Three ways you can prepare for tougher markets

Economic, market and regulation challenges mean the future is likely to be more difficult than the past.

Johanna Kyrklund, Chief Investment Officer and Head of Multi-Asset Investment at Schroders gives three ways that pension funds can overcome these obstacles as per her article below.

The future impact

We know that a combination of economic, market and regulation challenges are likely to make navigating the future more difficult than the past.

Here, I suggest three ways that pension funds can overcome these challenges, based on my experience of multi-asset investing.

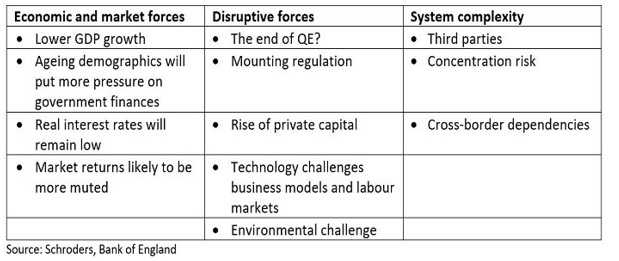

As we outlined in our paper ‘Inescapable investment truths for the decade ahead’, there are a number of adverse or disruptive forces that we believe will shape the investment landscape ahead. In addition to these, system complexity and the inevitable increased regulation of asset owners, not just asset managers, are likely to increase pressure on investors, as shown in figure 1.

Figure 1: The forces that will impact the future

Such pressure and concerns can either lead to inaction or reducing one’s investment and/or operational risks. But I believe that confronting these concerns head on is the appropriate way to address them. Here are my three lessons for navigating through this uncertainty.

Lesson 1: Get the ground work right

Before setting out on any journey or project, it’s important to agree what success looks like. Setting expectations, aligning goals and agreeing realistic time frames are an important part of this process.

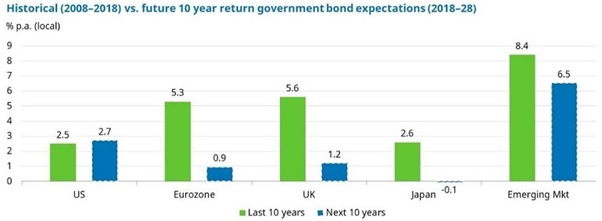

It’s critical to be honest about return expectations, particularly if they are too optimistic. Our expectations for the decade ahead are that both equity and bond returns are likely to be lower than the last 10 years (figures 2 and 3). Recognising this may mean a difficult conversation with a fund’s stakeholders, but it is better to do this before returns deteriorate, rather than after.

Figure 2: The future is different, there is a need to adapt to a new reality

Figure 3: The gap between future and past is even greater for sovereign bond markets

Source for both figures 2 and 3: Schroders, December 2018. The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors

Asset owners are increasingly investing in less familiar asset classes or incorporating ESG into their investment frameworks. As a result, it is important to ensure that the resources available are consistent with ambitions and that the timescale is consistent with the investment. In the case of ESG, this involves establishing a framework to incorporate ESG effectively, including setting objectives, parameters and limits to the extent of ESG integration. This is also likely to require asset owners to move beyond simple screening and stock selection approaches and take a holistic approach to the measurement of sustainability. (For more on this topic please see our research here).

Finally, evaluation of performance should be transparent and there should be accountability in the review and feedback process. Transparency and accountability are key pillars of our multi-asset investment process and they should also act as guiding principles for asset owners in their manager selection and evaluation processes.

Lesson 2: Be prepared and understand your risks

When markets are on the cusp of a transition from one part of the cycle to another, it can be daunting to decide how to position a portfolio. The stress of making decisions is also compounded as volatility increases and investors might feel that they have to make very significant decisions without enough information. Even at a more granular level, investors may be looking for the perfect entry point for an investment but are concerned about valuation, for example.

The same can be said about when to exit an investment that has not worked and there is no clear catalyst for turnaround. Here I believe that, firstly, it is important to focus on the portfolio as a whole. We won’t get every decision right, nor will we always get the perfect entry or exit point. But if the portfolio overall is appropriately diversified, we can withstand some imperfect timing. At the same time, it's important that incentives are aligned with the portfolio as a whole.

