The Home of the Brave

Today sees the swearing in of Donald Trump as the 47th US president. It is an odd American tradition that the inauguration takes place more than two months after the election, resulting in an awkward interregnum during which outgoing president Joe Biden was in office but not really in power. It could’ve been worse, however.

Prior to 1936, the inauguration was in March. It meant that for five excruciating months between November 1932 and March 1933, during the deepest depths of the Great Depression, the country was effectively leaderless. Herbert Hoover, the outgoing president, spent most of this time trying to frustrate the transition to his successor Franklin Roosevelt. It is Roosevelt who in turn introduced the much-copied idea of ‘the first 100 days’ of his term as an important initial period of action, and it was indeed laying the groundwork for the eventual recovery.

Many investors view Trump’s first 100 days with some trepidation. He promised many things on the campaign trail, but it is not clear exactly what, when and how they will be implemented. It certainly muddies the waters when trying to think about the year ahead for global markets (next week we’ll focus on China and the following week on South Africa).

It would, however, be a mistake to assume that Trump is the only thing that matters. He can certainly cause market volatility in the short term, but larger economic forces (including geography, technology and demographics) dominate in the end and the impact of US presidents on the economy has historically been overstated. Other policymakers also matter, notably the Federal Reserve, headquartered a few blocks away from the White House.

Fine, thanks

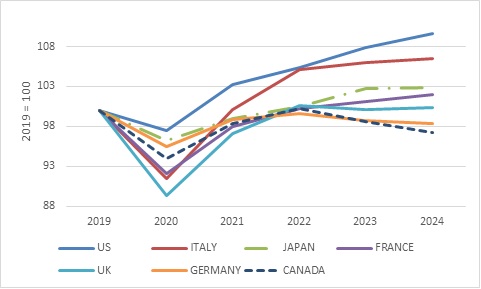

The irony of Trump’s ‘Make America Great Again’ slogan is that America’s economy is in good shape at the moment, certainly compared to other major economies. Very much unlike Roosevelt, Trump enters office with an unemployment rate of 4.1%, near multi-decade lows, while GDP growth has been running around 3% over the past two years, well above estimates of its long-term potential growth rate just below 2%. The booming US stock market has handsomely outperformed the rest of the world, not just during Biden’s term, but over the past decade. And then there is the dollar, which is trading near 20-year highs on a trade-weighted basis.

Chart 1: Real GDP per capita of G7 economies

Source: OECD

Now clearly, the economy is not working for everyone, otherwise the Democrats would have won the election. Most people were upset about high prices for groceries and fuel, as was the case across the world. Lower inflation, a slower increase in prices, did little to change the mood. Lower-income families do not benefit from surging equity markets, and for many young people, the dream of buying a house is out of reach due to elevated mortgage rates and high house prices.

Growth risks

Looking ahead, there is bound to be a lot of noise, but two fundamental questions need to be top of mind: what is the risk of a US recession, and what is the risk of the Fed hiking rates again. Either of these two outcomes will cause a big bear market in global equities. Almost everything else will just be volatility.

Starting with the first question, solid current growth rates of activity, sales, income, and employment together with healthy private balance sheets and company profitability make it hard to see a recession in the near term. It is likely, however, that growth would slow naturally from such strong levels.

Click here to read more...