheap markets may be a source of threats. In every situation, the right approach is to view the future probabilistically and think long term.

The hardest, yet most effective, approach when protecting against loss is to distinguish between volatility-induced setbacks and valuation-induced losses. Periods of volatility will come and go, which are scary at the time, but they rarely impact goal attainment.

As advocates of great investing, we must collectively resist impulsive actions and understand that the road won’t be straight. Accepting some volatility is a prerequisite for good returns in any market, but today’s market arguably requires greater care than usual. In our view, this necessitates us to target the best assets to protect and earn, with careful sizing and smart diversification.

A final thought on downside protection: we should be happy to forego some of the gains in strong upwards markets, acknowledging that we won't participate in losses to the same extent as others if we maintain a risk-focused approach. Ideally, if we can limit losses by investing in a risk-focused way, we are less likely to trigger an irrational response from investors, meaning we are more likely to help them stay invested, giving them a better chance of achieving their goals over time.