The road from Red October

An old Afrikaans poem refers to October as the most beautiful month, but ten years ago the global financial crisis was in full swing and September and October of 2008 were anything but pretty. The collapse of Lehman Brothers on 15 September 2008 moved the credit crisis into a dangerous new phase as interbank lending markets froze.

From an equity market point of view, October 2008 was the worst month with the MSCI World Index losing 19%. Even this red October was not enough of a capitulation and global equities only bottomed in March 2009, after investors gained comfort that the North Atlantic banking system would in fact survive.

But rather than focus on the dark days of a decade ago, it’s worth reflecting on how investment returns evolved over the subsequent period. This might also provide pointers on how to think about the future.

The mighty dollar

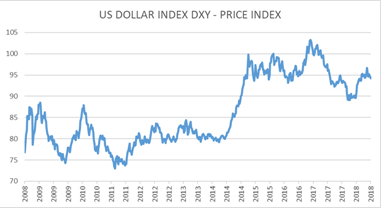

Let’s start with currencies. Despite the US being the epicentre of the financial crisis, the US dollar rallied as investors scrambled for safety. This is important: in a panic, the US is the place to be, because of the unique role of the dollar in the world’s financial system. But as the market panic subsided, the dollar eased again.

The flipside is that the rand slumped in September and October of 2008, but from March 2009 onwards, the rand appreciated from R11 per dollar to R7 per dollar in late 2011. However, at that point, the US dollar began appreciating again, this time reflecting expectations of higher growth and interest rates. For the next five years, the surging greenback would pile on the pain for emerging markets and commodity producers.

Though the dollar has been flat on a trade-weighted basis since 2015 (chart 1), it has experienced episodes of volatility, most notably this year when a renewed rise in the dollar caused panicked selling of the Argentinian peso and Turkish lira, and eventually, the rand too. The 1971 remark by US Treasury Secretary John Connally remains true today, “it’s our dollar, but your problem.”

Today, the trade-weighted dollar is at the expensive side of its historic range. This does not tell us where it will trade in a month or a year, but does suggest that most of its appreciation is probably behind us.

Low interest rate environment

One of the predictions made around the time of the crisis was that the world would enter a “low- return environment”. This was plausible at the time, given that the pre-crisis period saw virtually all asset classes booming, and therefore would always have set a high base for comparison. It also seemed likely that economic growth would be subdued. It definitely turned out to be a low interest rate environment. The US Federal Reserve slashed rates to near zero by December 2008, and remained there until December 2015. The Fed’s rate increase last week (to 2.25%) was the eighth in what remains a historically gradual hiking cycle. The benchmark US 10-year yield declined from 4% on the eve of the crisis to a low of 1.6% in mid-2016. It only rose above 3% this year, finally pricing in a stronger economy and rising inflation.

Low rates in the developed world sparked a search for yield among fixed income investors, especially in emerging markets. The yield on the 10-year local government bond plunged from 9% at the end of 2009 to 5.8% in May 2013 (bond yields move inversely to prices). However, at that point investor perceptions of the future path of US interest rates and quantitative easing changed suddenly (the so-called taper tantrum). From then on local bond yields were volatile, with local politics adding to a more uncertain global backdrop, most notably the firing of Finance Minister Nene in December 2015, a few days before the Fed’s first rate hike. At the end of the third quarter of this year, the 10-year was back at 9%. Over the previous ten years, the SA All Bond Index returned 8.5% per year.

For equity investors, however, the low-return environment didn’t materialise, and returns were not too far off the long-term average (but below the previous exceptional decade). One reason why is that companies relentlessly squeezed costs to grow profits even when sales growth was subdued. The flip-side of this phenomenon is the lack of decent growth in workers’ wages across the developed world. Unfortunately, the fears of a low-return environment might have pushed many investors into cash, the one asset class that definitely delivered low returns.

