The story so far

We are well into winter and approaching the midpoint of 2021. The contrast with the same point a year ago is notable. Back then, South Africa was about to be knocked down by the first wave of Covid-19 infections. Although we are again in the early stages of a new wave, the third one, the situation is different in that government restrictions are considerably less strict this time and are likely to remain so.

Since last year, businesses, schools and consumers have also adapted to new ways of doing things. There is light at the end of the tunnel too, given that a million people have already received at least one jab. With the vaccination roll-out appearing to gather pace after a slow start, last year’s sense of dread and fear has been replaced with a mixture of coronavirus fatigue and greater optimism about the future of the country. Or, perhaps more accurately, levels of pessimism are lower.

Many happy returns

This is also true for investor views of South Africa, as seen in the returns of the various asset classes over the past year. While these are largely determined by global trends, they do also reflect improved local prospects. But even these improved local prospects are due mainly to global factors, notably higher commodity prices. In turn, improved investment returns and rising house prices can boost confidence levels, especially for investors who rely on market performance to generate retirement income. True, only a minority of South Africans have investments, but they represent a disproportionate amount of overall consumer spending.

There is of course still much to be negative about. South Africa’s vaccination programme lags our peers’. New corruption scandals continue to be unearthed daily, seemingly with little consequence. And unemployment remains devastatingly high. According to the latest labour force survey, unemployment stood at 7.2 million in the first quarter or a record 32.6% of the labour force. To put it slightly differently, only 4 out of 10 adults work, a much lower proportion than our peer countries. About 10.5 million people were employed in formal sector jobs, which is 700 000 lower than before the pandemic, but 79 000 up from the previous quarter. What matters from an investment point of view is not where employment is today, but where it can go in the coming quarters. Depressingly, unemployment has always been high in South Africa, even during periods when growth was high and investment returns above average.

Mineral injection

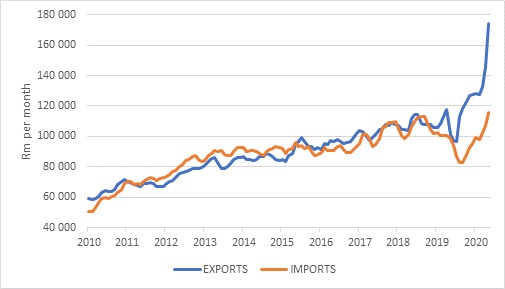

South Africa received a huge injection from higher commodity prices. Exports in the first four months of the year were valued at R575 billion compared with R376 billion for the same period in 2020 and R395 billion for the first four months of 2019. As a result, the trade surplus is at a record level. This is mainly the result of price, not volume increases. To grow export volumes will require substantial investment in expanding production in mining and manufacturing, electricity supply and improved rail and port infrastructure.

Despite our bountiful mineral endowment, we have seen spending on new exploration in South Africa dwindling in recent years, due largely to regulatory shortcomings. The Department of Mineral Resources has promised to address these issues. Changes that improve the incentive and ease of doing business – often called structural reforms – are crucial since commodity prices won’t be high forever. Like so many things, they are cyclical.

Chart 1: South Africa exports and imports, seasonally-adjusted and smoothed

Source: Refinitiv Datastream

Nonetheless, after years of disappointing growth, some of it due to our own goals (load-shedding, political uncertainty) and some of it due to external factors (droughts, pandemic), it is good to have some wind in our sails.

The same is true for investment returns. Returns over the past few years from Regulation 28 compliant balanced funds have been disappointing. This is largely due to South African equities greatly underperforming global equities, but the regulations limit exposure to the latter.

SA outperformance

Over the past year, the story has changed. South African investments have outperformed in common currency terms, with the help of the sizeable appreciation in the rand.

Global equities, as measured by the MSCI All Country World Index, combines developed and emerging markets, but with a much larger weighting to the former, returned 42% in the year to end May in dollars. The US S&P500 returned 40% over this period, leading the developed markets, while emerging markets returned 51% in dollar terms according to the MSCI Emerging Markets Index. These return numbers are clearly unsustainably large and reflect the fact that they are measured off a depressed base. However, even year-to-date returns are in double digits, despite a brief wobble when investors were spooked by inflation fears. Instead, strong economic growth means companies can generate strong profits and earnings estimates have been continuously upgraded.

Global listed property has lagged the recovery of equities with the FTSE/EPRA Nareit Developed, but a good recent run has seen a one-year return of 36%.

Measured in rand terms, the return from global equities over the past year was only 11%, with the appreciation of the local currency reducing the gain for local investors.

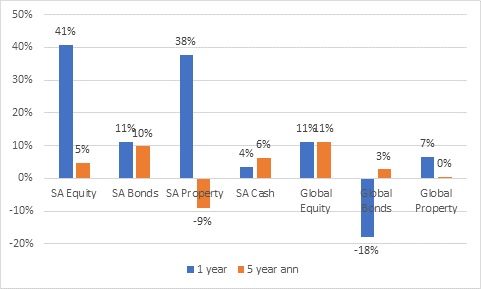

In contrast, South African equities returned 38% over the past year as measured by the FTSE/JSE All Share Index, and 41% according to the FTSE/JSE Capped SWIX. The latter limits the exposure to any given share at 10%, but in practice only Naspers is capped. While this extraordinary return reflects the depressed base from a year ago, the FTSE/JSE Capped Swix returned 14% from the start of this year and 18% since the start of 2020, a period that includes the crash.

