The Rand – what’s its objective value?

Andrew Flavell, Wealth Manager at AlphaWealth.

Rather than relying on dinner-time conversation and personal bias to determine one’s view on the Rand, AlphaWealth provides some analytical data that enables one to make a decision on the Rand or at least be able to present the volatile emerging market currency in a more objective light.

Who are our peers and how have we fared on a relative basis?

There have been five years of headwinds for emerging markets. In fact there has been a perfect storm for emerging markets with commodity backed economies. A Eurozone slowdown, Chinese GDP contraction, plummeting commodity prices, government instability, foreign capital outflow and a rising interest rate environment have made it very hard to make money in emerging markets. The good news is South Africa is not alone. Our peers, including Russia, Zambia and Brazil, have all been under pressure. So while some may dub this the ‘Zuma Effect’ it really is a macro theme.

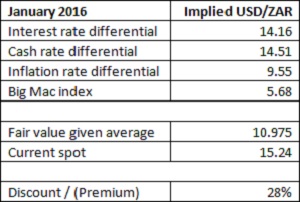

What is economic fair value of the USD/ZAR?

Rather than using one economic theory the table below reflects the average implied value of the Rand using four economic theories:

At current levels we are priced in line with the Russian Rouble. Whether this is fair or not, really depends on one’s view of the GDP growth forecasts, the ability of the government to be fiscally prudent, the commodity cycle, the carry trade, amplitude of the interest rate cycle and foreign investment.

The ZAR since 1971

Since the liquid trading of the ZAR, the currency has depreciated on average by 7.26% per annum. This is an important figure given that the depreciation has not been very far from the inherent depreciation that inflation and cost of debt naturally introduce to the currency.

These factors indicate that while it seems crazy that the USDZAR is at 15.24, it can be explained. Given that the listed investable universe in South Africa is less than 0.03% of the global market capitalisation, one needs to consider offshore investing more from a geographic stand point as opposed to a currency call. Forecasting the ZAR over the short term is impossible. While now it is oversold from a trader’s perspective, it can stay oversold for a long time. Conversely big money managers globally can flick the “carry trade switch” back on and the ZAR could easily move to fair value.

What the smart money thinks

With the JSE trading at lofty equity valuations and many money managers calling for companies to grow into their earnings, there is a strong thesis why a passive strategy in 2016 is not one that is going to deliver the best risk adjusted returns.

At AlphaWealth we have targeted equity like returns locally while only taking on one third of the market volatility. We achieve this by blending our selection of different hedge funds strategies in a single fund of fund called the Alpha Equity Hedge.

With annualised returns since inception in 2006 of 13% and a standard deviation of closer to 6% it is clear that the underlying managers are doing something right.

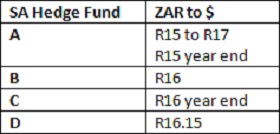

We surveyed the managers that make up our equity hedge strategy locally to gain insight as to their Rand predictions:

In summary

Targeting jurisdictions and opportunities where you can achieve the best risk adjusted return irrespective of the ZAR still remains the best capital preservation strategy.