The Economic Consequences of the Peace

The title of this article was also that of a famous 1919 book by the great John Maynard Keynes.

He argued that the Treaty of Versailles, which officially brought an end to World War I, imposed such economic hardship on Germany that a European financial collapse and another war were virtually inevitable. He would be proven catastrophically right on both counts. In contrast, the Memorandum of Understanding between the US and Iran – signed by US President Trump on Wednesday, also at the Palace of Versailles – is unambiguously good news for the world economy. However, it does little to salvage Trump’s reputation or American foreign policy credibility.

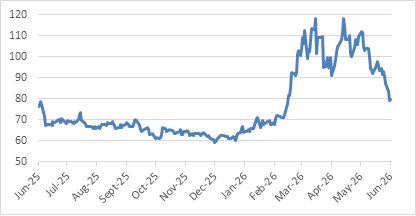

An MoU does not, of course, guarantee peace. Flare-ups and incidents remain likely in the 60-day period while both sides negotiate the thorny issues related to Iran’s nuclear programme. Indeed, the first roadblock was hit over weekend when Iran claimed to close the Strait of Hormuz again in response to ongoing fighting between Israel and Hezbollah. What lies beyond the 60-day period is also unknown. Nonetheless, reaching an MoU strongly suggests both the US and Iran want to put the war behind them. At any rate, markets didn’t wait for the finer details - they rarely do - and immediately started positioning for a post-war world which includes a gradual reopening of the Strait of Hormuz. In fact, this repositioning started weeks ago already, another reminder of how difficult it is to time the market. The upshot is that crude oil tumbled to $80 for the first time since March on Friday. This move might be a bit overdone given the uncertainties, but few will complain since the price is now well below the late April peak.

Chart 1: Brent crude oil price, $ per barrel

Source: LSEG Datastream

However, it is still higher than at the start of the year, squeezing household purchasing power and company margins. The relief won’t necessarily be felt immediately, just as the impact of higher prices wasn’t, as businesses don’t change orders, hiring or pricing plans overnight. In South Africa specifically, we’ll have to wait until next month for retail fuel prices to decline. Even then, the fall will be tempered by the fuel levy rising to its normal level. Still, petrol is on course to drop around R1.50 per litre and diesel by R3 per litre in the first week of July.

From an inflation point of view, the reported numbers are backward-looking. Most countries have only released May data, a period when oil prices averaged around $100. It is only by July that reported inflation will start looking better. However, because the oil price fell sharply during the second half of last year, there is unfavourable base for the remainder of this year, keeping inflation rates somewhat elevated. It’s important to remember that inflation always compares current prices with a period in the past, usually 12 months earlier.

Fighting the last war

This will still cause concern among central bankers who worry that inflation expectations could become unmoored, in other words, that households and businesses might believe that temporary inflation will become permanent. Central banks are often accused of fighting the last war. Put differently, they tend to be haunted by the last policy error made. Most underestimated the post-Covid inflation surge and waited too long to act. This time round, faced with elevated inflation, and the risk that price pressures broaden from fuel to other goods and services, several central banks increased interest rates. Others have adopted a wait-and-see attitude. Only time will tell which approach is right. For those that hiked, oil price relief will not lead to an immediate reversal of these changes, and indeed some central banks might choose to plough ahead with a few more hikes.

Among major central banks, last week saw the Bank of England, Swiss National Bank and Bank of Canada maintain interest rates, while the European Central Bank (ECB) and Bank of Japan hiked. The ECB lifted its policy rate from 2% to 2.25%. It is famously (or infamously) sensitive to energy prices, and hiked rates in response to higher oil prices on the eve of both the 2008 and 2011 crises. It was quickly forced to reverse those increases. However, with the European labour market being relatively tight, the risks of a wage-price spiral remain, and the market is pricing in another 25-basis point hike.

The Bank of Japan is on a very gradual path to exit two decades of near-zero interest rates. Even after last week’s hike, its policy rate is still only 1%. Arguably, it would have been hiking rates regardless of the Iran war, though with the yen still weak and Japan an energy importer, it was treading a fine line.

Warsh and Peace

The most important central bank remains the US Federal Reserve. Last week’s policy meeting was the first under the leadership of the new Chair, Kevin Warsh. He will have been particularly relieved to learn about the ceasefire, as it reduces the urgency to act. US inflation has been above the 2% target since early 2021 and has recently moved further away from the target.

Click here to read more...