Underperforming fund managers cause retirement investors to lose out on returns

Steven Nathan, Chief Executive Officer of 10X Investments.

Are you making the right decisions when it comes to choosing a fund manager for your retirement savings? In the recent Alexander Forbes Manager Watch survey it was noted that it is futile trying to predict which manager will out-perform over what period. It also showed that spreading your investments across different fund managers may not protect you against underperformance as investment managers tend to have a ‘herd mentality’ and follow the crowd.

To overcome this, the survey recommends that investors blend managers with different skills. This requires that they study each manager’s investment philosophy and stock picking process, assess whether this has the potential to capture an above-average return, decide whether the manager’s portfolios reflects their investment philosophy and whether the risks that a manager takes are adequately rewarded.

According to Steven Nathan, Chief Executive Officer of 10X Investments, this suggestion underlines just how ridiculously complicated the retirement industry presents itself. “The industry offers hundreds of different competing and contradictory investment choices. This is compounded by many different investment styles - momentum, growth, quality, minimum volatility, value, deep value and contrarian – as well as different portfolio constructions such as benchmark-cognisant, benchmark-agnostic and enhanced index. Who can make sense of this?”

In his view, the retirement industry deliberately mystifies investors. “Faced with so much choice and confusion, few investors know what to do. They are forced to seek advice and employ consultants who can help them blend the ‘ideal’ portfolio. This just increases costs without adding to the return.”

Nathan says that investors should rather own index funds in their investment portfolio in order to capture the full market return. “Even the Alexander Forbes survey concedes that the simplest way to benefit from equity returns is to invest in a passive investment – in other words, a fund that tracks an index.”

According to Nathan the results of the survey are in line with international studies showing that most fund managers underperform the market. “As per the Alexander Forbes survey, only 13 out of 47 managers of groups of similar portfolios out-performed the market and only 15 equity managers (that each manage a group of similar portfolios) out of 50 beat their benchmark in 2014.”

Despite the proliferation of different investment styles and strategies, most asset managers tend to invest similarly anyway, says Nathan. “In practice, asset managers adopt a herd behaviour, to stay safe within the crowd. They don’t stick to the investment strategies they claim to follow and investors therefore don’t benefit from different strategies or by diversifying among managers.”

In this instance, the survey shows that most multi-asset portfolios (with an offshore allocation) were over-invested in cash. Many of the managers in the survey also shifted into resource stocks and sold shares that have continued to perform well, such as Naspers, Aspen and MTN.

According to Nathan, a fund-of-funds approach does not really achieve what it promises, nor is it possible to predict which active manager will out-perform in future. “Investors are best served with one optimal investment strategy using low cost life-stage index funds, rather than an array of complex, competing and expensive options.”

By avoiding actively managed funds and using index funds, savers earn the average market return - no more, but more importantly, also no less. “When it comes to retirement investing, it is far more important to eliminate the downside risk of earning a below-average return than it is to invest in hope of achieving an above-average outcome.”

Nathan says that the optimal approach is to invest people automatically according to their investment time horizon. In that way the essential advice is embedded in the portfolio already.

“It is equally important that total fees are minimised to ensure more of their savings are invested and that they capture more of their investment return,” he adds. “Once they have done this, they need to remain steadfast in their investment decisions through good and bad periods, and to avoid the industry’s marketing messages to chase what has just done well.”

“Be sceptical about fund managers who offer too many investment choices, as the majority of investors will destroy substantial value over time when exercising investment choice - anywhere between 2% and 4% per year,” warns Nathan.

“Each 1% extra return increases your final pension by approximately 30%. Losing 2% to poorly performing fund managers and high fees will more than halve your final pension and living standard in retirement,” Nathan concludes.

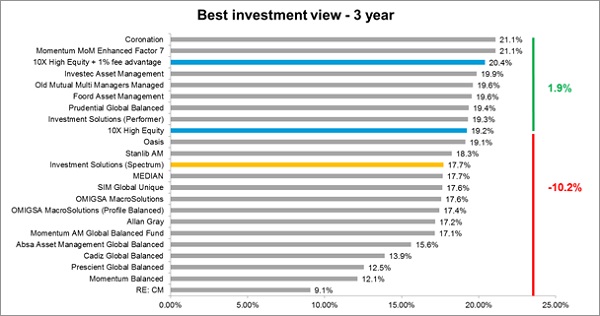

The chart below shows the compound returns (before fees) delivered by large fund managers for long term retirement savers. Over the 3 year period, the average manager earned 17.7% pa (before fees), which is 1.5% pa lower than the 19.2% returned by 10X’s index fund. 10X’s total fee savings (administration, advice and investment management) typically save clients 1% in fees. Thus the after-fee advantage for investors increases by another 1% pa to approximately 2.5%. The best performing fund outperformed 10X’s index fund by a mere 1.9% pa after fees but the worst performing fund underperformed by a devastating 10.2% pa.

Compound investment returns (before fees): 3 Years to February 2015

Source: Alexander Forbes Large Manager Watch Survey, Global Best Investment View, 10X Investments