The good news edition

For a country always in need of cheering up, last week’s news of better-than-expected economic growth was most welcome.

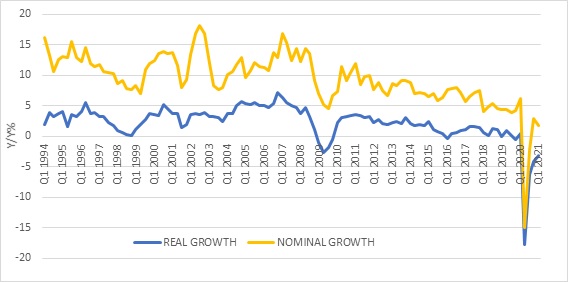

StatsSA data showed that the economy grew by 4.6% after inflation in the first quarter on a seasonally adjusted and annualised basis. This was not just better than the consensus forecast of 2.5%, but even better than the most optimistic projections. As a result, economists are upgrading their forecasts for 2021 full-year growth from 2020’s record 7% contraction in gross domestic product.

Nonetheless, compared to a year ago, the economy was still 3.2% smaller in real terms, and will still take several quarters to return to pre-pandemic levels.

In terms of the details at the sector level (the production side), mining, and the finance, the business services and real estate sector were the biggest contributors to quarterly growth. However, mining is the only large private sector that has recovered to pre-Covid levels of real activity (agriculture has been buoyant but it is small at around 2% of GDP).

Chart 1: SA economic growth, year-on-year %

Source: StatsSA

Spending again

The surprise factor largely came from household spending, the biggest component of economic activity when measured from the expenditure side. It grew 4.7% at an annualised rate in the first quarter. Compared to a year ago, the level of household spending was 1.3% lower in real terms but marginally bigger when inflation is added back. Spending patterns have diverged substantially, though. Spending on durable goods (such as cars and furniture) was 4.5% higher than a year ago in real terms, while spending on semi-durables (such as clothing) was 11% lower. Spending on non-durables (food) and services have almost recovered to year-ago levels.

Household finances have been much more resilient than feared throughout the pandemic, despite the loss of some 700 000 formal sector jobs and even more in the informal sector (which is by nature harder to measure). Additional government social grant payments also helped, but came to an end. The biggest driver of better-than-expected household spending is that those who have kept their jobs have done reasonably well.

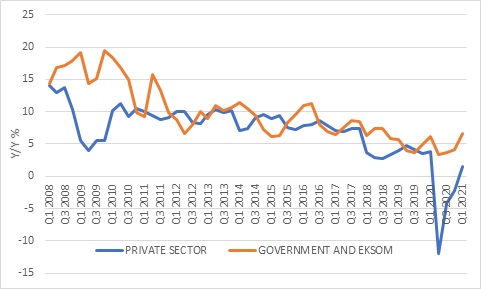

The economy-wide wage bill (employee compensation) has surpassed pre-Covid levels, up 3.2% from a year ago in the first quarter (this number is reported in nominal terms). While the private sector portion of this fell sharply last year due to a combination of job losses and salary cuts, the public sector wage bill continued to grow throughout. Current wage negotiation at national and local government level and also at Eskom and Transnet should be seen against this background. So while the recovery in household incomes hides the massive divergence between the haves and have-nots, and the winners and losers from the pandemic, it remains the ultimate driver of consumer spending.

Chart 2: Nominal employee compensation growth, year-on-year %

Source: StatsSA

Consumers also benefit from lower interest rates. New borrowing activity is still muted so most of the boost comes from savings on servicing existing loans. At the end of the fourth quarter, the portion of after-tax income that households spend on interest payments was at a 15-year low of 7.7%.

Third wave meets stage 3

The biggest obstacles to economic growth over the next few months are the third wave of Covid cases (possibly followed by a fourth wave) and electricity shortages, as last week’s shock return to stage three load-shedding reminded us.

