The dogs that didn’t bark

• South Africa’s fiscal outlook has improved, helped by elevated commodity prices.

• While global bonds have sold off this year, local bonds have rallied.

• SONA placed the economy and private sector at its centre.

Ahead of next week’s annual Budget Speech, there is no shortage of things to be worried about. First and foremost, is the fact that the Speech will not be held in Parliament, which was seriously damaged in a fire recently. Following the July riots, this adds to the sense that the country is quite literarily burning and that the state has lost its ability to maintain law and order. If a prominent building in the middle of Cape Town cannot be protected, what hope is there of protecting critical infrastructure in outlying parts of the country? The Speech may also take place in darkness due to loadshedding which feels like another metaphor coming to life.

And yet, it is not all bad news. There are several positives. Or rather, negatives that have not materialised. Following the title of Sherlock Holmes’ story called Silver Blaze, written by Arthur Conan Doyle 130 years ago, we might call them the dogs that didn’t bark. (In the story, the fact that the watchdog didn’t bark signified that the intruder was not a stranger, but someone known to the dog.)

Tax rebound

Government’s tax revenue slumped in 2020 as the economy was locked down. At that point, recovery seemed a long way away. However, the rebound in tax revenues has been faster than expected since then. This trend has continued in recent months, and tax revenues are on course to exceed even the October Medium Term Budget Policy Statement (MTBPS) forecast.

In December, the latest month for which we have data, corporate tax revenues were 74% higher on a fiscal year-to-date basis compared to the same period in the previous year. This compares with a MTPBS projection of 43% largely thanks to the ongoing commodity price windfall. However, it is by no means purely a mining story. Personal income tax growth was also reasonably robust at 15% compared to the 11% projection.

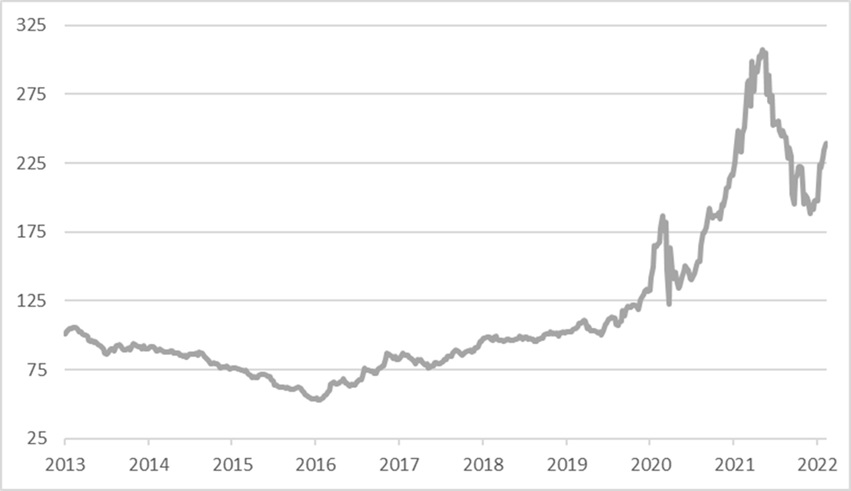

Chart 1: Price index of South Africa’s main commodity exports, $

Source: Refinitiv Datastream

This means that the budget deficit for the current financial year is likely to end up smaller than the 6.6% of GDP projected in the MTBPS, perhaps as much as a full percentage point. The deficit was a massive 9.9% in the previous fiscal year. The deficit – the difference between government spending and revenue that has to be financed by borrowing – remains unsustainably large in absolute terms but is at least moving in the right direction. Government debt levels (the cumulative impact of historical deficits) will only stabilise relative to national income by the middle of this decade and decline slightly thereafter, and that is only if everything goes according to plan.

There is no doubt that South Africa’s fiscal situation is bleak, but it is not hopeless. Importantly, the risk that the government will default on its debt – the ultimate fear of any bondholder - is still small. What matters is not just the size of the debt load, but its composition. For any household, business or government, debt is inherently riskier if there is a mismatch in maturity (funding long-term assets with short-term debt) or currency (funding hard currency debt with local currency income).