In other words, investors would have been better off staying invested through the crash than sitting on cash the whole time. The best return theoretically would have come from being in cash before the crash, then switching into equities near the bottom. People often say they will adopt such a market timing strategy, but in practice it almost never works out. Predicting a crash is one thing, but having the conviction to get back into the market when all hell has broken loose is another.

This surge of local equities over the past year raises their longer-term return numbers and by implication, those of SA balanced funds. This is how it always goes. The long-term average return from SA equities is roughly 13% per year (7% in real terms), but this includes many years where nothing much happens, some negative years, and then years when returns are exceptional. To miss out on these exceptional periods is to substantially reduce longer-term returns. Then you may as well stay in cash and at least be shielded from stomach-churning volatility. It has often been said but it remains true. Missing the 10 or 20 best days on the market will considerably reduce the return one gets from equities even over a 10 or 20-year period.

Annual returns for the FTSE/JSE Capped Swix Index over the past three years have been lifted to 7% (9% for the All Share) and 6% for the past five years (8% for the All Share). The Capped Swix doesn’t have a 10-year history, but the All Share returned 11%.

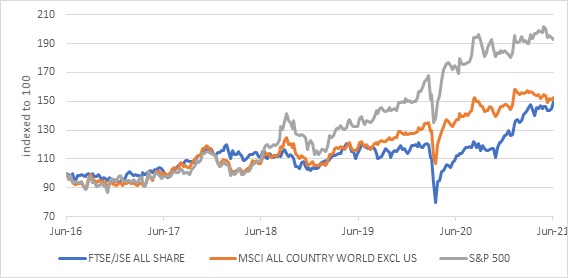

While local equities have outperformed global over the past year in common currency terms, they still lag over long periods (five and 10 years). However, this is largely due to the US and its tech giants. South African equities have caught up with non-US global equities (MSCI AC World Ex US) over five years and almost over 10 years. In other words, local equities have performed broadly in line with the rest of the world, excluding the US.

Chart 2: SA, US and non-US equities over the past five years in rand

Source: Refinitiv Datastream

While the US has the world’s largest economy, most important financial markets, reserve currency and the most innovative companies, a repeat performance of the exceptional returns of the past decade seem unlikely for the simple reason that starting valuations are now so much higher. A decade ago, the forward price: earnings ratio on the S&P500 was 12. Today it is 21.

And while global equity valuations are on the more expensive side of fair value, local equities still offer value (forward PE of 10, lower than where it was a decade ago). Prospective returns from local equities are therefore still good.

Global bonds and cash lost around 20% each in rand terms over the year to end May due to the stronger local currency. The worst possible mistake a local investors could therefore make a year ago was to panic about local prospects and take the money offshore into the perceived safety of developed market fixed income. The rand would have to depreciate by an unreasonable amount to make up for this loss, and the opportunity cost of being invested elsewhere. In fact, given that South African interest rates are historically much higher than in developed markets, if you are going to sit on cash, it is better to do so at home. Long-term rand depreciation does not make up the difference.

In contrast, local bonds have delivered a decent return despite all the worries about the government’s rapidly growing debt pile. The All Bond Index showed 11% over the past year, interestingly tied with the global equity rand return. The main reason is that the starting yield on the ALBI a year ago was 10%. At the end of May it was slightly lower. Most of the returns therefore came from interest payments, not capital gains. The debt problems have not gone away, but the commodity boom means government finances will get a small boost from mining profits. With the starting yield still high for future investments (more than double the Reserve Bank’s inflation target), it remains an attractive proposition.

Despite returns of 16% year-to-date and 37% over the past year, the FTSE/JSE All Property Index has yet to recoup its pandemic-related losses, as well as the weakness predating the pandemic.

Chart 3: Asset class benchmark returns in rand to end May 2021

Source: Iress

How does all this translate into fund returns? A year ago (end May 2020), the one-year return on the average retail balanced fund was -0.2% and the five-year annual return was 2.9% according to Morningstar. Today the numbers are 20% and 5.2% respectively. The five-year return is now slightly ahead of inflation, but still behind the cash return of 6.3%. What this shows is that cash can outperform a balanced fund for a period of five or so years, but will struggle to do so over longer periods (10, 16 or 20 years). Yes, with hindsight, cash was an attractive alternative to a market-linked investment over this period because real short-term interest rates were high. They aren’t any more, and cash is no longer a viable alternative.

Over the last year, the money market benchmark return (the Stefi Index) was only 4%, in line with the lower repo rate. Rates are likely to remain close to these levels for some time and there is little prospect of earning a real return from cash in the next few years.

Lessons from the story so far

What can we learn from all this? The recovery from the Covid-19 crash was much faster than most imagined and too fast to jump in and out of the market. Remaining invested during the uncertainty of the past year was the right thing to do, as difficult as it was.

With all the uncertainties of the future, including the questions over the high valuation of global equities, remaining invested is also the right strategy. But given the fact that the future is always uncertain, diversification is important. How many people a year ago thought that South African investments would outperform global? Forecasting is difficult, and it is better to spread the risk.

Finally, there is much we can and should do to get our house in order as South Africans, but ultimately much of what happens on domestic financial markets is influenced by global factors. The markets crashed and then started recovering even before South Africa had a noticeable Covid-19 outbreak. South Africa remains a small boat floating on large global tides.