The investment case for emerging markets?

Adrian Saville, Chief Executive at Cannon Asset Managers

Investment manager and author Mebane Faber recently argued for “investing entirely in emerging markets (EMs) for the long haul”, reasoning that the endemic features of these markets make a compelling case for the long run.

To start, EMs are home to large and growing populations that drive household and business spending. As many as 6.4 billion people, or 86% of the world’s population, live in EM countries. China and India alone are home to 37% of the world’s population, and by 2030 the World Bank estimates that as many as one in five consumers will live in Africa.

Additionally, EM populations have a young demographic make-up compared to developed markets (DMs), with positive implications for human capital, productivity growth and business competitiveness. The median age in Japan is 48 years old, whereas the median age in the Philippines is 24.

Along with rapid market growth, EMs are also the birthplace of innovative and disruptive business models. For example, China’s Ant Financial has built the world’s largest money-market fund in five years and achieved a valuation of $150 billion, while India’s Narayana Health performs heart surgeries – with first-world results – for $800.

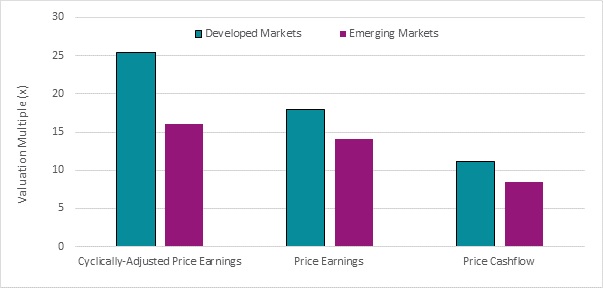

Further to this, valuations are much more attractive in EMs than DMs.

Source: Thomson Reuters Datastream (2019

Caveats to the EM argument

But things are seldom as simple as they first appear, and closer analysis raises several caveats. As Stephen Arnold of Aoris Investment Management cautions, the above arguments are of no consequence if economic growth and demographic drivers in EMs don’t translate into growth in company earnings.

Conventional wisdom posits that superior economic growth produces superior growth in company earnings which, in turn, translates into corporate prosperity. Put simply, faster economic growth should mean faster company growth, and vice versa.

Yet, at an index level, inflation-adjusted earnings per share (EPS) have declined in three of the five BRICS over the past ten years. In the case of Brazil, earnings have halved. And in nine of the fast-growing Next 11 (N11) countries, the numbers are as disappointing, with earnings growth having lagged economic growth, as measured by the “growth gap”.

Further emphasising the disconnect, EM economies have grown at 4.9% per annum over the last ten years, as compared to 1.4% produced by DMs. However, of the 16 BRICS and N11 countries, only Nigeria and the Philippines have recorded real earnings growth faster than the 3.9% DM average.

|

A Decade of Economic Growth and Earnings Growth: 2009-2018 |

|||

|

|

|

|

|

|

|

Real GDP (% p.a.) |

Real Earnings (% p.a.) |

Growth Gap (% p.a.) |

|

|

|

|

|

|

Brazil |

1.2 |

-7.0 |

-8.2 |

|

Russia |

0.7 |

-3.2 |

-3.9 |

|

India |

7.1 |

-2.3 |

-9.4 |

|

China |

8.1 |

0.8 |

-7.3 |

|

South Africa |

1.6 |

0.4 |

-1.2 |

|

|

|

|

|

|

Pakistan |

4.0 |

-1.4 |

-5.4 |

|

South Korea |

3.1 |

-2.4 |

-5.5 |

|

Turkey |

5.6 |

1.1 |

-4.5 |

|

Bangladesh |

6.3 |

-5.3 |

-11.6 |

|

Egypt |

3.5 |

3.8 |

0.3 |

|

Indonesia |

5.4 |

1.1 |

-4.4 |

|

Mexico |

2.2 |

-4.5 |

-6.7 |

|

Nigeria |

4.5 |

5.3 |

0.8 |

|

Pakistan |

4.0 |

-1.4 |

-5.4 |

|

Philippines |

5.8 |

4.0 |

-1.8 |

|

Vietnam |

6.0 |

-5.4 |

-11.4 |

|

|

|

|

|

|

BRICS |

3.7 |

-2.3 |

-6.0 |

|

Next 11 |

4.6 |

-0.5 |

-5.1 |

|

EM |

4.9 |

-1.2 |

-6.1 |

|

|

|

|

|

|

DM |

1.4 |

3.9 |

2.5 |

Source: World Bank, Thomson Reuters Datastream and Cannon Asset Managers (2019)

