Ukraine-Russia crisis and the oil price pain

• Oil and other fossil fuel prices have increased sharply over the past year.

• Fears over a Russia-Ukraine war have stoked further recent increases.

• While oil raises the cost of living for consumers and reduces business margins, we’re not yet facing a repeat of 1970s stagflation.

Global oil prices have increased rapidly in recent weeks, some would say alarmingly so. This is part of a broader rise in energy prices that is creating winners and losers, threats and opportunities.

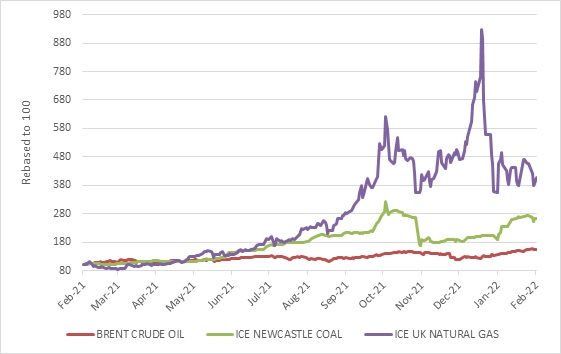

Over the past year, the Brent crude price has risen 60% in dollars to hitting $90 per barrel for the first time since 2014. While oil price volatility is normal, the usually sleepy coal market saw prices triple, fall, and rise again to 156% above year-ago levels. Even more impressive (or depressing, depending on your vantagepoint), European natural gas prices rose in the region of 300%, depending on the specific contract.

Chart 1: Energy futures prices in US$

Source: Refinitiv Datastream

The most immediate cause is the risk of a war between Russia and Ukraine. Russia is one of the world’s energy superpowers, being a major producer of oil, gas and coal. In particular, Europe is reliant on Russian gas exports, and therefore an easy target if Russia wanted to retaliate against any new sanctions imposed by the West. Adding to the geopolitical risk premium usually built into oil prices is a recent attack on UAE oil installations.

The deeper cause of surging energy prices is simply that demand has recovered faster than supply can keep up. It wasn’t that long ago that the reverse was true. Lockdowns in early 2020 decimated oil demand, and a key American futures contract memorably traded at a negative price in April 2020. Traders were giving the stuff away. Not anymore.

Today global growth is strong, mobility has largely recovered, and demand has improved. Supply is a different matter, for a number of reasons.

The first is that OPEC together with Russia still maintains production quotas. In other words, there is an artificial restriction on supply. For those panicking about prices shooting ever higher, this fact should serve to calm nerves somewhat. Cartels require enormous discipline to keep production down when prices are high and there is the chance to sneakily make more money. This is particularly the case for the OPEC countries that rely on oil to maintain public spending while non-OPEC producers have a free ride and benefit from higher prices without having to show any production restraint. Moreover, given that there is no certainty that the world will still be using oil in two or three-decades’ time, there is a strong incentive to get as much of it out of the ground now. But for the time being, OPEC has only announced a small increase in its production quota.

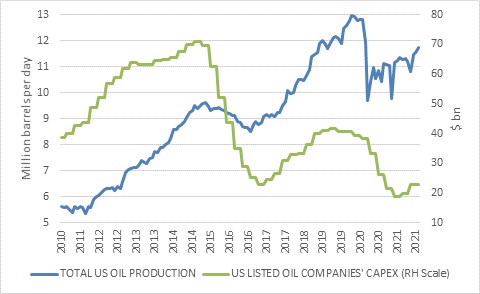

Secondly, the swing producers that emerged so forcefully in the past decade – the US shale companies – have changed their business model in a small but significant way. Instead of spending to grow production at all costs, there is a much greater focus on returning cash to shareholders. Some of the most productive wells are also rapidly depleting, meaning output cannot be ramped up even if producers wanted to.

US oil production has therefore increased after collapsing in 2020 but is still below pre-pandemic levels.

