Tipping point or false dawn? South Africa’s defining question

An air of optimism is breaking through the gloom that has shaped South African news flow in recent years.

The risk of loadshedding has receded, freight transport woes appear to have turned a corner, and the government of national unity (GNU), while not without strain, has held thus far.

At the same time, powerful rallies in gold and platinum prices have bolstered the fiscus, the rand has strengthened, and a benign inflation outlook creates scope for further interest rate cuts. These factors support consumption and moderate economic growth over the near term.

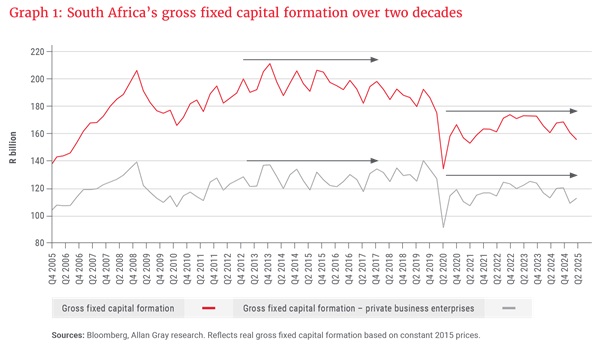

While consumption sustains today, investment secures tomorrow. Despite improved sentiment, South Africa’s gross fixed capital formation – spending on construction, machinery, equipment and other productive assets – remains anaemic, as shown in Graph 1, limiting the economy’s medium-term growth potential.

To achieve the 5% GDP growth that South Africa truly needs after more than a decade of stagnation requires a continued focus on rebuilding and expanding dilapidated infrastructure that weighs on productivity and competitiveness. In acknowledgement of the work required, the government launched Operation Vulindlela in 2020 – a structural reform agenda aimed at addressing entrenched failures in state-owned monopolies and, under Phase II from 2025, widespread dysfunction in local government. Five years on, and with a boost from the GNU, some positive results are emerging.

In addition, as debt-servicing costs ease from a base that currently absorbs 20-22% of national revenue, fiscal space should open for higher public infrastructure investment. This begs the question: Can the alignment of reform momentum and macroeconomic tailwinds deliver an inflection point for South Africa’s economic fortunes?

Electricity reform

After enduring 335 days of loadshedding in 2023, South Africans are acutely aware of the importance of a reliable power supply for economic growth. The current absence of loadshedding reflects not only improved supply, but also lower demand, easing pressure on the grid. In the second half of 2025, average monthly peak demand ran nearly 3 gigawatts (GW) below the 2021 pre-loadshedding baseline – a material delta given that each stage of loadshedding reflected a roughly 1 GW supply–demand shortfall.

A key driver of lower demand has been the government’s 2021 decision, albeit overdue, to lift the licensing cap on embedded generation, unlocking rapid deployment in the commercial and industrial sectors. Together with household deployment, rooftop solar capacity has more than tripled, rising from 2.3 GW in July 2022 to around 7.5 GW today – broadly equivalent to the capacity of all grid-connected utility-scale renewable energy projects. However, weaker demand also reflects the cumulative impact of electricity tariffs roughly doubling over the past five years, weighing on energy-intensive industries.

Click here to read more...