While the South African government’s total amount of debt is large, the structure of debt is well managed by National Treasury with clear limits on how much is borrowed in hard currency (currently 10%), and how much is borrowed in short-term bonds versus less risky (from the point of view of the borrower) long-term bonds.

Going the opposite way

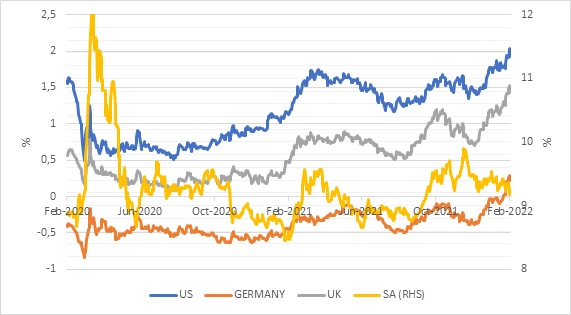

The big story on global markets this year has been rising interest rates amid elevated global inflation. Data released last week saw US consumer inflation hitting 7.5%, the highest level in over 40 years. The market now expects the US Federal Reserve to hike six or seven times this year, up from three not too long ago. Even the European Central Bank is now expected to raise its policy rate towards the end of the year. As a result, the US 10-year Treasury bond yield increased to 2% for the first time since mid-2019 though it is still low in absolute terms (rising yields means falling bond prices). Germany’s equivalent is back above 0%. Shorter-dated yields have increased even faster, with US 2-year Treasury yields rising close to a percentage point to 1.6% in the past three months, reflecting the rapid repricing of interest rate expectations.

Chart 2: 10-year government bond yields in local currency

Source: Refinitiv Datastream

Strikingly, however, South African long bond yields have declined since the start of the year. The 10-year government bond yield firmed from 9.4% to 9.2%. The decline is modest, and the yield is still high in absolute terms, but the fact that it declined while US yields have increased so dramatically is encouraging.

The rand has also been remarkably stable in the face of global market turmoil this year. Clearly bonds and the currency are helped by firm global commodity prices and the better fiscal outlook discussed above.

But lower bond yields probably also reflect the fact that the medium to longer-term local inflation outlook remains muted, which gives investors a hefty real yield on a current and prospective basis. In contrast, the US 10-year bond yield is negative in real terms if you assume low inflation over the next decade, and it is deeply negative if you think that current high inflation will persist.

The South African Reserve Bank has been hiking rates, with more rate increases expected. This is reflected in shorter dated yields rising, but the weighted basket of government bond yields as reflected in the All Bond Index is lower, not higher this year. This is a huge relief, not only because it means positive returns for investors (in dollars, South African bonds have outperformed global bonds by 11% this year), but because interest costs are a large and growing portion of government spending.

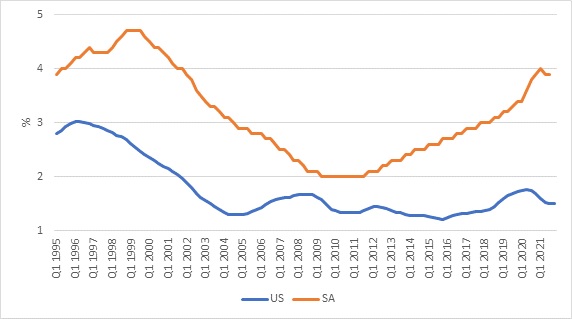

In fact, it is the fastest growing item in the Budget, and will eventually be the largest, mainly because of high interest rates. The US government, for instance, has a much higher debt-to-GDP ratio than South Africa’s (120% vs 70%), but the former can borrow at lower interest rates and therefore spends only 1.5% of national income on interest payments, compared to 4% (and rising) for South Africa.

Chart 3: Government interest payments as % of GDP

Source: Refinitiv Datastream

Modest progress

Thirdly, as much as if it feels as if the country is going to the dogs, there is slow but steady progress in economic structural reform.