It is essential to make plans ahead of time, before conditions deteriorate, so that you may “respond” rather than “react”. You need to understand what shocks your portfolio might be exposed to and what might happen in more stressed conditions. To this end, it’s critical to form a holistic understanding of how all the risks are meshed together.

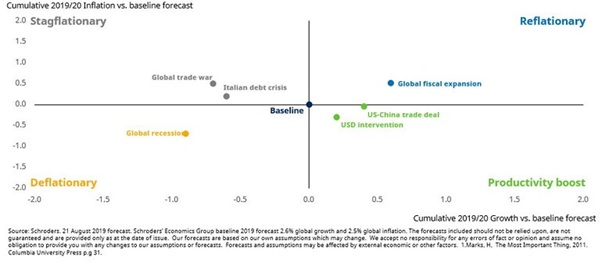

In my experience of dealing with financial market uncertainty, it’s important to identify potential risk scenarios that could have a meaningful impact on both the growth outlook and the portfolio. We continue to take risk in the portfolio but we ‘cushion’ it by implementing hedges against possible adverse scenarios. These scenarios must apply to the portfolio and must be something against which we can invest, rather than just political headline issues. As can be seen from figure 4, we currently worry more about deflationary risks than reflationary risks. Appropriate sizing of the hedges relative to the central (baseline) scenario is key to continuing to take a suitable level of risk in the portfolio. Just focusing on the other scenarios can result in too much ‘protection’.

Figure 4: "Risk means more things can happen than will happen”

Being prepared makes it essential to know what everyone involved in a portfolio will do in an environment where conditions are deteriorating. For example, some of Schroders’ mandates have an actively managed multi-asset portfolio at their core with a systematic de-risking ‘brake’ applied to reduce volatility in extreme conditions. The brake is managed by a separate team to ensure accountability. For these portfolios we have run ‘fire drills’ where we have simulated a market event to check that the communication between the two teams is tight and that responsibilities are clear.

Finally, as a leader, be prepared to step in in the rare event that things go badly wrong. Just because the analysis is good, doesn’t always mean the investment will work well when it is expected to.

Lesson 3: Build a resilient team

Resilience is an often over-used word but in the context of managing assets, from both an investment manager perspective and that of asset owners, it is apt. Being in charge of significant assets and responsible for a team delivering to objectives in challenging conditions can be lonely. There’s burnout risk for everyone involved and more difficult environments can exacerbate this risk.

I am convinced that resilience is a team game. Too much reliance on a small number of ‘resilient superheroes’ might cause these individuals to be unaware of their limitations and overestimate their leadership capabilities, making them difficult to work with and prone to burnout.

In my view, building team resilience requires:

Alignment with a common purpose. Professional competency is a necessary but not sufficient condition for coping with adversity. By establishing a common purpose, you can emphasise outcomes you are trying to achieve rather than causes of failure.

Create a learning culture. Lead by example on self-awareness – admit your own mistakes. I believe it is critical to focus on learning from both successes and setbacks as well as recognising mistakes quickly so that the team may move to a new solution. Linked to this, it is important to promote space for people to fail. After all, mistakes will occur and the team will not learn to cope in difficult conditions if I had a zero tolerance of failure. For more on this please see our article from earlier this year "Multi-asset investing in tough times: the human factors to consider".

Ensure your decision-making structures are “battle-ready”. A tougher environment may require swifter decision-making with smaller teams and / or a less consensus-driven approach. Clarity on who is responsible for each decision is important.

When it comes to additional lessons for asset owners, my belief is that it is important to build a support system. Asset owners often have limited resources – so leverage your relationship with your investment managers if they are true partners. Identify peers at other asset owners or asset managers with whom you can share your challenges. We have found that the most successful sharing cultures between asset owners and investment managers operate on multiple levels.

Writer's Thoughts:

Acknowledging that it will be harder to generate good returns in future is one thing but knowing what to do about it is another. I’ve suggested three lessons that I believe have applicability for asset owners facing similar issues to us managing multi-asset portfolios. It’s not just about numbers and analysis. Ultimately, people and their leaders will have to manage through this and I firmly believe that it is their wellbeing (and a supportive environment in which to work) that will be the answer.

If you have any questions please comment below, interact with us on Twitter at @fanews_online or email - [email protected].