The local fund management industry in numbers (part 2) : Investment teams, decision-making, co-investment and ownership

Leigh Köhler, Head of Research at Glacier by Sanlam.

Collective investment schemes (unit trusts) provide so many of us with access to some of the best investment minds in the business, but deciding which one to invest in is not an easy task. Not all of us have the privilege to interact and engage directly with the fund managers who make the investment decisions that ultimately drive the performance of these funds. Fortunately, Glacier Research conducts in-depth analyses of fund managers both locally and globally. We use our findings to support financial advisers to make better investment decisions for their clients. These findings are based on sound quantitative and qualitative research, and hopefully prevent them from simply basing fund selection on brand (which is often a proxy for the size of advertising budgets) or industry awards (purely awarding past performance, which as we all know, is not an indication of potential future performance). Glacier Research provides a pivotal differentiator for the Glacier platform and provides supporting financial advisers with meticulous investment insights-based, rigorous and disciplined research. In 2017, the team conducted 172 due diligence meetings with investment managers – coverage that not many manager research teams can match.

In our previous article, we focused on manager characteristics such as age, tenure, undergraduate university attended, whether they hold a CA, CFA and/or MBA qualification, their investment style and company affiliation. This work produced some fascinating insights, such as 46% of all fund managers obtained their undergraduate degree from UCT and the average age of fund managers is 47.

This paper examines investment team size, team diversity with a focus on female and employment equity representation, co-investment, share ownership, and decision-making (intuition vs. model and individual vs. team).

The data set was collected over the course of 2017 and was comprised of 146 funds across the ASISA Multi Asset Low Equity (LE), Medium Equity (ME), High Equity (HE), Flexible Equity (FE), and General Equity (GE) categories. We selected these categories because they have attracted the most assets over the last few years. The sample excluded all multi-managed funds and fund of funds. LE represented 21%, ME 10%, HE 28%, FE 21%, and GE 63% of the funds. The HE category is the largest by AUM, attracting 47% of AUM, while the ME category is the lowest, attracting 4% of AUM. The study used five-year performance figures (measured by cumulative net returns) and risk (measured by standard deviation) figures for the period 1 January 2012 to 31 December 2016. It is important to note that for the purposes of the exercise, overall performance and risk were averaged across fund categories depending on the fund manager characteristic in question.

Investment team size

The investment team plays a very important role in fund management and can be defined as individuals who are responsible for the research (cash, bonds, property, equity and derivatives) that informs instrument selection and portfolio construction of the fund manager. The more resourced an investment team, the wider the breadth and coverage of research. This is particularly relevant to bottom-up fundamental analysis. However, with improving screening technology and the advent of passive investing, artificial intelligence and machine learning, the relevance of team size has been brought into question. Our study shows that the average team size supporting the fund managers in South Africa is 11 team members. Therefore, one could define an investment team with less than 10 investment professionals as relatively small, and larger than 10, relatively big. Team size is an important consideration when forming an opinion about a fund, and depending on the mandate and investment opportunity set, should be considered when selecting a fund.

The average team size of funds in the LE category is the highest at 13.4 and the lowest in the FE category at 7.2 investment professionals. This observation makes sense as Multi Asset Low Equity (LE) funds typically comprise of teams focused on both fixed income (60% or more of the fund) and equity (maximum of 40% of the fund), and these are often separate teams in the fund management business. Multi Asset Flexible Funds are typically more equity-centric, predominantly utilizing equity teams, with very little fixed income focus.

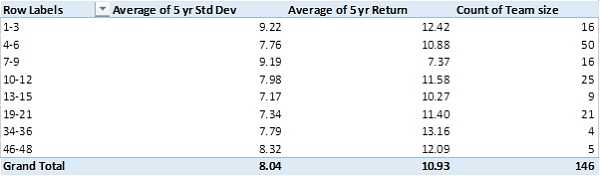

Table 1: Team size

50 funds within the sample are supported by team sizes between four and six investment professionals. It seems like larger teams generally perform well, noting that teams between 34-36 members generated the best average five-year return at generally lower levels of risk. However, it is important to note that only nine funds in the sample are supported by teams larger than 34 individuals. Another interesting observation is the impressive performance of teams between one and three individuals, generating an average return of 12.42% over five years. These results do not provide a clear indication as to the relationship between team size and performance, but they do seem to provide some evidence that performance of large investment teams is not necessarily constrained by their size. There is a school of thought that exists within the investment industry that large teams tend to slow down the investment process (idea generation to portfolio construction) and ultimately result in underperformance. The results of this study show that this is not necessarily the case.

