The impact of higher global bond yields

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

How worried should we be about the recent jump in developed market bond yields? Global bonds sold off after a string of central bankers, most notably the ECB’s Mario Draghi, discussed the prospects of reducing monetary stimulus at a recent conference in Sintra, Portugal. Bonds pay a fixed coupon and therefore a decline in the price increases its yield (and vice versa). There are a couple of issues to consider. Firstly, will central banks follow through with tightening policy, or are markets overreacting? Secondly, is the jump in yields large enough to derail global growth? Thirdly, what does it mean for equities? Lastly, what does it mean for South African financial markets and monetary policy, local bonds and the rand, given that we have benefited from being a high-yielding country?

Will they or won’t they?

It is important to remember that most central banks have a committee that establishes monetary policy. These committees often have opposing views and these debates can spill out into public view. (This is very common in the US, less so in Europe, and almost never happens in South Africa.) Some central bankers are keen to return interest rates to more ‘normal’ levels, arguing that emergency measures are no longer needed, almost ten years after the start of the global financial crisis (in August 2007). Ultimately, policymakers need to work out how to balance two seemingly conflicting pieces of evidence: stronger growth (and falling unemployment) against stubbornly low inflation.

The curious thing about the supposedly newfound central bank hawkishness, given the fact that most central banks target inflation, is the lack of inflation. For instance, the Canadian central bank hiked last week despite core inflation of 0.8%, while its inflation target is 2%, focusing instead on a strong economy and frothy housing market.

Inflationary pressures remain weak globally. June’s US inflation report was weaker than expected. Producer inflation in China – the world’s factory – declined in June after a hopeful increase in prior months. Combined with a marginally stronger yuan against the dollar, this puts downward pressure on global goods prices. In the background, wage growth in the developed world is constrained because of two big long-term trends: technology (including automation) and competition from poorer economies.

Growth not at risk yet

Could higher yields derail global growth? To the extent that the higher yields reflect expectations for solid growth and hence less need for central bank stimulus, no. As corporate bonds price off the government curve, funding costs for firms will rise marginally but this will only be for new debt. A much larger move would be required to cause concern over growth. But if central banks persist in tightening policy it would eventually put borrowers under pressure.

There have been four big synchronised sell-offs in the global bond market since the end of the financial crisis, with the most recent benign by comparison. The first, in late 2011, coincided with S&P downgrading the US after the debt ceiling debacle, and the first rumblings of the European fiscal crisis. The second was Ben Bernanke’s Taper Tantrum in May 2013, when the US Federal Reserve chairman at the time noted that quantitative easing might be pared back. Reasons for the third, in April 2015, are harder to pinpoint, but was centred on Europe and followed yet another episode in the Greece saga after a strong rally in bonds. Meanwhile in America, investors were looking ahead to the first Fed rate hike. The fourth happened after the US election in November, when investors priced in faster growth and higher inflation. Interestingly, after each of these big sell-offs, yields eventually ended up moving even lower. A year after the 2015 sell-off, German yields fell into negative territory.

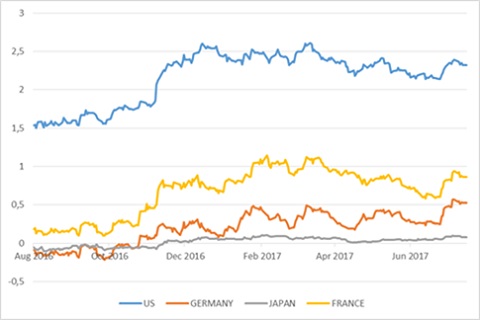

By late last week the sell-off in global bonds had run out of steam, following the soft US inflation report and Fed Chair Janet Yellen’s Congressional testimony where she said that the Fed would adjust its policy stance if inflation didn’t pick up as expected. US yields are still below the peak level for the year, while German yields are still at the highest level in a year. Japan’s yields are also somewhat higher, but since the Bank of Japan has committed to keeping the 10-year yield around 0%, traders are very careful to bet against an institution that can print yen.