In that regard, last week’s State of the Nation Address placed the economy at centre of the speech, and rightly so. As Harvard economist Dani Rodrik once said of South Africa, if we don’t solve our unemployment crisis, it doesn’t really matter which other problems we solve. Focusing purely on economic policy, SONA was better than expected (it was rather disappointing on matters relating to law enforcement).

The only solution is to make it easier and cheaper to do business in South Africa. Companies that are profitable expand, invest and hire. Companies that aren’t, don’t. The government’s focus should be on allowing business to flourish. This will not only create jobs, but also generate the tax revenues to fund social grants, public education, health care and so on.

The penny seems to be finally dropping. The President emphasised, probably for the first time in public, that governments don’t create jobs, businesses do. Up to now, government has always placed itself in the centre of economic development, unfortunately barking up the wrong tree. The more government focuses on creating an enabling environment for the private sector while limiting its own direct involvement in the economy, the better the chance of meaningful growth and job creation.

He highlighted steps to cut red tape, including the appointment of a “red tape czar” (as the Americans would call it) in the form of former Exxaro CEO Sipho Nkosi. There is also excessive red tape at all levels of government, while the failure to adequately deliver basic services like roads, water, and policing drives up the cost of doing business. In the end, it is the poor that suffer most.

The biggest culprits are state-owned enterprises that have virtual monopolies on transport and energy but fail to deliver, thereby holding the rest of the economy hostage. Therefore, reforms in the energy sector are critical. Eskom is being unbundled into three separate units for generation, transmission and distribution. Almost 10,000MW of electricity from government’s various independent power producer programmes will come on stream in the next few years. In parallel to this process, companies can now generate their own electricity up to 100MW and certain municipalities can also source electricity from independent producers.

Another key reform in the works is Transnet allowing private players access to some of its railways and port terminals. A third and much-delayed change, auctioning spectrum to allow for faster and cheaper broadband is set to take place in March after years of delay.

As always, the SONA is heavy on promises of things to be done and light on things that have actually been delivered. The phrase “we will soon finalise” is a favourite that rings a bit hollow by now. But all these slow and small steps will add up over time.

Worse than its bite

Amid such concerns of chaos and decay and giving record unemployment and the hammering the ruling party took at last year’s municipal election (as well as the upcoming intra-party leadership contest), a shift to populist policies might be expected. But remarkably, populism’s bark is still worse than its bite in this country.

As emphasised in SONA, the government remains committed to gradually reducing its deficit, even though it is never a popular thing to do. It might even have to raise personal and value-added tax rates at some point in the coming years to do so.

One specific example is the debate around the introduction of a basic income grant, which has been conducted mostly in very pragmatic terms of what can be afforded and what the associated benefits and costs will be.

In simple terms, the country can afford to provide an extended social safety net that will blunt the impact of the desperate poverty many of our compatriots have to face. But we cannot afford to do so in the current budget framework on a sustained basis. Wisely, the commodity windfall is not expected to last and therefore government knows that increased social spending will have to be accommodated by cutting spending elsewhere (reprioritising) or raising taxes. As the President noted, “Any future support must pass the test of affordability and must not come at the expense of basic services or at the risk of unsustainable spending.” Until that is figured out, the R350 per month Social Relief of Distress grant, extended for another year to March 2023, is likely to remain in place.

The investor’s perspective

Finally, a point worth repeating. The list of problems in South Africa is long and the political will to fix them seems to be in short supply. Covid only worsened things. However, returns from South African investments have been pretty good over the past two years. The link between the South African economy, its politics and returns enjoyed (or not) by local investors is not as straightforward as many assumed. Where there have been spectacular implosions, it is mostly due to corporate governance failures (Steinhoff), inept capital allocation (Woolworths) or excessive debt (SA listed property), and not because of the macro environment.

It is early days, but in 2022 South African bonds and equities have outperformed global counterparts in dollars, helped along by a firmer currency. Anyone who took all their money offshore is missing out on the diversification benefits of having both local and global investments. The expected widespread collapse of South African asset prices is therefore another dog that didn’t bark.