Investment team diversity

One of the more interesting results from the team analysis is the diversity composition of South African fund management teams. The average female representation in investment teams is only 18%, while the average employment equity (race) representation is a slightly higher at 31%. While investment team profiles are slowly changing, our study reveals that the South African fund management industry is still dominated by white men.

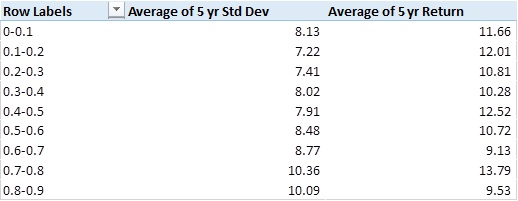

Table 2: Employment Equity (EE) %

While it is very difficult to gauge any clear observations from the above results, it is clear that teams with EE representation between 70%-80% produced the highest five-year returns, but at the highest risk levels as well. From the results above, it seems that the best risk-adjusted (relatively high performance at lowest risk levels) performance is produced by teams represented by 40%-50% EE. These figures seem to support the investment merits of team diversity.

Decision-making

The final portfolio construction decision is an interesting fund manager characteristic in the South African asset management industry. The decision is either made:

1) individually or team-based (supported directly by one or more investment professionals, either through a co-management or multi-council process); or

2) driven by a model, intuition or a combination of both.

The data analysis suggests that 68% of the funds’ final portfolio implementation decisions are team-based with an average of three investment professionals directly influencing the final portfolio construction decision, while 27% make use of individual-based decision-making and 5% make use of both.

Table 3: Decision-making: individual or team (1)

Team-based decision-making has shown to outperform individual decision-making over the five-year period. It also seems that teams were more willing to take on risk in achieving these returns. Glacier Research’s fund manager selection process typically gravitates towards funds managed by teams where key fund manager risk is mitigated. It is our belief that ‘two (or more) heads are better than one’ in terms of overall performance consistency, key-man risk mitigation and succession planning.

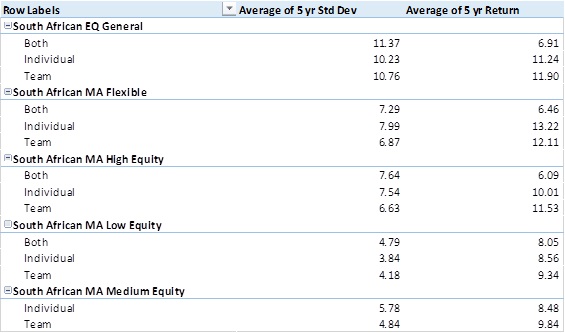

Table 4: Decision-making: individual or team (2)

When analysing the data and taking categories into account, it is evident that decision-making that combines both individual and team has generated the lowest returns, regardless of the fund category. Obtaining clarity around decision-making is a critical component in our due diligence interviews with fund managers. We look for a clear indication of whether decisions are team-based or individual-based. It is evident from the numbers that when there is a lack of clarity in this regard (combination of both individual and team), it may have an impact on overall performance.

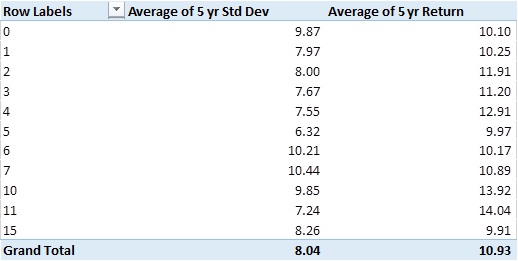

Table 5: Decision-making: support

The decision-making support characteristic speaks to the number of investment professionals (typically analysts) that provide support to the decision-making process. The data suggests that where final decision-making included 10-11 investment professionals, the best five-year returns were experienced, at relatively lower levels of risk. The data suggests that team size may count when considering potential future returns and risk. Intuitively, this makes sense in active management – the larger the team, the wider and deeper the research efforts.

