Tripped up by trade trepidations

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

Only in its fourth month, 2018 is already an eventful year. As investors digest their first quarter statements, the contrast between the general sense of optimism on the streets and around the braai fires and the disappointing short-term investment returns couldn’t be more stark.

Economic sentiment in South Africa has turned for the better and is benefiting from three tailwinds. The first is obviously the prospect (with some initial evidence) of improved governance and the return of sensible policy-making under President Ramaphosa. Secondly, the global economy is humming along nicely and South Africa, as a small open economy, tends to follow the global cycle with a bit of a lag. Thirdly, local consumers are already benefiting from lower inflation boosting real incomes and spending power. The recent interest rate cut in March will also help. This is a huge improvement from a year ago, when we suffered downgrades, a technical recession and huge political uncertainty. Moody’s has recognised this, announcing that they are maintaining South Africa’s investment grade credit rating and upgrading the outlook to stable.

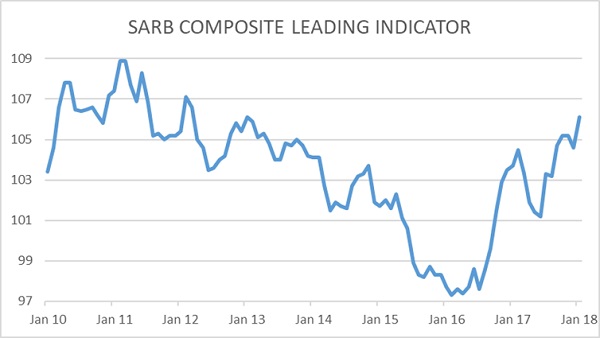

Economic data often lags what is happening on the ground. One of the more recent indicators, the Standard Bank Purchasing Managers’ Index, remained above 50 points in March, indicating that the private sector is growing. The Reserve Bank’s forward-looking composite leading indicator is at its highest level since March 2012.

Return of volatility

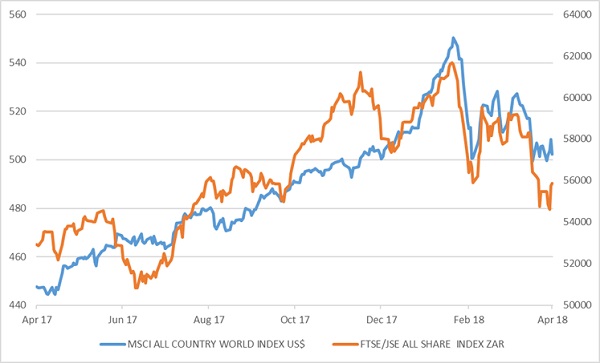

Compared to this fairly happy picture, global equity markets have experienced a torrid time in the first quarter as volatility returned after a long, quiet stretch in 2017. The JSE has followed global markets lower.

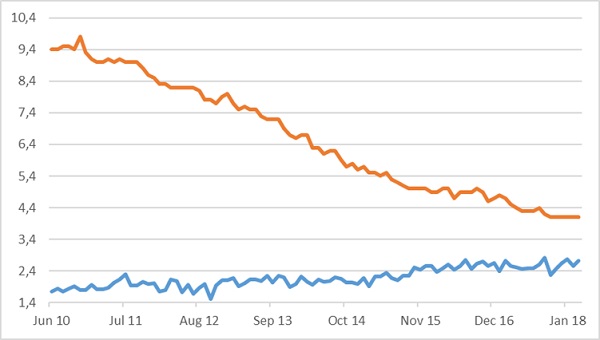

In the past two months, global investors’ optimism, fuelled by tax cuts in the US and strong global growth, has made way to three broad concerns. Firstly, the worry that strong growth and tightening labour markets will lead to inflation jumping and central banks – particularly the US Federal Reserve – slamming on the breaks. Equities and bonds sold off in early February on rising interest rate expectations as data showed a jump in US wage growth in January. That number has since been revised lower, while the same wage growth indicator for March, released on Friday, came in as expected at 2.7% year-on-year. This hardly points to runaway wage and price inflation even as unemployment hovers around a 17-year low. The 10-year Treasury yield has declined to 2.8% since spiking to almost 3% in February.

Secondly, the high-lying technology sector has come under sudden pressure as investors fear a regulatory backlash against dominant companies like Facebook and Amazon. Naspers, the biggest share on the JSE, also had a rough ride as global tech sold off. These shares traded at high valuations after a strong run and were vulnerable to reversal, but there is no evidence yet that their business models are fundamentally threatened.