Chart 2: US oil production and capex

Source: Refinitiv Datastream

The third reason is less clear cut but the fact that the extraction and burning of fossil fuels has fallen out of favour among many investors means capital to fund such activities is becoming scarce. Listed oil producers are investing less in new capacity. This is a good thing, but the problem is that the world is not quite ready to function without fossil fuels. Electric vehicle sales have shot up in many countries, but still constitute only a fraction of total vehicles on the road. In China, the world’s largest car market, EV sales increased to around 20% of the total last year, but that means 80% of new cars and an even higher percentage of older cars still have internal combustion engines. This trend towards EVs is likely to accelerate and eventually a key tipping point – peak oil demand – will be reached where oil demand falls sharply when a substantial portion of vehicles on global roads no longer run on petrol or diesel. The influential International Energy Agency believes it can be in as soon as 2025 if policy adjustments encourage further electrification of transport.

This is in contrast to the last big oil price spike, in 2008, when the prevailing narrative was one of “Peak Oil” referring to peak oil supply. This was the idea that the world faced an imminent decline in the supply of oil with devasting consequences for economies and society. It proved to be very wrong for the simple reason that there are abundant sources of oil worldwide – South Africa might even have a meaningful endowment – provided there is the technology, capital and political willingness to extract it from hard-to-reach places.

Where the peak demand tipping point is exactly is hard to know, and until then oil prices can remain quite volatile, with small changes in demand relative to supply causing big price swings, including upward spikes as we are experiencing now.

That is hardly comforting, but the brutal reality is that high, not low oil prices, will spur the adoption of battery electric and hybrid vehicles. The transition to clean energy is not necessarily a smooth or pain-free one, but it still needs to happen.

Market impact

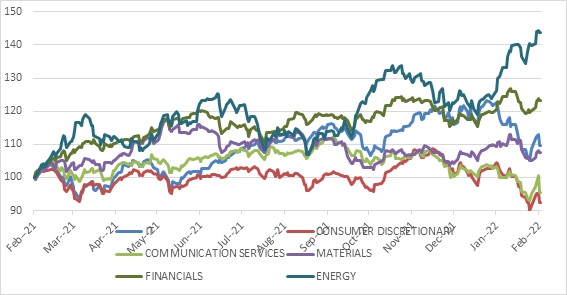

Needless to say, energy shares have surged over the past few months or so. Until recently, investment strategies with an environmental, social and governance (ESG) overlay could claim to outperform with help from being overweight technology shares, and it was an easy sell: do good and earn superior returns. But not this year. In 2022 money has been made by owning the dirtiest of industries and shunning technology.

This does not mean that investors should abandon ESG principles. Rather, as in most things in life, you only realise how committed you are to your principles when sticking to them causes discomfort. If saving the environment matters, as it should, investors should surely be prepared to sacrifice something to achieve that.

Chart 3: Select global equity sectors (MSCI All Countries World Index)

Source: Refinitiv Datastream

Economic impact

Oil embargoes and association price spikes caused a major global recession in the 1970s. Many fear a return to that dreaded period of soggy growth and high inflation. But the world economy is a lot more energy efficient these days. Each unit of GDP uses a lot less oil and gas, and therefore every dollar the oil price rises, takes a relatively smaller chunk out of business and consumer pockets.

However, the recent spike in energy does not leave those pockets whole by any means. The first impact of higher energy prices is simply that there is less money to spend on everything else. Therefore, while energy prices will push up headline inflation rates, central banks don’t respond immediately. They will only respond when there is evidence of “second round” effects, where firms such as retailers push up selling prices in response to higher input costs. This can only happen in reasonably healthy economy. Raising your prices when consumers are under severe pressure means they walk out the door.

The same is true of global food prices, which are hovering around all-time highs according to the UN Food and Agriculture Organisation. Its food price index gained 28% in the past year, driven by increases in a broad range of soft commodity prices as supply chain problems, shipping costs and extreme weather collide with rising demand. Higher oil prices compound food price spikes, as more maize is diverted to produce ethanol. As it happens, Russia and Ukraine are two of the biggest maize and wheat producers, with the famed chernozem (black soil) of the steppe forming Europe’s breadbasket. Conflict between them is likely to put further upward pressure on global grain prices.