Equities can stomach higher bond yields

Global equities (lead by the US) rallied from 2009, initially on the basis of a recovery in profits. Since late 2011, the rally has been driven by a rising price:earnings ratio. The forward PE multiple on the MSCI World Index increased from 9 to 16, which means that investors are now prepared to pay 16 dollars for every dollar of annual earnings, while a few years ago they were only prepared to pay nine dollars. This multiple expansion reflects greater optimism and risk appetite (as the fear of a repeat of the 2008 crisis receded), but it also mirrors low interest rates. Technically speaking, a lower interest rate increases the discounted present value of future cash flows. In much more simple terms, low bond and cash yields made equities an attractive alternative although they are more volatile.

In most developed markets, equity earnings yields – retained earnings plus dividends divided by price - are still above bond yields, making equities relatively attractive. In the US, the earnings yield on the S&P500 is 4.5%, meaning bond yields would have to move up a lot to become attractive relative to equities. Historically, bond yields have typically exceeded earnings yields.

Impact on emerging markets and South Africa

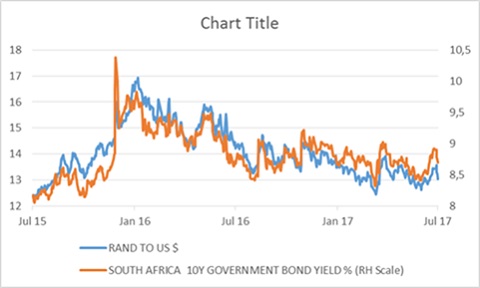

The benefit of South Africa’s open, deep and liquid bond market is that Government has ready access to funding at reasonable interest rates. However, with foreigners owning more than a third of outstanding rand-denominated bonds, and facing no capital controls, our yields will be priced off global yields. Since early 2016, South Africa benefited from a search for yield. Despite political uncertainty and credit ratings downgrades this year, foreigners bought South African bonds as part of a big push into emerging markets, keeping local yields down and supporting the rand. As perceptions of the direction of global monetary policy shifted, so has the rand. It weakened as global bond yields rose, but strengthened again late last week after the benign US inflation report and Yellen’s fairly dovish comments.

In terms of valuation, emerging markets, bonds, equities and currencies are still attractive relative to developed markets, despite the outperformance over the past year. This is because of the massive declines from 2010 to 2015 (roughly speaking). The rand is a case in point. The real trade-weighted exchange rate is still 15% below its long-term average.

Unlike the US and other developed markets, local bond yields are much higher than equity yields, reflecting high recent inflation, high short-rates and mistrust over Government’s fiscal policy. Local bond yields are also high in global terms. Therefore within South African assets, bonds are most attractively priced.

Local policy implications

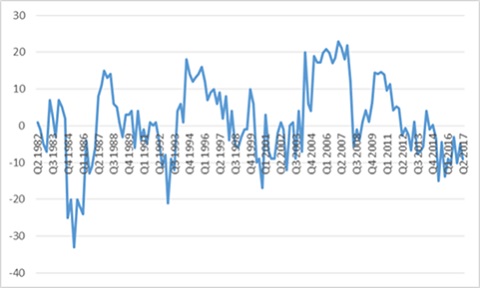

Finally, in terms of South African monetary policy, the case for rate cuts is still strong. The inflation outlook is declining, even with some recent rand softness. The economy – especially the consumer – is crying out for some relief. The BER/FNB Consumer Confidence Index spent a record 12th consecutive quarter in net negative territory in the second quarter. However, if the global monetary cycle is indeed turning, the SARB could be hesitant. This means stimulus would have to come from elsewhere. Finance Minister Gigaba’s 14-point plan to lift growth does not contain anything dramatic, but at least acknowledges that policy uncertainty is a problem. The plan attempts to address this with the responsible ministers with clear deadlines. There is also an acknowledgement that governance at State-Owned Enterprises (SOEs) needs attention. The door is also open for private sector participation, off-loading non-core assets and properly costing SOEs developmental mandates. What is worrying, though, are the comments around Eskom’s ‘hardship’, which indicate a big electricity tariff hike could be in the works.

Chart 1: 10-year government bond yields for major economies

Source: Datastream

Chart 2: South African bond yield and rand-dollar exchange rate

Source: Datastream

Chart 3: FNB/BER Consumer Confidence Index

Source: Bureau for Economic Research