The Role Of Hedge Funds In A Balanced Portfolio

The prevailing environment of persistent inflation, growing recession fears and heightened levels of uncertainty continues to batter markets and present strong headwinds to investor portfolios.

Over the 5-year period to December 2022, South African asset classes delivered muted returns - equities (4.8% p.a., measured by the Capped SWIX Index), bonds (7.9% p.a.), listed property (-7.2% p.a.), and cash (5.8% p.a.). The resulting returns for South African retirement fund members, who have the bulk of their exposure in South African assets, have struggled to beat inflation at 4.9% over the same period, mainly due to the lack of growth from SA equities. Global asset classes have provided some support over this period, although 2022 was a horrible year for most global asset classes, except US dollar cash.

Although hedge funds are not new, they are still under-represented in most retirement portfolios. This is arguably partly because of a lack of understanding of hedge funds and the role they can play in a diversified portfolio and partly due to a perception that they are expensive. Yet hedge funds offer attractive features that complement traditional asset classes, and the skills and tools that they bring to bear on a diversified portfolio can be worthy of their higher fees. Nonetheless, as in all investments, the hedge fund territory should only be explored by those with the necessary understanding of this type of strategy.

What Are The Benefits Of Introducing Hedge Funds?

Additional tools

The primary tool in a hedge fund manager’s toolkit that other managers don’t have, is the ability to short stocks. Although this is a tool best left to skilled practitioners, it offers the opportunity to profit from falling stock prices rather than just when prices go up. This short selling creates other opportunities too – because the hedge fund receives cash for the shares they have sold even though they don’t own them, they can then deploy that cash to buy more stocks that they like, a mechanism called leverage. This requires strict risk controls and careful management but can fundamentally shift the profile of returns earned.

Returns generated in a different way

The additional use of short selling creates a fundamentally different type of portfolio that behaves differently to a traditional share portfolio (also called a long-only portfolio). The hedge fund manager can control the overall net exposure of the portfolio (where 100% net exposure is a traditional share portfolio and 0% net exposure, or market neutral, means the value of shorts (borrowed shares sold) cancels out the value of longs (shares owned)). Different hedge funds position their portfolio somewhere on this continuum. As a result, hedge funds tend to capture less of both market up-swings and market drawdowns, resulting in a stable and smoother return profile.

Another important consideration is that hedge fund managers construct portfolios from a clean-slate approach, meaning they pay scant, if any, attention to a benchmark or index. As a result, whereas many traditional managers track the movement of the index up and down, hedge fund managers tend to look and perform differently to any indices.

Agility and access to growth stocks

Many hedge funds manage smaller portfolios of assets, enabling them to invest meaningful portions of the portfolio in the many small and medium sized companies that make up the JSE. Although these shares tend to be more volatile, they are often under-researched by large institutions and their growth phase is often early rather than mature, so their growth potential is better than the mature behemoths in the Top 40. This presents excellent stock-picking opportunities for discerning investors. Their small size also allows hedge funds to trade in and out of stock positions more quickly than very large portfolios. Although this still requires skilled execution, it presents an opportunity to react to opportunities that arise at short notice.

Limiting volatility and downside

Equities are essential for long-term growth that beats inflation by a wide margin (5% per year or more) and this is the level of return required by most retirement savers. However, equities are volatile and subject to sharp falls. The recent 5-year period saw SA equities record the three largest drawdowns post the Global Financial Crisis of 2009, as shown in Chart 1.

Chart 1 also plots the Old Mutual Multi-Managers Fund of Hedge Funds, which invests in equity-centric hedge funds, otherwise known as equity long/short funds (the long/short part is explained above). The downside protection capabilities are clear, although losses are not completely avoided. Volatile market environments such as what we have experienced over the last few years are expected to continue given the stubbornly high inflation, higher interest rate environment and low growth trajectory of South Africa’s economy. These conditions have historically proven to be favourable for hedge funds because of the extra tools at their disposal.

Chart 1

.jpg)

It is thus not surprising that there has been growing investor interest in hedge funds, more so as hedge fund fees have also come down as hedge fund firms reached critical mass and pressure from clients has spilled over from traditional managers into the alternative space. While the absolute level of fees has come down, they remain high and as a multi-manager we will always negotiate firmly but fairly to ensure our clients pay an appropriate fee. It is worth mentioning (although don’t tell any hedge fund managers) that we believe that hedge funds represent a premium solution that justifies a higher fee – it is just the size of this premium that is negotiable, but we do believe it will always settle above traditional portfolios.

We also expect further developments to allow Regulation 28 compliant unit trusts to invest up to 10% in hedge funds. This is a worthy endorsement which, if approved, will offer individual investors the opportunity to benefit from exposure to hedge funds within their existing, diversified multi-asset class portfolios in their personal capacity.

Including Hedge Funds In A Balanced Portfolio

To illustrate the impact of an allocation to hedge funds into a traditional portfolio, we examine the impact of an allocation to hedge funds into various portfolios.

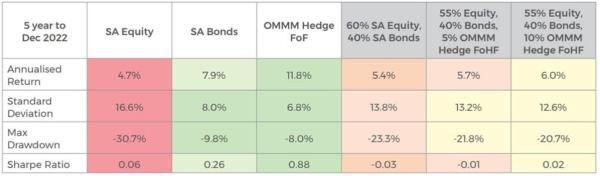

Chart 2 summarises some risk and return metrics for two traditional asset classes (SA Equity and SA Bonds), the Old Mutual Multi-Managers Long Short Equity Fund and three balanced portfolios (one with no hedge funds and two with hedge funds included). We have added a colour code to highlight the good vs poor outcomes of the metrics.

Chart 2

The OMMM Hedge FoF generated more than double the return posted by SA equity net of all fees and did this at less than half the equity risk, which then produced the superior Sharpe Ratio. It should however be noted that hedge funds are not a panacea. They enjoyed an excellent five-year period but this level of outperformance of all other assets at much lower risk is not what should be expected.

However, a relatively small allocation to hedge funds (noting that Regulation 28 allows a maximum of 10%) can have a significant positive effect on the risk-return profile of a diversified balanced fund, with only a small increase in overall fee.

What Do We Expect From Hedge Funds?

Old Mutual Multi-Managers’ primary focus is on generating inflation-beating returns for investors, because we believe that inflation is the most important hurdle when saving for long-term goals, like retirement. In this context, we believe that hedge funds provide valuable diversification benefits from traditional assets, and this contributes to our ability to deliver inflation-beating returns sustainably and consistently. The ability to lower volatility and limit drawdowns, while still providing high real returns makes hedge funds a valuable component of our portfolios. As a general rule of thumb hedge funds look to capture two thirds of the returns of stock markets when they move up and only one third of the negative returns in down markets. Hedge funds are thus an important source of return diversification and a useful component of a client’s overall portfolio rather than being a substitute for traditional asset classes.

Many Hedge Funds To Choose From

Another important consideration is that not all hedge funds are created equal. There are numerous hedge fund managers in South Africa and more than 200 hedge funds that employ different investment strategies at different levels of risk. Requisite manager selection and fund selection skills and expertise are necessary to navigate this space while manager risk should be mitigated by diversification across more than one manager and not by trying to pick the best manager based solely on past performance.

Successful investing requires a combination of skill and luck. Having more skill on your side removes some of the risks and contributes to a more consistent, stable outcome. In our view, an allocation to hedge funds and the different brand of tools and skills that they offer, is a valuable component of a long-term growth solution.