Our findings also show that only 3% of fund managers make use of only their ‘gut-feeling’ or intuition when making the final portfolio construction decision, while 50% rely on models and 47% use a combination of both intuition and models.

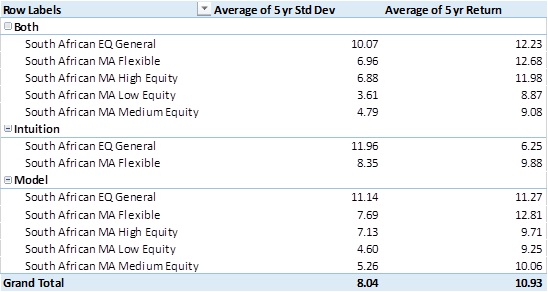

Table 6: Decision-making: model or intuition

The data suggests that where managers used a combination of both models and intuition, they yielded superior five-year performance at the lowest levels of risk. This observation mostly holds, regardless of fund category.

Co-investment: betting on your own horse

Fund managers manage money on behalf of their clients. However, some invest in the funds that they manage while others don’t. Investing alongside clients is termed ‘co-investing’ and higher levels of co-investment are often associated with higher levels of alignment of interest between fund manager and client – and vice versa. A higher level of co-investment is viewed by Glacier Research, as a favourable fund manager characteristic.

Our study shows that 85% of fund managers co-invest in the funds that they manage, but 62% invest less than half of their discretionary wealth in their funds. So while the number of managers that co-invest suggests client interest alignment, the level of co-investment may suggest otherwise. 26% of fund managers invest more than half of their discretionary wealth in the funds they manage, 3% invest all their discretionary wealth in the funds they manage, while 10% of the sample do not disclose the level of co-investment.

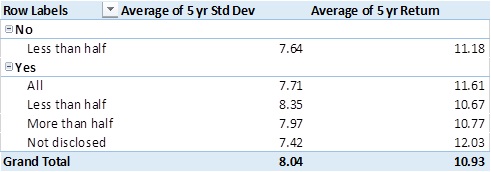

Table 7: Co-investing

These results reveal that fund managers who have not disclosed their levels of co-investment have performed the best over five years. However, if one isolates the observation only to those managers who do co-invest, it is the managers who co-invest all their discretionary savings into the funds that they manage, who have performed the best and at the lowest levels of risk. Very interestingly, managers who do not co-invest, have produced good returns at relatively low levels of risk.

Company share ownership

Fund managers are integral employees of investment companies and are often incentivised with company share ownership. However, not all fund managers have shares in the fund management company. Company ownership is often associated with higher levels of alignment of interest between fund manager and asset management company.

Our findings suggested that fund manager alignment with the asset management company is high, with 81% of managers owning shares in the company.

Table 8: Share ownership

These results indicate that fund managers who own shares in the asset management company, have produced superior returns relative to managers who do not own a stake in the company. Very interestingly, these managers also seem more willing to take on risk than managers who do not own shares. Share ownership is an important consideration for Glacier Research, and the analysis seems to confirm the importance of this fund manager characteristic.

Conclusion

There are many ways to compare one fund manager with another. Traditionally, quantitative factors such as performance and risk are used to create comparison benchmarks. These are useful tools, but limited in what they reveal. At Glacier Research, we hold the belief that a much broader and detailed view of fund managers is necessary to make the picks that underpin clients’ investment prosperity. The age, tenure, undergraduate institutions attended, CFA, CA, and/or MBA qualifications, investment style or company association, team size, team diversity, decision-making, co-investment and share ownership are important factors that assist us in benchmarking fund managers.

Conducting asset manager research goes far beyond just looking at the performance numbers. It is said that past performance is not a predictor of future performance, and if this is true, then what else can be considered to select and blend funds that will consistently outperform in the future? We believe that the answers lie in the qualitative detail, and this is why Glacier Research spends countless hours assessing fund managers. We aim to extract unique qualitative insights that will help South Africa’s financial adviser industry to make better investment decisions for their clients.