Underwhelming ECB shows nothing is a one-way bet

Izak Odendaal, Investment Analyst at Old Mutual Wealth.

For all the ups and downs on global markets, this year will probably be remembered for exchange rate movements, including the smallest big move, when the Chinese yuan was devalued by 2%, setting off a violent financial chain reaction. Several emerging market currencies have been hammered this year, including the Brazilian real, the Russian rouble the Turkish lira, and of course, the rand.

In anticipation of the first US rate hike since 2006, the US dollar has strengthened. Federal Reserve Chair Janet Yellen last week gave a fairly upbeat view on the US economy and confirmed that she is ready to move rates from the record low near-zero level. The big question for investors and policymakers in 2016 will be whether the dollar strengthens further. The South African Reserve Bank is very nervous of further dollar strength and rand weakness. But since this is the most widely advertised start to a US hiking cycle in history, a lot of it has to be priced in already.

Great expectations

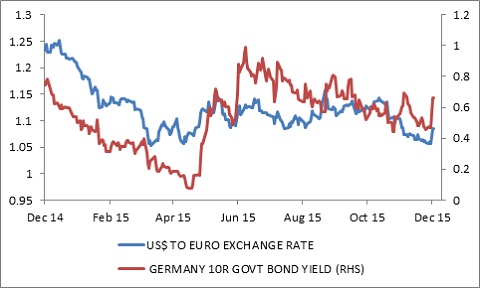

Expectations matter greatly. The European Central Bank announced further stimulus measures last week to combat low inflation. Eurozone inflation was only 0.1% in November while core inflation, which excludes food and energy prices, dipped to 0.9%. However, because the market was expecting it to do more, the euro strengthened by as much as 2.4% against the US dollar following the announcement. Bond yields spiked and stocks sold off. Traders taking big positions before the announcement were clearly caught out, but markets might still come round to accept that the measures are substantial.

The ECB cut its deposit rate – the rate commercial banks earn on their deposits at the central bank - by 10 basis points to -0.3%. By making banks pay to deposit money with it, the ECB hopes to encourage more lending. The ECB will also extend its Quantitative Easing (QE) programme by six months until at least March 2017 at the current monthly rate of €60 billion, and purchase a broader range of assets, including municipal and regional government bonds. The ECB will also now follow the Federal Reserve (Fed) in reinvesting principal payments, meaning its balance sheet will not shrink as the bonds it bought matured.

Markets outsized expectations partly due to ECB President Mario Draghi’s own doing as he previously hinted at significant action, but in the end he was probably constrained by German opposition on the ECB Council . Nonetheless, these measures should support the recovery in Europe. The ECB expects 1.7% growth in 2016 while the 2017 forecast was revised higher to 1.9% from 1.8%. As Draghi noted in his press statement, the ECB is expanding QE because it is working, not because it has failed. Since Europe remains an important export destination for us, and the main source of tourists from outside the African continent, this is important.

Not a one-way bet

What does it mean for investors in South Africa? It is not a one-way bet that the euro will weaken and the US dollar will strengthen. Interest rate differentials are only one of the factors that determine exchange rate movements (certainly rising local interest rates have not helped the rand). Europe has a massive current account surplus and the US a deficit. During the past two Fed hiking cycles, the trade-weighted dollar weakened once rate hikes got underway. And if the dollar did continue surging, it would make matters uncomfortable for the Fed by putting downward pressure on import prices and export revenues. On the other hand, growth in the US is much better than Europe (and Japan) so investors might simply favour the stronger economy.

Fundamentals don’t favour the rand

While the rand has fallen a lot and appears cheap, economic fundamentals don’t favour it. We still have a large current account deficit and the prices of our main exports – gold, platinum, coal and iron ore – have slumped. Since no one knows where exactly the rand is heading, diversification is important. Offshore assets will do well if the rand weakens (all else being equal) while local equities also have a significant rand-hedge component. Bonds and financial shares should do well if the rand strengthens.

Chart 1: Euro and German bond yields

Source: Datastream

Looking for silver linings

Last week was chock full of local economic data releases. Unfortunately, there was little good news. However, it wasn’t all bad news either.

PMI slumped

The Barclays manufacturing purchasing managers’ index (PMI) slumped to 43.3 index points in November, the weakest level since 2009. All the sub-indices of the PMI were below the 50 point neutral level for the first time since 2009. While it was easy to blame the weakness in the local manufacturing sector on load-shedding earlier in the year, it can no longer be the case since electricity production has seemingly stabilised. According to StatsSA, electricity output was basically unchanged in October after rising 2.4% between August and September. However, electricity output remains well below 2013 and 2014 levels. Since there has not been load-shedding in the past two months, this implies a lack of demand from electricity-intensive factories and mines. The factories, in turn, are running below capacity because they too face a lack of demand and are lagging the modest upturn in global manufacturing. The JPMorgan Global Manufacturing PMI was slightly softer in November, but remains in positive territory.

Trade deficit wider

South Africa’s trade balance worsened substantially, with a R21.4 billion deficit posted in October compared to R1.3 billion in September. However, October is traditionally a big deficit month ahead of the holiday season. The cumulative trade deficit for the first 10 months of the year is 40% less than what it was over the same period last year (R59 billion compared to R95 billion). Export growth has slowed down to 4.4% on an annual basis, weighed down by declining export prices. However, export growth is still faster than import growth, which at -2.3% is still negative (largely thanks to the low oil price).

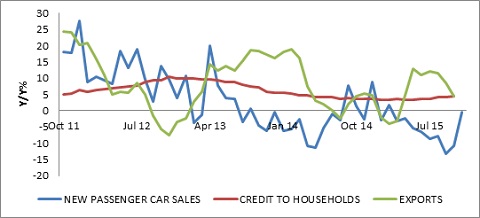

New vehicle sales rose 0.4% year-on-year in November, posting the first (slight) increase in nine months. Most of the improved performance came from heavy commercial vehicles (9.4% annual growth) while new passenger car sales were down 0.6% compared to a year ago.

Mortgage lending has picked up

Private sector credit extension accelerated in October, to 8.8% year-on-year from 8.3% in September. It remains the slowest credit cycle since 1970 and the lack of strong credit growth is probably a factor behind the fact that inflation never materially rose above 6% despite sustained rand depreciation over the past four years.

Both household and corporate credit growth increased in October, but the latter remains well ahead of the former. Households credit grew by 4.5% year-on-year while credit to corporates grew by 12%. Mortgage advances – the biggest credit component – rose by 6% year-on-year. That might not sound like much, but it means mortgage credit is now growing three times as fast as in mid-2013 when the cycle bottomed. Most of the growth has come from commercial mortgages, but home loan growth is also steadily increasing. This should bode well for activity in the real estate sector.

Chart 2: Local economic indicators, year-on-year change

Source: Datastream