Confirmed daily new Covid-19 cases are now rising at an average of 5 000, making the vaccine roll-out all the more urgent. While the infrastructure to get jabs in arms seems to have been set up quite efficiently, there simply aren’t enough vaccines in the country yet.

While further restrictions on gatherings and movement are possible, we are very unlikely to see a return to the very strict lockdowns that crashed the economy in the second quarter of last year. Consumers and businesses have also adapted to the new world. Studies from the IMF and others show that the economic impact of Covid-19 worldwide was due roughly 50-50 to government-imposed restrictions on the one hand, and the voluntary actions of consumers to avoid the virus on the other.

Electricity shortages are therefore a bigger threat to the economy, including the booming mining sector. Eskom’s aging fleet of power plants are prone to breakdowns and this is not going to change despite the improvement in the utility’s overall management, while the design and construction flaws at Medupi have clearly not been sorted out yet.

Reform lights go on

However, there is now light at the end of the tunnel (load-shedding always brings out the puns). President Ramaphosa’s unexpected announcement that companies will be allowed to produce up to 100MW of electricity for own use without going through the lengthy licensing process is a major step forward in five respects.

Firstly, companies that can produce their own power can maintain production even when there is load-shedding. Secondly, by reducing the demands on Eskom power, they make load-shedding less likely for everyone else. Thirdly, it will require billions to be spent, a boost to investment levels and construction activity, and by implication job creation. Four, most if not all the investment will be in solar and wind energy, reducing the carbon footprint for individual companies and over time, for South Africa as a whole. South Africa is one of the most carbon-intensive economies on earth, and this needs to change for its own sake, but also because of the risk of being shut out of key markets as global climate concerns rise.

Finally, there is no reason why this could not have taken place a year or two ago, and it seemingly took the crisis of stage 3 blackouts to get us here. But now that we are here it is positive for reform momentum in general, and particularly allowing the private sector to play a greater role in key network sectors (as also seen with the announcement of a new majority shareholder in SAA). This can change the narrative around the prospects for the local economy and the government’s commitment to making growth-enhancing policy changes which can help raise business confidence.

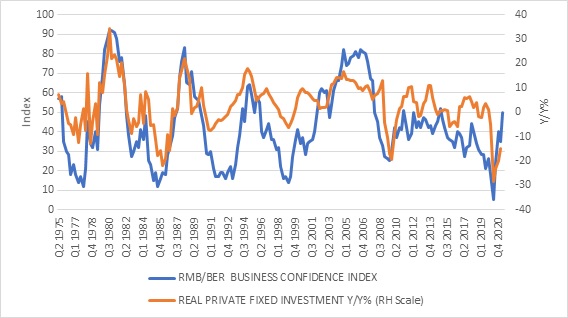

This is important because the one big negative from the GDP report was the decline in fixed investment in the first quarter even as other forms of spending rose strongly. Public sector fixed investment is severely constrained by financial and operational problems and has been on a downturn for several years. Private fixed investment has also been declining, held back by low confidence and weak profitability.

Confidence improving

This is starting to show signs of improvement that could get a further boost from sensible policy changes. The long-running RMB/BER Business Confidence Index showed a promising jump to 50 index points in the second quarter. For the first time in three years, half the respondents in the survey were positive about business prospects.

Chart 3: Business confidence and investment

Source: BER and StatsSA

While commodity prices are a major boost for the economy, longer-term growth will depend on raising confidence levels and greater investment spending by the private sector. Commodity prices are cyclical and the current rally will end someday, though when exactly is unpredictable.

There are still enormous challenges in the country, particularly with regards to service delivery at the local government level. This was highlighted by an announcement by Clover, the dairy company that was once listed on the JSE, that it would close its Lichtenburg, North West cheese factory due to the collapse of municipal services and relocate it to Durban. With local government elections looming, it might just be the kind of crisis that forces political leaders in the provincial and national governments to finally respond to the dysfunction of the municipality and others like it.

