Volatile global markets

Izak Odendaal, Investment Analyst at Old Mutual Wealth.

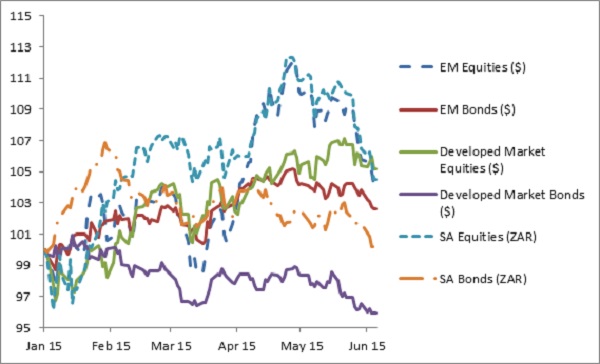

After stabilising in May, the global bond sell-off resumed last week. Again, European bond yields, which had fallen the most over the preceding year, were hardest hit, but US and UK yields also jumped. The German 10-year bond yield touched a yield of 0.99% from 0.52% at the start of the week, its highest level since November 2014. German yields bottomed to an unthinkable low level of 0.07% in late April. Even after the sell-off, developed market bond yields offer no value, unless deflation is expected. Part of the reason for the renewed sell-off is European Central Bank (ECB) President Mario Draghi’s comment that markets must get used to periods of higher volatility. In other words, the ECB will not intervene over and above the existing €60 billion a month quantitative easing programme. The lower the yields, the higher the volatility (a 30 basis point move on a starting yield of 0.5% is massive compared to a 30 basis point move on a 5% yield).

Draghi’s overall message was positive: inflation accelerated more than expected in April (though only to 0.3%) while the economic recovery was taking hold. Developed market bonds and equities have broadly behaved accordingly; with modest positive inflation and improving economic growth, equities should outperform bonds. Bond market liquidity has also decreased over time as banks had to cut back trading operations in line with tighter regulations, worsening volatility. The uncertainty around Greece’s debt repayments further weighed on European markets. Greece took an unusual step in negotiations over its bailout program: it will bundle its four debt payments to the International Monetary Fund due this month into a single payment. This is widely seen as a negotiating tactic to end stalemate.

EM equities pull back sharply

Emerging market (EM) bonds have outperformed developed markets this year, but emerging market equities have lost much of this year’s gains over the past two weeks. This is also more or less according to script: weak economic growth and low inflation in EMs led to interest rate cuts (most recently in India), which are good for bonds but the outlook for company earnings growth is muted. Meanwhile currency volatility has an impact on EM returns when measured in dollars (which is standard). The rand has taken a beating against the dollar, euro and pound, although other EM currencies, like Brazil’s real and Turkey’s lira, have fared worse.

Local markets struggle

Local bonds echoed the global sell-off, with the uncertainty ahead of Friday’s Fitch sovereign rating review also weighing on the market.

Local equities have fallen sharply over the past two weeks, including an unusual ten-day losing streak on the JSE All Share Index. Although there is never a single reason for a market pullback, higher bond yields hit interest rate-sensitive sectors such as banks and properties, particularly hard. Also, the local market had a strong run up to April, probably making profit taking inevitable, especially given the stretched valuations. Healthcare, fixed line telecoms and retail, three of the four worst performing sectors in the second quarter, were also three of the best performing sectors over the preceding year. The fourth, gold mining is still in the doldrums.

Where to from here?

Broadly speaking, equity returns come from three sources: dividends; earnings growth and the change in the price: earnings (PE) ratio. The dividend yield on the All Share is around 3%, in line with its long-term average. A change in the PE ratio (a rerating or de-rating) means that investors change their expectations for future earnings. It is hard to see a further rerating on local or global markets with valuations already on the high side. If anything, a short-term de-rating is possible. Therefore, returns above the 3% dividend yield would have to come from earnings growth. Over the past three years, earnings growth has been positive in the financial and industrial sectors, but negative in resources. A return to positive earnings growth from resources should lift overall JSE earnings, since the financial sector can continue to deliver fairly decent earnings growth if local economic conditions improve, while industrial earnings generally benefit from a weak rand. It is worth remembering that the local economy is still growing around 7% -8% in nominal terms, so locally operating companies can still achieve good top-line growth.

