Watering the green shoots

South Africans are long used to bad news, but recently the news has been better. Inflation is much lower, and the Reserve Bank cut interest rates again last week.

In fact, viewed in isolation, the latest South African inflation numbers call for an even bigger interest rate cut than what was delivered. However, South Africa is not an island, physically or metaphorically. It is interconnected with a complex global environment.

Through the floor

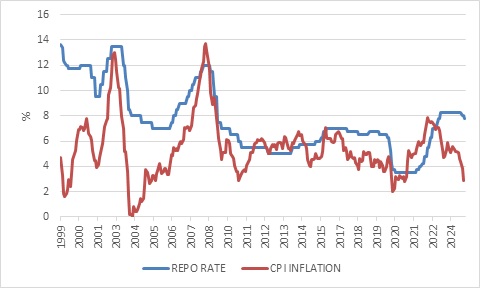

Consumer inflation fell through the bottom end of the 3% to 6% target range in October for the first time since February 2021, when the pandemic played havoc with global prices. That disruption would soon push prices in the opposite direction, with inflation surging globally and locally in 2022 and 2023.

Prior to that, inflation also briefly dipped below 3% in 2010, again in the wake of a global dislocation, this time due to the financial crisis and the wild swings in the oil price. Inflation also fell through the floor in 2004, hitting 0%, after the rand appreciated from R11 per dollar to R6 between 2002 and late 2004.

This time round, the main driver has been the sharp decline in goods inflation, particularly food and fuel prices. Goods inflation fell to 1.4% year-on-year in October. On the flipside, goods inflation was also mostly responsible for the spike in headline inflation above the target band in 2022.

Goods prices make up 49% of the SA consumer price index, and services the rest. Service inflation is stickier and moves more slowly. Arguably it is also more closely linked to domestic demand, while goods prices are largely set in international markets. The good news is that service inflation has been trending lower, dipping to 4.3% in October, but we also know that hefty electricity tariff and medical aid increases still need to be reflected.

In other words, October’s sub-3% inflation number is likely to be temporary.

Chart 1: SA repo rate and consumer inflation

Source: LSEG Datastream

Unanimous

The members of the Reserve Bank’s Monetary Policy Committee (MPC) unanimously decided to lower the repo rate from 8% to 7.75%, maintaining the gradual pace of rate cuts.

The Reserve Bank’s forecast expects inflation to average 4% next year, before hovering around the 4.5% target in 2026 and 2027. The Bank’s economic growth forecasts are broadly unchanged, with growth rising to 2% by 2027. This remains a conservative outlook compared to many private sector forecasters. The MPC statement describes the risks to its growth outlook as “balanced” meaning if the forecast is wrong, it can be wrong in both directions. If the risks are viewed as being to the “upside”, it means the forecast is more likely to underestimate than overestimate.

The statement also views the risks to its inflation outlook as balanced. Despite this, the statement and Governor Kganyago’s post-announcement comments placed a lot of emphasis on factors that could place upward pressure on inflation, including electricity tariff increases locally, but more importantly, increased global uncertainty following the US election. The statement noted that “new inflation pressures and heightened uncertainty” suggest diminished policy space for central banks internationally.

Click here to read more...