The uncertain road to normality

When will things return to normal? This is the question we’re all asking. Interestingly, the author Jonathan Moodley points out that the term ‘normal’ entered the English language as recently as the mid-1840s, even though it “masquerades as an ever-present universal truth”. Coming from the Latin word norma which refers to a carpenter’s square, it was initially used by mathematicians to mean ‘right-angles’ or ‘perpendicular’.

For investors, the definition of normal might also have changed.

It is clear that we are still in a very abnormal situation. The global spread of the highly contagious Delta variant of the coronavirus means the world is still in pandemic mode despite impressive progress with vaccinations.

The good news is that vaccines still seem to offer the best protection against serious illness, even if booster shots may be needed from time to time. Unfortunately, if rich countries start administering booster shots before people in poorer countries have received their first vaccines, it is not only unfair, but also counterproductive, as this could potentially create the breeding ground for new variants.

The other piece of good news is that the global economy is weathering the Delta storm better than health systems in many countries, the US South is taking particular strain from Delta at the moment alongside Hurricane Ida, but there is no question that Covid is still distorting economic activity.

Delivering the goods

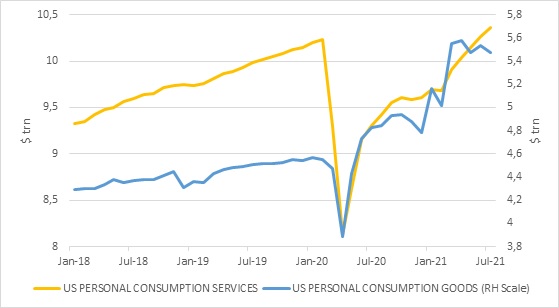

Importantly, consumer spending continues to be robust, but spending on goods is strongly above pre-pandemic levels, while spending on services is still depressed. The reason is that services typically require being out and about and in contact with other people, such as theatres, hair salons, theme parks, dental hygienists and so on. Cancelling a gym membership and purchasing an exercise bike instead is a simple example of switching spending from services to goods. Another would be upgrading your TV instead of going to the cinema.

The problem with spending on goods is that they need to be produced and transported, often over long distances. In contrast, services are typically consumed locally or increasingly over the internet.

Chart 1: US personal consumption spending on goods and services

Source: Refinitiv Datastream

Therefore, the world has experienced a manufacturing boom over the past year, but also a number of shortages, supply chain snarl-ups and bottlenecks. Firms are still reporting long delays in receiving key inputs.

Shipping is a particular problem. A large portion of global cargo is usually shipped in passenger airplanes, but fewer of these are flying across borders these days. In other words, the goods need to go on ships. Shipping rates have shot up as a result, along with the costs of many other commodities. Major ports have long queues of ships waiting to unload their cargoes.

Ships and port operators are also impacted by Covid when crew members are infected. China recently shut the world’s third busiest port, Ningbo, after a single worker tested positive. The shutdown was brief, unlike the week-long blockage of the Suez Canal earlier this year, but the knock-on impact on tightly coordinated supply chains can be severe.

The chips are down

Apart from logistical logjams, the shortage of computer chips (also known as semiconductors) is a particularly acute problem. Covid-related shutdowns impacted the production of these essential components of modern life last year, and the backlog has just grown since then. The shift to remote working and ecommerce massively increased demand for IT equipment, and with it, for microchips. And since there are only a few factories that make microchips, any disruption (Covid-related or not) can cause severe delays. In the past year, a factory in Japan was damaged by fire, while one in Texas was knocked out by severe snowstorms. And in Taiwan, the largest producer, a drought has constrained production.

One of the industries most severely impacted by the global chip shortage is motor manufacturing. Production of new cars is impacted globally. Just last week, Toyota said it would have to almost halve its global production in September due to its stockpile of chips running out.

As a result, many consumers have turned to used cars. But there is a shortage of used cars too, since the biggest suppliers of the used car market in many countries are car rental companies that did not expand their fleets last year for obvious reasons and now don’t have many cars to sell. Used car prices, which normally fall, shot up in many parts of the world.

This is the economic equivalent of the theory of mathematician and meteorologist Edward Lorenz that a butterfly’s flapping wings can, through a chain of events in a complex interconnected system, cause a hurricane in another part of the world.

Inflation blues

This combination of strong demand for goods and the stop-start supply response has been the main reason why inflation rates have shot up, most notably in the US.

Many economists and policymakers have pointed out that this burst of inflation should be transitory because such supply problems tend to sort themselves out. Eventually production ramps up, or consumers look for alternatives, but it is taking longer than expected, particularly in the case of semiconductors.

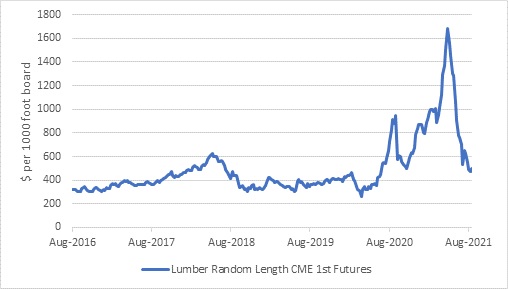

An example is lumber prices. The combination of remote working and low interest rates saw a massive demand for new homes in North America, and with it, lumber. But many sawmills were impacted by Covid shutdowns. Lumber prices shot up as a result, and since lumber futures are traded on major exchanges, speculators jumped in to get a slice of the action.

Today, however, sawmills are working overtime, and supply has been restored. Meanwhile housing demand is cooling due, in part, to high prices. Predictably, the lumber price has come down to earth faster than you can shout Timber!