For longer-term investors, South African equities can still deliver positive real returns, but these are likely to be lower than over the past decade or so (when the starting valuations were more attractive). Local long bonds are now trading at yields above the average of the last 10 years, and offer reasonable value.

Chart 1: Developed market, emerging market and SA bond and equity returns

Source: Datastream

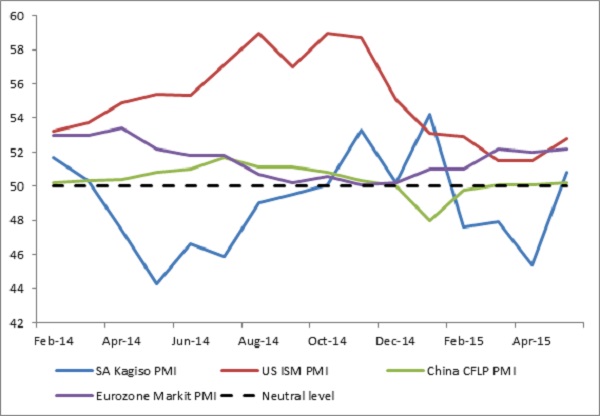

Positive PMIs

South Africa’s Kagiso seasonally-adjusted manufacturing Purchasing Managers’ Index (PMI) rose to 50.8 points in May from 45.4, which was well below the neutral 50 index level. Last month, it suggested that local firms found load-shedding less of a constraint in May than in April. This can also be seen in the business activity sub-index’s jump from 40.6 to 49.6. Expected business conditions also picked up strongly from 56.3 to 61.8. New sales orders rose above 50 points for the first time since January.

The improvement in demand and output is encouraging, but the average for the second quarter so far is still below the first quarter’s 49.9. The manufacturing sector contracted by 2.4% in the first quarter, according to GDP data.

Global manufacturing improved in May

JPMorgan’s Global Manufacturing Purchasing Managers’ Index nudged up to 51.2 points in May from April’s 51.0, suggesting a modest acceleration in activity after the slowdown of the previous three months. Most importantly, the employment component of the Manufacturing PMI survey increased; job growth bodes well for consumption spending down the line. The sub-indices for input and output prices moved into positive territory, suggesting that the short period of oil price-driven deflation is now behind us. Notably, however, it is the developed markets that are holding up the global PMI; the emerging markets’ manufacturing PMI is in negative territory.

The US ISM index, the longest-running PMI, rose to 52.8 in May from 51.5 in April, after seven months of declines.

Eurozone better

The Eurozone manufacturing PMI rose slightly to 52.2, matching the 10-month high reached in March. The Eurozone PMI signals continued expansion in the Eurozone manufacturing sector, but as usual there was quite a divergence between member economies. Spain reached an eight-year high of 55.8 and Italy reached 54.8. France’s PMI was at a one-year high of 49.4, but still in negative territory. Germany’s PMI remained in positive territory at 51.1 but has softened in recent months, while Greece’s PMI fell further into negative territory.

China still weak

The Chinese HSBC Manufacturing PMI was at 49.2 points in May, slightly up from the previous month. Export orders fell at the fastest rate since January 2013, but surveys showed that domestic demand was also soft. Both input and output costs declined. As the economy battles good price deflation, real interest rates remain high. The official Chinese PMI, which focuses on larger, state-controlled entities, was marginally positive at 50.2, up from 50.1 in April.

Chart 2: Manufacturing Purchasing Managers’ indices

Source: Markit, BER, ISM