Weighing Up The Investment Case For Commodity Stocks

Commodities have been booming lately. Copper is 95% higher than in March 2020 (as at 14 July, and 50% above pre-Covid-19 levels) and has been reaching levels last seen in 2011. Oil is back above US$70, at levels that were not thought possible in a world phasing out fossil fuels, and with recent technological advances in oil and gas extraction (shale).

This is the second commodity bull market in two decades. Just like in 2007, there is current debate around the likelihood of a commodity supercycle – a time when commodity prices trade significantly above their long-term price trends for an extended period. Unlike in 2007, when it was argued that Chinese demand drove the supercycle, proponents of the current potential supercycle point to the lack of new supply to meet future demand (which is likely to be supported by global infrastructure projects combined with substantial 'decarbonisation'-related investment).

In case we had forgotten that the South African economy is heavily dependent on the fortunes of the commodities we produce, rand strength (until June) on the back of a trade surplus and budget overruns reminds us of the windfall that results from surging commodity prices, especially platinum group metals (PGMs). Unfortunately, when stock prices are buoyant, we tend to forget about the boom-bust nature of commodity cycles. It is worth remembering that the past two decades also saw vicious bear markets (2008 to 2009 and 2012 to 2016). Before that, commodity markets were in the doldrums from the late 1970s right through to the early 2000s when the Chinese growth miracle kicked into gear. Although the commodity index has had a good recent run, the performance still lags when compared to that of the S&P 500.

A reminder on the nature of the commodity cycle

Commodity markets move in pronounced cycles because sporadic surges in demand cannot immediately be met by increases in supply. This imbalance leads to high prices and wide profit margins, which incentivises capital spending, leading to lumpy additions of supply. We witnessed this phenomenon earlier this century when Chinese demand drove commodity prices, and we look likely to witness a substantial increase in demand again on the back of the green revolution and infrastructural ‘build back better’ initiatives.

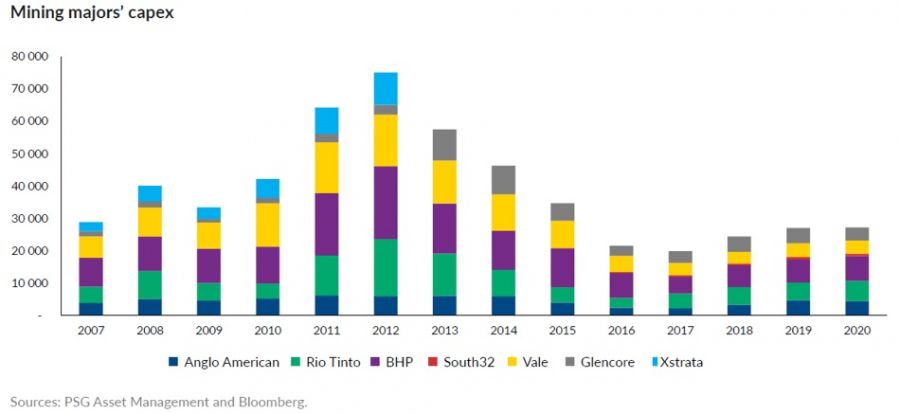

The chart below details the capital spend of the largest miners from 2007 to 2020. Note the supply response to ‘insatiable’ Chinese demand for industrial metals in the 2007 to 2012 period. BHP’s surging capex spend, rising from US$8 billion in 2007 to US$22.7 billion by 2012, is a poster child of the industry’s overall astounding 160% growth in spend from 2007 to 2012.

The rush to build mines in a time of very high commodity prices flooded the market with metals in 2012 to 2015, resulting in some of the mining majors having near-death experiences in late 2015 when Chinese demand eased at the same time that production capacity (supply) surged. Balance sheets that had used debt to finance expansion became very stretched and capital preservation – and in some cases capital raises (Glencore) – became the order of the day. Importantly, the 2015 near-death experience had a pronounced impact on subsequent investor psychology. The mantra from the institutional shareholder base ever since has been to prioritise restoring balance sheet strength first and thereafter focus on capital returns to shareholders. Shareholders’ demands have seen very high hurdles being set for allocating capital to expanding production or exploring for new deposits, and we have seen industry-wide capex all but coming to a halt. BHP has gone from spending US$20 billion a year on mine expansion in 2012 (total capital spend including maintenance US$22.7 billion) to paying US$20 billion back to shareholders this year.

Capital constraints also impact future supply

We have seen similar dynamics at play in the capital cycle for the oil and gas sector: a surge in production, followed by a near-death experience and a strong push for capital discipline and shareholder returns. In this case, abundant cheap capital and technological advancements (fracking) allowed a wall of production to be added in the US between 2010 and 2014 that shattered the OPEC hegemony. Over-indebted oil and gas producers in the US have had a very tough time since, undergoing many years of cash burn, bankruptcies, consolidation and a dramatic reduction in rig count. Like they did for the miners, capital markets have imposed strong capital constraints on oil and gas extractors, with the focus firmly shifting to capital discipline and shareholder-friendly payout policies.