Chart 2: Lumber price

Refinitiv Datastream

Whether inflation remains elevated, or whether it returns to a lower pre-pandemic pace, the driver is unlikely to be goods or commodity prices. These should stabilise as production catches up with demand (remembering that high prices typically also reduce demand).

This doesn’t mean commodity prices will necessarily slump – that would be bad news for South Africa – but that further large increases seem unlikely. For inflation to be sustained, by definition, prices across the board need to rise year after year. A once-off jump in the price level or in specific prices is not enough.

Rather, the key driver is likely to be services inflation, which is a much bigger component of the consumer basket and tends to be stickier. In other words, when it is low, services inflation tends to stay low, and when it is high, as in the 1970s and 1980s, it tends to stay high.

Policy normalisation

This brings us to the question of monetary policy, and when and how it can return to normal.

As it stands, major central banks are still undertaking large-scale ‘emergency’ bond purchases while also maintaining interest rates at zero or below (in the case of Europe and Japan).

This is not normal. The US Federal Reserve at least had a semblance of an interest rate cycle prior to the pandemic. It gradually raised rates from 0.25% to 2.25%, before slashing all the way back down to almost zero. Europe and Japan went into the pandemic with negative rates.

A normal post-pandemic policy stance in the US might only be marginally positive interest rates, while in Europe and Japan, getting back to zero, never mind positive territory, will be seen as an achievement. So not to levels that were previously seen as normal.

There has been a shift in central bank thinking along the way, however, particularly in the US. Whereas in the past the focus was largely on maintaining steady inflation, the emphasis today is much more on the benefits of having as many people working as possible. This is particularly in light of growing inequality across the developed world.

Indeed, the theme at this year’s annual Jackson Hole central banking symposium held virtually for the second year running instead of in the spectacular Grand Teton mountains, is “Macroeconomic Policy in an Uneven Economy”.

While investors were combing the opening address by Fed Chair Jerome Powell for clues as to when the central bank may start paring back its bond buying programme, the broader message remains that monetary policy will remain extremely accommodative despite current elevated inflation. This is because the Fed wants the millions of Americans still without work to have a reasonable chance of finding employment. Emergency support is no longer necessary, and the Fed might start tapering its $120 billion per month bond purchase programme later this year, but interest rates should remain low for a long time, given all the uncertainties and distortions that still plague the global economy.

This stance implies a preference for equities over fixed income assets across the developed world. Equities might not be cheap anymore, but they are attractive relative to bonds and cash.

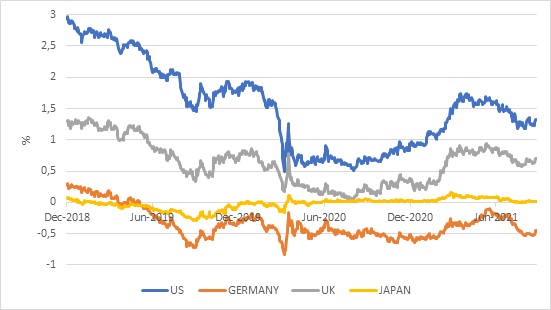

In as much as they can talk, bond yields are not telling us to worry about inflation, but rather suggest that interest rates will remain low well into the future.

Chart 3: Developed market 10-year government bond yields, %

Source: Refinitiv Datastream

A different way of looking at this is to ask: what is the normal the global economy returns to once the pandemic and all its distortions are finally behind us? Is it a Roaring Twenties, as some have argued, or a return to the soggy post-global financial crisis growth of the previous decade?

In the short term, any number of things can raise or lower growth rates, including interest rates, commodity prices, a debt build-up, and changing consumer preferences. The two long-term drivers of economic growth are population growth and productivity growth.

Productivity growth is difficult to predict, depending on several factors, including how much firms invest. We simply do not know whether the shift to digitisation and automation will lead to a productivity boom. It might seem obvious that this would be the case, but not if large numbers of workers are displaced into low-productivity work. Many firms across the developed world are complaining of shortages of labour (along with the shortages of other inputs) and rising wages. This could ultimately force the investment needed to increase productivity. Time will tell.

Dearth of births

Population growth is a lot more predictable. Demographic profiles in the world’s four biggest economies, US, China, Eurozone and Japan, are pretty bleak. Japan’s population is outright declining. The populations of China and the US are growing by only 0.5% per year, a reality that finally led to Beijing allowing couples to have a third child.

So it seems the coming years will be a battle between (hopefully) rapid increases in productivity versus the relentless lower grind in population growth.

What is normal anyway?

Finally, you might ask if recent investment returns have been normal, or distorted along with everything else? This is a difficult question to answer, because there are many moving parts. For instance, developed market equity valuations are reasonable when compared with bonds but not in isolation.

What we do know historically is that returns from equities are lumpy. The superior long-term returns from equities are generated by short-term bursts in prices, sometimes even when conditions on the ground seem far from normal.

A different way of saying this is that while the average long-term real return of SA equities, for instance, is 7% per year, there are few years when the return is exactly 7%. Most years it is more or less. Since we don’t know when it will be more, you need to be invested to benefit.

Ultimately the best guide is asset class valuations. These don’t tell you what will happen to markets in the next month or year, but over longer periods - like five, 10, and 15 years – they are a good indication of potential returns. For instance, South African bonds returned 8.5% per year over the past decade, mainly because the yield on the All Bond Index 10 years ago was 8.5%. Today it is 9.5%. A quick scan of valuations suggests that global bonds could easily deliver negative real returns in the next decade or so, global equities below-average returns, while SA bonds, equities and property are currently priced to deliver above-average returns in a reasonably positive scenario.

Overall, a balanced portfolio should continue to do the job.