Evidently, as Stephen Arnold notes, the relationship between economic growth and market EPS growth does not assert itself equally. Additionally, adjusted for inflation, earnings in nine of the 16 EMs are lower today than they were ten years ago – notwithstanding that EM economies grew materially faster than DM economies.

For at least four reasons, the causal link between economic growth and equity returns should not be taken at face-value.

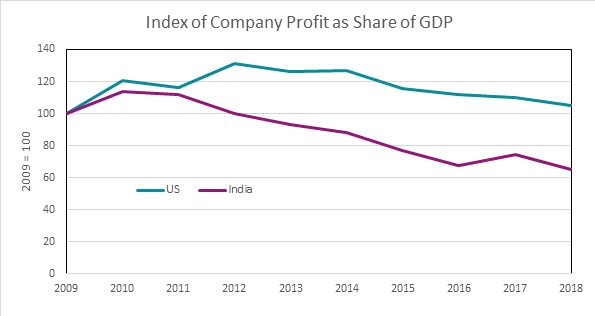

First, the ratio of corporate profits to GDP changes over time. For instance, the profits of all companies in the US relative to GDP rose after the global financial crisis and have remained relatively buoyant (above 100). By contrast, although profit share in India also lifted after 2009, the profitability of Indian companies has been far more erratic, falling to nearly half the 2010 peak.

Source: FRED, Economic Times of India (2019)

Second, companies listed in one country often do business outside of their local market, particularly larger listed EM companies – just consider the examples of British American Tobacco, Naspers and Richemont. As a result, the home economy has very little to do with these companies’ earnings.

Third, while a country’s stock exchange often resembles the country’s economy, many EMs remain heavily commodity based, which pins domestic firm performance to global growth rather than domestic growth. Brazil, Egypt, Nigeria and Russia are a few cases in point. Additionally, markets in these countries are often immature. For instance, the Rwandan economy has grown at 8.1% per annum since 2001, but has just eight companies listed on the stock exchange – none of which are in the agricultural sector that makes up 40% of its GDP.

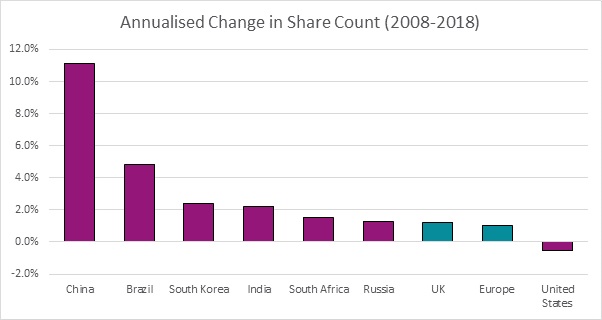

Finally, investors should be concerned with per share earnings, and not company earnings, which poses one last hurdle: dilution. EPS growth relies on net profits growing more quickly than the number of shares in issue. But a large proportion of listed EM businesses are in capital-intensive sectors such as resources and financials, or are young and growing off low bases, which translates into the dilution of profits from share issuances.

Ultimately, you may feel bullish on the Chinese economy, or the prospects of a recovery in Brazil. But your view on an economy needs to accommodate a range of elements before it has any real bearing on your expectations for EPS growth from your investment – counterintuitive though this may feel.

The past decade demonstrates that if you want economic growth, you will find it in EMs; but if you want earnings growth, you will find it in DMs. As compelling as the economic cases might be, investors need to examine the more carefully identified investment drivers – and not the more easily told EM investment narrative.