What Are Sukuk?

Sukuk is the plural of the Arabic word Sak, literally translated as title deed. They are financial certificates structured to comply with Islam’s prohibition on the charging or paying of interest (known as Riba) that grant an undivided interest or share in an underlying asset along with the profits, cash flows and risk commensurate with such ownership. Sukuk are often referred to as the Islamic equivalent of bonds.

The principle of risk sharing is relatively straightforward and lends itself particularly well to investments in listed equity, private equity and real estate, which is where more than two-thirds of Shariah-compliant mutual fund assets are currently allocated.

While the core principles of Islamic finance are over 1,500 years old, the first modern Sukuk were launched in Malaysia at the beginning of this century. Bahrain pioneered the Sukuk Al Salam and Sukuk Al Ijara instruments to the Islamic market in 2001 while Malaysia introduced the global Sukuk Al Ijara in June 2002.

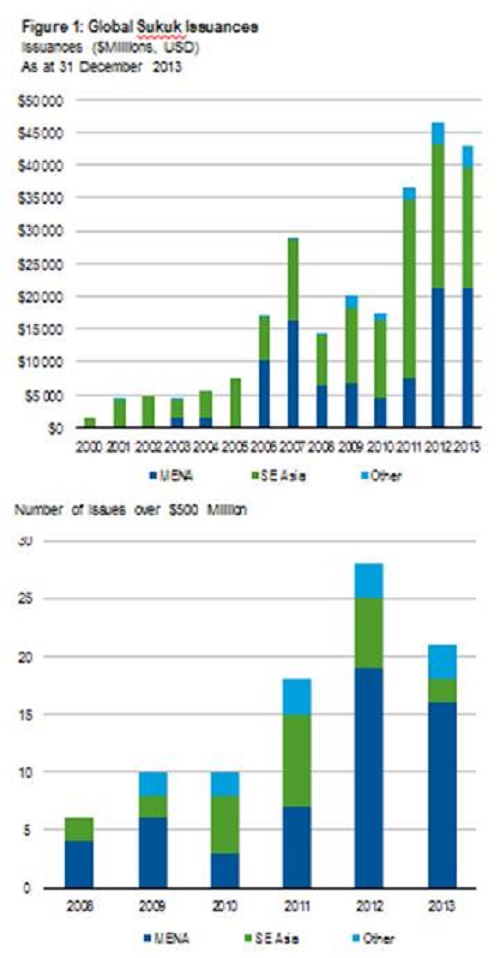

Current demand, which comes from Islamic financial institutions as well as fund managers and high net-worth individuals, far outstrips supply, reflecting the fast growth of the Islamic banking industry and the increasing appetite for credible, Shariah-compliant, liquid securities. Global Sukuk issued by corporations and sovereigns in 2013 slipped 15% to US$115.5 billion from 2012’s record US$136 billion, with Malaysia, Indonesia and Gulf Cooperation Council (GCC) countries still accounting for the lion’s share of Sukuk issuance.2

Issuers tend to be banks, sovereigns and sovereign-backed entities. Until recently, the funds collected tended to be used mainly to finance infrastructure-related projects, although there has been significant diversification of issuers, sectors and underlying assets in recent years. There has also been a noticeable globalization and expansion of Islamic finance products outside their traditional heartland. For international issuers, Sukuk offerings are seen as a way of diversifying their funding base and boosting their profile in the Muslim world, while non-Muslim governments are keen to foster potentially lucrative domestic Islamic finance industries.

How Are Sukuk Structured?

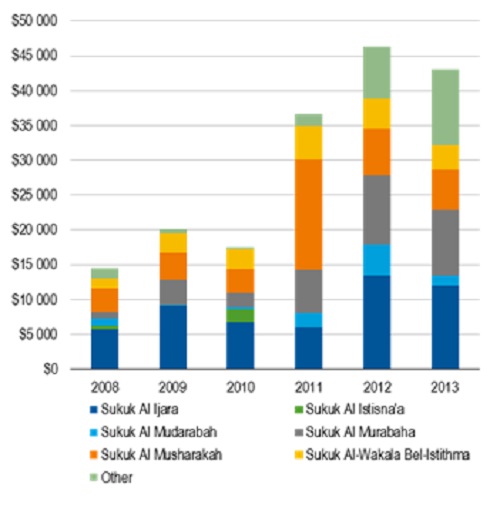

Although there are various kinds of Sukuk structures, depending on the nature of the underlying asset (see below), they all endeavor to generate returns for investors without infringing on Shariah law’s prohibition on the payment or receiving of interest. In addition, as discussed above, all Sukuk provide investors a common share in the ownership of the assets linked to the Sukuk (although, critically, this common share does not represent a debt owed by the Sukuk issuer). The three most popular Sukuk contracts by issuance volume are Sukuk Al Ijara, Sukuk Al Musharaka and Sukuk Al Murabaha.

Sukuk Al Ijara are the most common, straightforward type of Sukuk contract, accounting for over one-third of Sukuk issuance, according to estimates by Bloomberg and Franklin Templeton Investments (ME) Limited. “Ijara” is broadly understood to mean a lease. Sukuk Al Ijara are therefore sale-and-leaseback structures that use revenues from an underlying asset, such as a building, to pay investors. An issuer of Sukuk Al Ijara buys an investment for a customer and then leases it back for a specified period. Returns come in the form of profit from rent, not interest, which is forbidden. As with all Sukuk structures, Sukuk Al Ijara rely upon either the performance of an underlying asset or a contractual arrangement with respect to that asset. Sukuk Al Ijara issuers must therefore identify tangible assets on their balance sheets to back the Sukuk.

Sukuk Al Musharaka is another form of Sukuk contract, derived from the word “Shirkah” which means partnership, in which all partners contribute capital and labor. Profit is shared among partners at an agreed-upon ratio or declining basis. Losses, however, are shared in proportion to the contributed capital. It is not permissible to stipulate otherwise. Essentially, a Musharaka is akin to an unincorporated joint venture but may, if required, take the form of a legal entity.

Sukuk Al Murabaha is another basic building block of the Islamic financial industry. Murabaha is understood to refer to a contractual agreement according to which a financier buys a good or an investment and then sells it on to a customer with a markup on a deferred basis. Customers are expected to be able to meet their payment obligations upon delivery. The advantage of Murabaha contracts is that they offer a form of credit to customers to make a purchase or an investment without having to take out an interest-bearing loan. However, Sukuk Al Murabaha cannot be traded on the secondary market because Shariah does not permit trading in debt except at par value, thus limiting their use to short-term funding, either in the form of money market liquidity management tools or deposit taking by Islamic commercial banks.

Other popular Islamic contracts that have been adapted to issue Sukuk include:

Mudarabah is a form of partnership where one party supplies the capital (rabulmal) while the other manages it (mudarib). Profit is shared among parties at an agreed-upon ratio. Losses are borne by the provider of funds (except in the case of gross misconduct by the other parties).

Istisna is a preproduction instrument used when an item or an asset needs to be manufactured or constructed. The price of the item or asset should be known as well as the time of payment.

Wakala is an agency appointment whereby one party entrusts another party to act on its behalf according to specific terms and conditions. A principal appoints an agent (or wakeel) to invest funds provided by the principal into a pool of investments or assets, and the agent manages those investments on behalf of the principal for a particular duration to generate an agreed-upon profit return.

To see the full perspective from Franklin Local Asset Management Group click here.