The adoption of capital discipline by commodity producers has had a pronounced impact on future supply. Despite surging prices, exploration remains curtailed and given the long lead times (it can take more than a decade to develop a new large-scale copper project), supply of many commodities could be insufficient to meet robust future demand. Indeed, despite the run-up in prices, the message from the mining majors is that prices would have to be at sustainably higher levels to incentivise a meaningful return of sizeable expansionary projects. Also, the higher-grade deposits in ‘investor-friendly’ countries have been depleted and new supply of metals like cobalt and copper will have to increasingly be sourced in more challenging jurisdictions, like the Democratic Republic of the Congo (DRC).

ESG brings new pressures to bear

Beyond capital discipline at a company level, there is another giant contributor to potential supply constraints: the emergence of environmental, social and governance (ESG) investing. An ESG focus has become well entrenched in capital markets and it is difficult to imagine the influence of this growing trend diminishing anytime soon. That said, the ESG revolution is evolving and while the objectives are sound – holding corporations to higher levels of ESG standards – current implementation is sending tremors through financial markets. For example, the current social mood is firmly focused on the ‘E’ of ESG, with intense political pressure to impose aggressive targets for future greenhouse gas (GHG) emissions or to aim for carbon neutrality. Consequently, there has been a very strong push to divest from industries that are involved in the extraction of fossil fuels or other activities that harm the environment. While such steps and targets are well intended and a more proactive response to climate change is long overdue, things are far from simple and the risks of unintended consequences are extremely high.

The complexities bear some thought

For example, while it is all well and good to refuse to fund new fossil fuel production and mandate future production cuts, we should remember that even the most optimistic projections for energy transition anticipate it taking decades to overturn our dependence on fossil fuels for energy and transport. This is particularly the case in the developing world, which lacks the means to finance a speedier transition. A moratorium on new capacity to replace the existing oil, gas or coal reserves that will certainly be consumed in the decades ahead suggests a high likelihood of higher prices. Higher prices for dirty sources of energy will likely incentivise a speedier transition to greener energy sources but will amount to a tax on poorer nations that cannot afford new renewable energy production or electric vehicles.

Furthermore, governmental commitment to carbon neutrality necessitates the aggressive roll-out of renewable production capacity and meaningful adoption of electric vehicles and other ‘green’ technologies. This transition is of enormous scale and will require significantly higher quantities of certain metals such as copper, nickel, cobalt, lithium and graphite.

Commodity demand is likely to remain supported

China remains the primary consumer of most commodities. Accordingly, a Chinese slowdown remains the largest demand risk to commodity prices. However, it is worth noting that much of the world is just emerging from the Covid-19 slumber and we are increasingly seeing various governments embarking on sizeable infrastructure projects to ‘build back better’ or provide economic stimulus. The US has just passed a trillion-dollar infrastructure plan. While future demand is inherently unpredictable, it is fair to assume that the dependence on Chinese industrialisation for demand will subside as the global decarbonisation initiative gains traction, other developing economies recover from deep recessions and mega-infrastructure projects are undertaken.

A pragmatic approach can deliver optimal outcomes

We prefer to take a pragmatic (and far more demanding) approach than many of our peers when it comes to investing in companies that produce fossil fuels. While many asset managers may decide not to invest in any such companies, or actively encourage these companies to divest from any fossil fuel exposure, this doesn’t actually address emissions. With global demand for fossil fuels likely to be underpinned by increases in developing market demand for a number of years, pushing the supply away from large public companies that are subject to extensive scrutiny could have material negative consequences, potentially even driving an unintended increase in emissions. Where resources companies are trading at substantial ESG-related discounts, we are open to investing and then supporting or driving reductions in emissions by these companies over time, in accordance with transparent public plans. We believe this approach will deliver the optimal outcome – both from a global emissions perspective and for our investors.

The saying goes that the cure for high commodity prices is high prices, as high prices incentivise more supply, while thrift, substitution and recycling weigh on demand. However, commitment to the decarbonisation agenda likely means that demand remains rigid for 'green’ metals, while supply is likely to be constrained for some time. This current status quo of healthy long-term demand for many commodities, in conjunction with constrained supply, supports our base case that the prices of many commodities will remain underpinned, and there is a reasonable possibility that some commodities could trade above trend in the years ahead. As always, we prefer to take a bottom-up approach in identifying varying risks and opportunities within materials and energy stocks and indirect commodity plays. A feature of the current investment environment is that global portfolios are heavily exposed to the winners of the past (passive, growth and the US), and the weightings of sectors like materials and energy in indices are low.

To illustrate, the weighting of the entire energy and materials sectors in the MSCI World Index reduced from 11% in June 2017 to 7.5% by June 2021, similar to the joint weight of Apple and Microsoft at 7.3%. The situation in the US market is even more extreme, with Apple at 6.2% of the S&P 500 being larger than materials and energy combined (5.3%).

We see attractive opportunities in the resources sector

Despite the run-up in commodity prices and recent price performance, many stocks can be acquired at attractive valuations based on normalised commodity prices. While resources stocks are volatile in nature and have had a strong run over the past year, many are currently on favourable valuations, will return a lot of cash to shareholders and serve as very cheap hedges against future inflation, making them a compelling part of a portfolio. Given the attractive set-up we currently see in energy and materials stocks, the PSG Global Equity Fund had 27% of its assets invested in this space. We expand on some of these opportunities in the case studies that follow.

*Case studies include Royal Dutch Shell, Glencore, Shipping Stocks and SA Inc. Stocks.

To view the case studies, please read the full article here