Trade spat

Thirdly, and perhaps most significantly, has been the concern that the world’s two largest economies are heading toward a trade war after US President Trump announced tariffs on Chinese goods and China retaliated with tariffs on mostly agricultural imports from the US. The background is firstly long-standing complaints that China is pilfering US intellectual property, but more recently that the US trade deficit has ballooned to record (in nominal terms) levels. However, the trade deficit is not a sign of the weakness of the US economy, but rather its strength as improving domestic demand draws in more imports. US exports are also at record- high levels. Trump’s fiscal policy is likely to further stimulate the economy and increase imports, irrespective of tariff levels.

We live in a globally integrated world where almost no piece of machinery, equipment or consumer product is made in a single country in its entirety. Parts are typically sourced from several places and even assembly can happen in different locations. The same good can cross borders a number of times before it is finalised. Detangling these complex supply chains can be like unscrambling an egg. Another layer of complexity is that companies from one country often export to another from a third; the two biggest exporters of cars made in the US to China are German (BMW and Mercedes). This also means that if you try to block imports from China, there is a good chance that imports from India or Vietnam will surge, doing nothing to reduce the deficit.

Markets tend to sell first and ask questions later, but it really does appear too soon to argue that a full-on trade war is looming. There is still plenty of time for the two sides to iron out an agreement (President Trump – whose autobiography is called The Art of the Deal – loves to burnish his credentials as a master negotiator). Within each country, there are also powerful interest groups who would want to maintain the status quo. Last week saw encouraging comments from both sides, but also another shoot-from-the-hip threat from President Trump on Thursday. While both sides have now announced, or are contemplating, tariffs on some $200 billion in traded goods, the decline in market value of global equities has been in excess of $1trillion since the tariff spat began, clearly an overreaction. Looking ahead, with each successive tariff announcement, the surprise factor will be less and market response should be milder.

Global macroeconomic backdrop still healthy

However, it is safe to say that uncertainty is back on markets, particularly regarding the unpredictable US president, and markets never like uncertainty. But looking beyond this, the global economic picture is still healthy. Growth is solid, inflation remains low and central banks accommodative. After all, even though the US Federal Reserve is hiking rates, they are still negative in real terms. In Japan and Europe, they are negative in nominal terms. Companies are generating strong profit growth. Major bear markets have historically only occurred during US recessions (1987 was a notable exception), and there is no sign of a looming recession in the US or any other major economy.

Therefore, investors who follow a considered approach, grounded by a proper financial plan, can avoid a knee-jerk reaction to market turbulence. After all, while corrections are always unpleasant, they are also fairly common, especially after a strong run-up in equities.

No pain, no gain

To benefit from the superior long-term real returns from equities, you have to be prepared to experience some short-term distress. An appropriately diversified portfolio – like our Strategy Funds – will reduce this discomfort, because not all asset classes have struggled. Buoyed by lower inflation, a rate cut and the Moody’s reprieve, bonds have delivered 8% returns year-to-date. But the discomfort can never be eliminated completely in funds that aim to generate above-inflation returns, since no one can time these ups and downs consistently.

It is also worth considering that a portion of most balanced funds – usually around a quarter – is exposed to global markets directly and the rand’s 14% appreciation against the dollar is a further dampener on these returns. Should the rand depreciate in the near future – and remember not too long ago many thought it impossible for the rand to do anything but depreciate – this situation will reverse itself. The importance of diversification is precisely that we do not know exactly what the future holds, and therefore need to be prepared for a range of outcomes.

Sit tight, don’t fight or flight

For investors, it is hardly comforting to hear that they should “sit tight” or “focus on the long term” when faced with dramatic headlines and disappointing returns. Instead, the fight-or-flight response tends to kick in. This is normal. But remember that the fight-or-flight response evolved in a very different set of circumstances, certainly before we were able to do proper financial planning. When looking at markets, we should do our best to ignore our instinctive reptilian brains and engage the more reflective mammalian parts. One way is to remind ourselves of the general principle that financial plans should be amended in response to changes in your personal circumstances, but not in response to changes on financial markets.

Chart 1: Global and local equities over the past year

Source: Thomson Reuters Datastream

Chart 2: US unemployment rate and wage growth, %

Source: Thomson Reuters Datastream

Chart 3: SA composite leading economic indicator

Source: SA Reserve Bank