The mighty dollar

September has been a rough month on local markets, and last week was particularly volatile with the rand losing further ground against major currencies. The JSE is on course for a monthly loss, led down by mining shares, retailers, and telecoms. The All bond index is also in negative territory, led down by losses on the longer end of the curve. Despite these losses, all local assets are still in solid positive territory year-to-date. Listed property in particular recovered from a poor start to the year to post good returns in the second and third quarters.

Globally, the picture is more mixed with flat returns from US equities in September, strong gains from the Japanese market, a stark divergence between the stock markets in Hong Kong and Shanghai (with the former down 4% and the latter up 5%). The MSCI Emerging Markets index is down almost 5% in dollar terms

The dollar makes a comeback

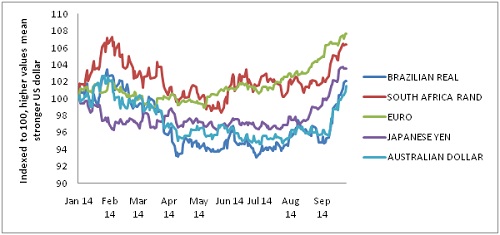

Two main themes run through the volatile market performance this month. First, the US dollar has surged against the euro, yen and the pound, as well as emerging market currencies (including the rand). The strength of the dollar reflects the improved fundamentals of the US economy and the consensus view that interest rates would start rising from mid-2015 (without choking off the recovery). At the same time, weakness in Europe and Japan point to interest rates remaining lower-for-longer with unconventional measures thrown in the mix. The Europeans and Japanese central banks won’t mind a weaker currency, as it will help stimulate exports and lift inflation from dangerously low levels. The US Federal Reserve (the Fed) won’t mind a stronger dollar as it contributes to lower inflation and thus does some of the work of monetary tightening for them.

The central bankers who mind weaker currencies are the members of those emerging markets with large external deficits. This includes South Africa, Brazil, Turkey and Indonesia. Weaker currencies can stoke inflation and thus make life difficult for central bankers who are torn between fighting inflation and supporting fragile economic growth. In Brazil, the central bank has erred on the side of fighting inflation and in South Africa, on the side of supporting the economy (interest rates are 11% in Brazil compared to 5.75% locally with inflation more or less the same).

South Africa and Brazil belong to a second unhappy group of countries that also includes Australia and Russia: commodity producers. This takes us to the second dominant theme on markets over the past month or so.

Commodity prices falling like lead

Global commodity prices are under severe pressure across a broad spectrum of products. The oil price has fallen 13% in 2014, despite a cocktail of geopolitical crises centred on major oil producing regions. Iron ore has fallen 30% since the start of the year. Copper is down 8%, and, yes, lead prices are down 7%. The platinum price is 3% lower despite the main producers being out of action for much of the year due to the strike. Soft commodities – wheat, maize, sugar, and cotton - have also fallen substantially in dollar terms this year (though unfortunately for caffeine dependents, coffee prices have risen sharply).

Since commodities are priced in US dollars, the strong dollar tends to lead to lower commodity prices. But the broader problem is the age old issue with commodities: there is a huge lag between supply and demand. When demand is rising, producers cannot immediately increase output. But the time they can increase output, spurred on by high prices, demand has often stabilised or started falling. Currently we are in such a phase, where extra capacity is created based on projections of ongoing rapid growth of the Chinese economy. China’s economy, however, is clearly settling into a lower growth range of 6% - 7% (if things go well) rather than 9% - 10% per year. Ongoing weakness in Europe and Japan, and below trend growth in other large emerging markets (such as India and Russia) is also contributing to lower growth. Falling dollar commodity prices is of course good news for the Fed and US consumers.

Implications for South Africans

South Africa is in the unfortunate position of being very dependent on the actions of the US Fed (which will determine the capital flows we need to fund our large current account deficit) and the Chinese authorities (who need to decide whether they will allow their economy to slow down, or to stimulate it further). This means our own Reserve Bank cannot focus purely on domestic factors when setting interest rates.

From a long term investors’ point of view, a bad month is fairly insignificant. The bigger concern is that valuations do not provide much of a margin of safety on local equities, but these are still priced to potentially deliver real returns in excess of cash or bonds over the next few years. Local equities are also highly correlated to global equities. Being properly diversified remains a source of comfort. The best example of this is how the foreign component of most balanced funds at 25% benefits from a weak rand. Having a long-term view is also important. Just look at the 15 year annual total real return from local equities – 11% – despite numerous corrections and a serious crash during this period.

Chart 1: Various currencies against the US dollar in 2014

Source: Datastream

Some good news ahead

The SA Reserve Bank’s composite leading indicator rose by 0.3% in July, the third consecutive monthly increase. Year-on-year, the leading indicator rose 0.5%. As the name suggests, the composite leading indicator is a combination of 11 economic indicators that give an indication of whether economic activity will improve or deteriorate over the following 6 to 9 months. This suggests that the economy will pick up a bit of speed in the coming months, provided that there are no further serious disruptions in the form of strikes and electricity black-outs. But there is also nothing to get particularly excited about. South Africa’s underlying growth trend remains around 2% a year in real terms or around 8% including inflation. The economy is therefore not falling over, but it is fragile nonetheless. The main hope for a positive growth surprise is for non-commodity exports to benefit from the weaker rand and US-led global growth.

Export prices up slightly

According to new StatsSA data, export prices rose 4.8% year-on-year and 0.5% month-on-month in July. It was the first monthly increase since March. While commodity export prices are all sharply down as can be expected, agricultural items, vehicles, chemicals and certain types of machinery showed promising price increases. The same data shows that the rapid rise in import prices due to the weak rand has been tapering off. But at 19.5%, annual growth in import prices still exceeds that of export prices. It will thus still be an uphill battle to close the trade deficit.

From an inflation point of view, import price growth is obviously still a concern, and the potential for further rand weakness will keep members of the SARB’s Monetary Policy Committee (MPC) up at night. However, the pass-through remains low. For instance, the latest data show that imported inflation of clothing running at10%, while at producer level, clothing inflation is 7.9%. At consumer level, in other words on the shelves of retailers, clothing inflation is only 5.5%. At each step of the value chain, companies are sacrificing some margin to maintain market share in a weak economy.

Producer inflation lower

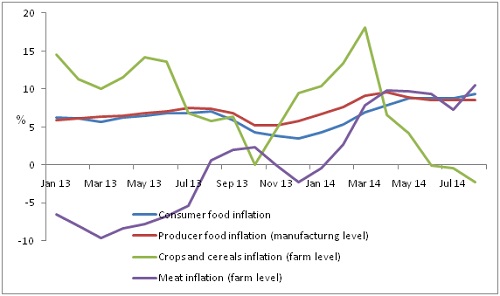

Overall producer prices rose by 7.2% year-on-year in August, down from 8% in July and below market expectations. Producer prices give a reasonably good indication of what to expect from consumer goods prices in months to come, so this drop would provide some comfort the MPC. Food inflation remained more or less unchanged at a manufacturing level, which means that we will probably have to wait a bit longer to see lower food inflation at the consumer level.

At the agricultural level, prices of maize, wheat and other cereals are falling, while vegetable prices are rising very slowly (global crop prices are also falling). However, meat prices rose by 10.5% year-on-year and 5.6% month-on-month at the farm level. South Africans who celebrated Heritage Day with a braai paid significantly more for their meat compared to last year.

Chart 2: Food inflation at various stages of production and consumption

Source: StatsSA