The elephants in the room

There is an old African proverb that says when two elephants fight, the grass suffers. US President Donald Trump and Federal Reserve Chair Jerome Powell are arguably the two most powerful men on earth, although for different reasons.

Their fight this year has, fortunately, not trampled markets underfoot. However, it offers a useful way to look at the US economy and what it means for investors.

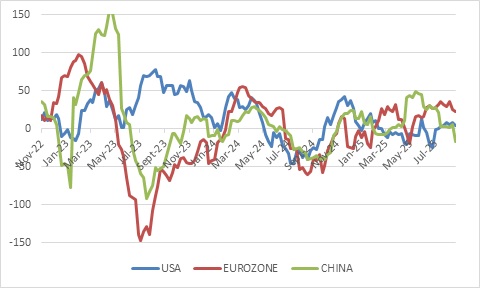

According to Trump, the US economy is experiencing a boom. “Under President Donald J. Trump’s bold pro-growth policies, American businesses are thriving like never before”, a recent White House press statement read. Even allowing for some poetic license, this is surely an exaggeration at a time when businesses in the US and abroad face extreme uncertainty. Having said that, economic activity remains surprisingly resilient compared to expectations that the wild policy swings this year would cause business activity to decline sharply. The indices in Chart 1 fall below zero when economic data disappoint relative to economists’ forecasts. The last few weeks the US and Eurozone indices have held up, though July data from China has pulled its index into negative territory.

Chart 1: Citigroup economic surprise indices

Source: LSEG Datastream

It helps that the US economy was in good shape heading into the year. Growth in consumer spending has slowed, but from a high level. However, it appears to increasingly be held up by wealthier households, who benefit from a rising stock market, among other things. Considering data points like credit card defaults, lower income household are feeling strain. It also helps that fiscal policy is very loose – i.e. the government is borrowing and spending freely, while tax cuts will also take effect next year. Some businesses also benefit from deregulation, but the US economy was not overregulated to begin with.

Under pressure

If the economy was in such great shape, why has Trump and his team argued so forcefully for lower interest rates? Trump has badgered Powell to urgently cut the fed funds rate. As he can’t legally fire the Fed chair, he has resorted to other forms of pressure. The latest is calls that a member of its board of governors should resign for allegedly cheating on a mortgage application.

At this point, it is probably not only about interest rates, but also about control and dominance. Nonetheless, Trump has said he wants lower borrowing costs to reduce the government’s interest burden. Despite the additional hundreds of billions that Trump’s import taxes will bring in, the federal government’s deficit looks set to keep rising. The problem of course is that the government doesn’t borrow at the fed funds rate, which is an overnight rate in the interbank market. The government borrows in bond markets, typically at longer maturities, and the market is still allowed to make up its own mind. The risks of high future inflation from a loss of Fed independence can put upward pressure on long-term bond yields, even if short-term interest rates are cut. Rising government debt levels are probably also leading to higher long-bond yields, even as the market prices in rate cuts.

Click here to read more...