The Nifty — and Not-So-Nifty — 15

For the better part of a decade, large technology companies have proven to be the ultimate equity investment. Indeed, investors have become so enthralled with them, that acronyms have been formed in conjunction with market indices. For example the FANGs, and the New York Stock Exchange (NYSE) FANG Index, among others.

The onset of COVID-19 and the ensuring economic lockdowns have seen these businesses being elevated to “antifragile” status, a designation previously reserved for US treasuries.

Coined by Nassim Taleb, antifragile is used to describe things that benefit from disorder, and technology businesses have undoubtedly benefitted from the chaos that ensued following economic shutdowns.

Much like the Nifty 50 in the 60s and 70s, today we can informally refer to 15 of the large cap technology companies as the Nifty15. For those who follow market history, the Nifty50 were a group of large cap stocks on the NYSE that were widely viewed as solid buy and hold growth stocks. This elite group of companies were credited with driving the bull market of the early 70s, before they came crashing down, leaving many casualties in their wake.

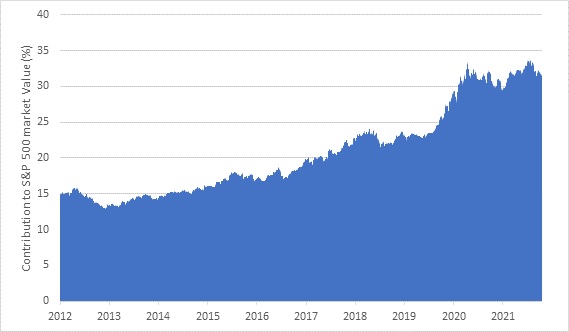

The Nifty15 can be traced back 10 years, with Facebook (now Meta Platforms) being the last of these companies to publicly list in 2012. The relative outperformance of the Nifty15 becomes evident in graph 1 below. In 2012, the Nifty15 contributed less than 15% of the total S&P 500 market value. Today, they contribute 32% of the S&P 500 market value. Over this period, the S&P 500 generated a very respectable cumulative return of 329%, while the Nifty15 overshadowed with a spectacular cumulative return of 832%!

Graph 1: Nifty15’s Market Value Contribution to Total S&P 500 Market Value

Source: Refinitiv Datastream, Old Mutual Wealth Private Client Securities

Frothy valuations, rising expectations

Today, the antifragile nature of these businesses is being questioned. Concerns around the US Federal Reserve becoming more hawkish than markets originally anticipated has caused anxiety within markets.

Compounding the issue are high valuations and several companies releasing results that are not meeting market expectations. This has resulted in a number of the Nifty15 companies’ market values declining significantly in a very short space of time.

On 3 February, following the release of results that did not meet market expectations, Meta Platforms’ market value declined by a whopping $232bn (or just over a quarter of its total market value), representing the largest ever daily market value decline for a single business.

However, given that market values rise over time, we are likely to see this value exceeded in the future. Table 1 highlights the six largest daily market value falls. Interestingly, they have all occurred over the last four years.

Table 1: Largest Daily Market Value Falls (as at 3 February 2022)

|

Stock |

Date |

Loss |

|

Meta Platforms |

03 Feb 2022 |

$232bn |

|

Apple |

03 Sep 2020 |

$180bn |

|

Microsoft |

16 Mar 2020 |

$178bn |

|

Tesla |

09 Nov 2021 |

$140bn |

|

Amazon |

30 Jul 2021 |

$130bn |

|

|

26 Jul 2018 |

$121bn |

Source: Bloomberg

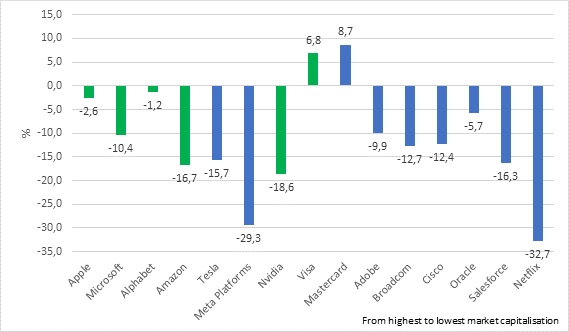

Despite its significant single-day decline in market value, Meta Platforms is not alone when it comes to disappointing year-to-date returns. Graph 2 shows the total return of the Nifty15 shares since the beginning of 2022. Those coloured green are included in the PCS Global Equity Portfolio either directly or indirectly in the case of Apple and NVidia. The re-rating of many of the Nifty15 becomes glaringly apparent.

Graph 2: Nifty 15 Year to Date Total Return

Source: Refinitiv Datastream, Old Mutual Wealth Private Client Securities

Importantly, not all companies have sold off to the extent of Meta Platforms or Netflix, and in fact, some of the Nifty15 companies have actually thrived. The prospect of economies returning to some form of normality, where consumers venture out and travel again, has benefited Visa and MasterCard, which both endured a difficult 2021.

What is also apparent from the companies that have held up relatively well (including Apple, Microsoft, Alphabet and Amazon, is that diversified revenue streams are not to be underestimated. Having started out as mono-line revenue businesses, many of these companies have pivoted into new revenue streams, either organically or through acquisitions. No doubt we will see further activity in many of the Nifty15 companies.

So what next? Do some of these businesses follow the path of many of the Nifty50 companies of the 70s; or is this just a bump along the road?

As long-term stewards of our clients’ capital, it is our job to ensure that we are invested in businesses that not only survive times of turbulence, but emerge stronger. Our investment philosophy and process ensures that we construct well diversified portfolios that invest in high quality companies and assets, and that we do not overpay for those investments. Importantly, we then exercise patience to allow our portfolios to benefit from the compounding ride of returns, despite the ebbs and flows during the short term.

As Cullen Roche once said: “the stock market is the only market where things go on sale and the customers run out of the store”.