Nonetheless, it does muddy the water for central banks. With inflation rates already at multi-decade highs in the US, Europe and elsewhere, surging food and fuel prices can cause a panicked reaction and the urge to do something. We could see faster-than-expected interest rate increases at the same time as consumers are squeezed by commodity prices. This increases the risk of a major slowdown, but for now does not seem likely in the big and developed economies.

It is a different story in some emerging markets where interest rates have risen to nose-bleed levels. Brazil now has the dubious distinction of double-digit consumer inflation and short-term interest rates.

South Africa

South Africa is an oil importer but a coal exporter. Since the coal price has increased more than the oil price over the past year or so, the impact on the trade balance is limited (other key export commodity prices, iron ore and palladium, have also gained in recent weeks). The biggest impact is therefore on consumers’ pockets and companies’ margins.

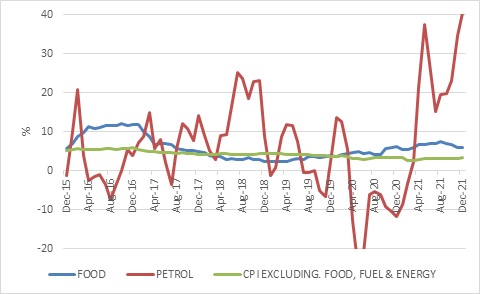

Last week’s price hike took South Africa’s petrol price back to above R20 per litre, but the fuel inflation rate has already peaked. It was 40% year-on-year in December, declining to 28% in February. Today’s elevated price creates a high base from which future inflation rates will be calculated. The petrol price can still rise if global oil prices increase further or the rand weakens and come April, fuel levies are likely to be adjusted higher. However, it is unlikely that the fuel inflation rate hits 40% again.

Therefore, our Reserve Bank can also afford to largely look through these price increases until it sees evidence of firms passing on these increases. Together with elevated food prices, fuel prices undoubtedly put pressure on consumers’ purchasing power. Core inflation is still below 4%, indicating limited passthrough from surging commodity prices to prices of other goods and services.

Chart 4: SA inflation components

Source: StatsSA

A taxing matter

As the petrol price has increased, so have calls to reduce the portion made up by taxes as the various levies make up a third of the total price. Regulated margins make up another 16%, with the basic fuel price (global petroleum prices at the prevailing rand-dollar exchange rate) the biggest component at around half.

It is true that the share of total pump price made up of taxes has increased over time, but it is still not high by global standards. Taxes constitute more than half of the pump price in most European countries, not only because it is a relatively easy tax to collect, but also because it serves to disincentivise unnecessary driving that causes pollution and congestion. In other words, they serve a non-fiscal purpose too.

Some developing countries subsidise fuel prices, which is a great way to keep voters happy but comes at a great cost to the fiscus – especially when global prices spike – as well as encouraging wasteful use. In fact, in some places like Nigeria, subsidised fuel was simply smuggled out of the country and sold in neighbouring states for a tidy profit. Therefore, fuel subsidies are unsustainable in most cases.

If the South African government did not tax fuel, it would have to raise taxes elsewhere. It’s six of the one or half a dozen of the other.

Deregulating dealer margins could result in somewhat lower prices in South Africa but will also likely lead to a big variation in prices between urban and rural areas, with small towns having to pay much more for fuel than cities. In other words, it is not straightforward.

In summary

We should all hope that war doesn’t break out between Russia and Ukraine, but it is unpredictable. Outsiders cannot read Vladimir Putin’s mind. For the time being, the world still runs on oil and other fossil fuels. The sharp increase in prices (from historically low levels in 2020) will hurt global economic activity, but they are not at a point yet where we have to start worrying about a global recession or a repeat of the 1970s stagflation. Therefore, while it makes sense to drive less in response, making large portfolio changes is unnecessary.