Investment outlook

How does this impact asset classes? South African equities can be roughly grouped into three buckets, each with its own drivers. For mining companies, commodity prices matter most. However, operationally energy supply is important and local miners have been among the most vocal proponents of allowing own-generation. This is good news for them. For rand-hedge global consumer companies, domestic economic trends mean little, but a stronger currency can dent returns from the perspective of local investors. Recent news is rand positive, but the big move in the currency is probably behind us. For the third group of mainly domestically-focused companies such as banks, insurers, retailers, food producers, construction firms and logistics providers, a stronger local economy is unambiguously good news and supportive of their ability to grow earnings. These companies still trade at attractive valuations, since the market does not seem to have priced this in.

The story is similar for local listed property, where companies who operate in the UK and Eastern Europe are unaffected but the news for the domestically-focussed portfolios is positive. These firms are also very cheap, but property always lags the economic cycle because leases are normally in force for a number of years. Leases signed in a tenant’s market characterised by oversupply stay on books even when market conditions improve (and vice versa). Investors might therefore have to wait longer for their returns to materialise.

For money market and cash-plus products, stronger economic growth can put upward pressure on interest rates. The sooner the economy is judged to be close to operating at its full potential, the sooner the Reserve Bank will start raising interest rates from levels that are currently negative in real terms. However, the stronger rand – up 10% against the dollar since the start of the second quarter – reduces imported inflation and means that the repo rate should remain close to the current levels of 3.5% for some time.

Finally, for government bonds the news is also good. Bond yields reflect market views of where inflation and short-term interest rates are going, and these should serve as an anchor for longer-term yields. The reason the latter remain elevated is mainly due to concerns over high government debt levels (debt-to-GDP ratio), expected future borrowing (deficit-to-GDP ratio) and the ability and willingness to make interest payments on all this debt down the line.

A stronger economy means more tax revenue for government and a reduced need to borrow, lowering the numerator in the ratios. But a stronger economy, particularly a bigger nominal economy, means the denominator is bigger, further reducing the overall ratios. This is a bit technical, but high commodity prices push up the economy-wide inflation rate (the GDP deflator) which raises nominal GDP (real GDP plus inflation). In nominal terms, the economy was already larger than pre-pandemic levels in the first quarter.

Therefore, the deficit ratio should decline much faster than initially expected, substantially reducing the risk of a future default.

There is some risk that better revenue collection will allow the government to ease up on its fiscal consolidation plans, but in all likelihood it will stick broadly to them. However, until a public sector wage deal with minimal wage increases is signed, scepticism will remain high. South African bonds have long been pricing in a fiscal disaster scenario. But that scenario now seems avoidable, and bond prices can continue rising reflecting this.

The biggest risk to local bonds rather stems from abroad, specifically the US. If the high current inflation rate (US CPI was 5% year-on-year in May) proves to be sticking at current levels rather than a temporary result of base effects and reopening, it could put upward pressure on bond yields globally as investors price in central bank rate hikes. Emerging markets are typically susceptible to capital outflows in such a scenario. The good news on this front is that South Africa is currently running a current account surplus, reducing our need to attract foreign portfolio inflows. The current account surplus was a near-record 5% of GDP in the first quarter due to a 7% trade surplus, itself due to record high export prices. As imports continue recovering in line with domestic demand, the surplus should narrow but remain in positive territory for some time. In contrast, South Africa was running large current account deficits of between 7% and 3% between 2013 and 2018, when the US Federal Reserve started tightening its policy stance, putting pressure on the rand. Investors viewed it as a member of the ‘Fragile Five’ because of this.

In summary, the outlook for returns from local asset classes has certainly improved with the outlook for the domestic economy. After years of extreme pessimism over local prospects, the behavioural mistake would now be for sentiment to swing completely the other way. South African assets have strongly outperformed global equivalents in rand terms over the past year, but that doesn’t mean diversification should go out of the window now. Prudent portfolio construction means continuously spreading the risk around and casting the net wide in search of opportunities.