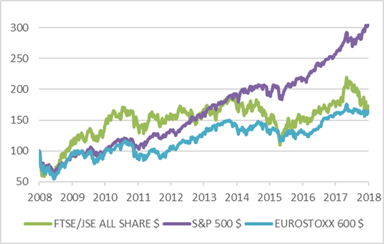

The US benchmark S&P500 Index delivered an 11% annualised return over the past ten years. This includes the fact that share prices only bottomed in March 2009, and would suffer further sharp corrections in mid-2011, late-2015 and earlier this year. Depending on how one measures these things, it has been the longest US bull market on record. One of the most interesting developments was the presidential election of November 2016, delivering two surprises: the first that Donald Trump won, the second that the market rallied, instead of selling off (the consensus was that an unexpected Trump victory would cause investor panic). This was as good a lesson as any how unpredictable events can have unexpected outcomes, making market timing almost impossible.

Notably, US equities have outperformed other markets, with the divergence starting in 2011 (around the time when renewed dollar strength started causing pain elsewhere). The outperformance, illustrated in chart 2, reflects the fact that the US economy recovered better than other developed markets, that US stocks enjoy a tailwind from corporate buy-backs, and that the US is home to the world’s most dynamic tech companies.

The European market by contrast suffered the fate of a second recession, as premature fiscal and monetary tightening combined with the debt crisis in Greece and other Southern European economies pushed the Eurozone into a double-dip recession. The Eurostoxx 600 Index only returned 7% per annum in euro terms (and 4% in dollars) over the past decade.

SA equities recovered sooner than global markets, having bottomed in November 2008. Over the past ten years, the FTSE/JSE All Share Index delivered an annualised total return of 11% in rand. However, there was a decisive break in the return path of the local market in early 2015. From September 2008 to April 2015, the All Share returned an annualised 15% - certainly not a low-return environment - but the subsequent period has seen returns of only 3.6%, most of it from dividends and not capital appreciation.

The other notable feature of the local market is the extent to which JSE-listed companies have internationalised, and hence benefit from a weaker rand. In dollar terms, the All Share only returned 6% per year over the past decade. The dollar performance of the JSE has not been out of line with other major non-US markets over this period, contrary to perceptions that things have been uniquely bad in South Africa.

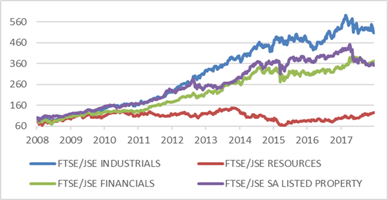

Of the three main economic sectors on the JSE, Industrials had by far the best performance being dominated by large rand hedges, and the remarkable rise of Naspers, which went from being less than 3% of the All Share to more than 20% in the space of a decade. This incredible 1 700% share price gain was of course due to its stake in Tencent, the Chinese internet giant.

While Resources should have benefited from the 6% annualised depreciation of the rand against the dollar over the past decade, the sector only returned 1.9% per year. Commodity prices, and mining shares, rebounded quickly from the financial crisis as a massive stimulus package boosted Chinese imports of raw materials but also inflated expectations of future demand. By 2014 those expectations had been thoroughly dashed and between mid-2014 and early 2016, the JSE Resources Index crashed 44%. Since then, Resources have been recovering, and the sector is the best performer this year, but the 2014 peak has not been regained (nor for that matter, the mid-2008 all-time high).

Financials returned 13% per annum over the past decade, a respectable return. Listed property is officially part of the Financials sector on the JSE, but treated as a separate asset class by most investors. Listed property quickly recovered after the crisis and the FTSE/JSE SA Listed Property Index returned 17% per year until the end of 2017. 2018 has been a disastrous year for the sector as investors question the financial practices employed by property companies to boost distribution growth and a tough economic backdrop.

A few more lessons

What else can the experience of the past ten years tell us about the future? Firstly, valuations matter. The best time to buy was unfortunately when many people were panic-selling in late 2008 and early 2009. While the headlines were scary and emotions ran high, valuations provided a strong signal to buy, not sell. By the time the ‘dust had settled’ markets had already rallied and many missed out. Secondly, over the past ten years different asset classes performed at different points, highlighting the importance of diversification. Lastly, returns have been disappointing over the past while, but they have actually been quite decent over the past decade, despite a very uncertain environment. There is no reason to expect that returns over the coming decade shouldn’t reward patient investors.

Chart 1: Trade-weighted US dollar index

Source: Thomson Reuters Datastream

Chart 2: Major global markets in US dollars, rebased to 100

Source: Thomson Reuters Datastream

Chart 3: Main sectors on the JSE, rebased to 100

Source: Thomson Reuters Datastream