The Cost of the Energy Crisis

According to the law of energy conservation, energy cannot be created or destroyed. It can only be converted from one form or another. Similarly, it seems, the current energy crisis is shifting in nature, without going away.

Going global

A few months ago, the energy crunch was truly global in nature. Since almost everyone needs to use a vehicle at some point, whether a luxury SUV, tuk-tuk or even a rickety rural bus service, the surge in oil prices over the past year caused universal pain. The oil price was rising even before Russia’s invasion of Ukraine, as the world economy reopened from 2020’s lockdown, going from $50 to $80 per barrel during 2021. But the war caused oil prices to spike to as high as $130 in early March 2022. This resulted in higher retail fuel prices across the world. In the case of the US, the land of the large vehicle, petrol (gasoline) prices hit $5 per gallon for the first time ever, as high oil prices were compounded by record refining costs (crack spreads).

Today the oil price is back to pre-war level, around $100 per barrel. The worst-case scenarios in terms of supply disruptions have not materialised while investors are increasingly concerned about the negative impact on oil demand as the global economy slows. As a result, the US gasoline price is back below $4, a 20% decline from the peak. Similarly, South Africa’s petrol price is likely to fall by more than R2 per litre next week.

A continental sized problem

However, the energy crisis persists elsewhere, notably in Europe. Natural gas flows from Russia have slowed to a trickle, ostensibly because of pipeline maintenance, though probably due to Russia weaponising gas supplies to inflict maximum pain on European consumers and reduce their willingness to continue supporting Ukraine’s war effort.

The big difference between oil and natural gas is that the former can easily be loaded onto a ship and transported to almost any market. Indeed, while some countries refused to import Russian oil, others like India and China have been eager to capitalise on lower prices. Even Saudi Arabia has imported Russian oil for domestic use, leaving more of its own production available for export.

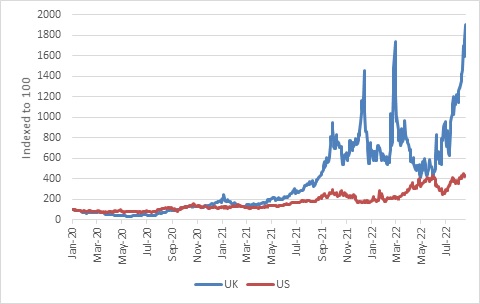

Chart 1: Natural gas prices in the UK and US

Source: Refinitiv Datastream

But gas needs to be liquefied before it can be shipped, and then re-gasified on arrival. This is costly and requires specialised infrastructure that is lacking in many European countries. Piping natural gas is much cheaper and more convenient, except if your main source turns out to be your enemy. Therefore, while Europe has ramped up imports of liquified natural gas (LNG), particularly from the US, it is not able to import as much as it would like to because the infrastructure is not yet adequate. This explains the wide differential between European and American natural gas prices: American gas cannot flow freely to Europe to benefit from higher prices there as financial arbitrage is prevented by physical obstacles. It also means, of course, that other countries, notably in Asia, have to compete with Europe for gas imports. Recently a $1 billion gas import tender by Pakistan failed as no suppliers made any bids. It a tight market, suppliers would rather sell to countries with a better credit rating.

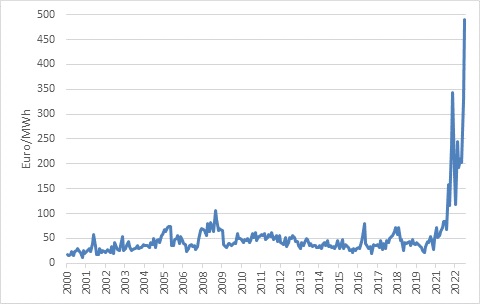

Apart from gas, Europe has the additional problem of a major drought that is wreaking havoc with hydroelectricity production in countries like Norway, while some French nuclear plants have had to cut back output because of river temperatures. In Germany, the drought is impeding the transport of coal on river barges.

Chart 2: Wholesale spot electricity price in Germany

Source: European Energy Exchange

The net result is an epic surge in electricity prices and inflation rates. German producer inflation hit a record 37% year-on-year in July, and August is unlikely to have been any better. In the UK, consumer inflation hit 10%, with economists forecasting a peak of between 15% and 19% next year.

In other words, while US inflation rates have probably peaked, the same is not true across the Atlantic. US Federal Reserve chair Jerome Powell on Friday reiterated that rates would still have to rise and probably remain high to make sure inflation returns to the 2% target. This spooked markets, but at least US inflation seems to be trending lower and will relieve some of the pressure on households and business. Central banks in Europe will also have to continue to raise rates even as the cost of living crisis intensifies and underlying economic activity comes under further pressure.

South Africans are by now used to electricity supply constraints, as well as rapidly rising prices. But the process of adaptation is only now getting underway in Europe. There is little doubt that with enough time and money, it can wean itself of Russian supplies, but there is likely to be severe economic pain until then, with a recession likely.

This is one of the main reasons the euro has fallen back to parity against the US dollar.

Heatwave

It is not just in Europe where drought is playing havoc with electricity production. A record two-month long heatwave has gripped China and many rivers have dried up, including some parts of the Yangtze, the country’s longest river. This has drastically reduced hydroelectric production at a time when extreme heat has led to a surge in demand for electricity. The result has been widespread loadshedding and at a time when sporadic zero-Covid lockdowns are already disrupting activity in the world’s number two economy. Crops are also at risk if the weather doesn’t turn more favourable soon.

Other emerging markets face not just high energy prices, but also the compounding impact of a strong dollar. Energy importers are particularly hard hit, having to pay high dollar oil and gas prices at weaker exchange rates. This can lead to severe balance of payments problems if the country cannot earn enough hard currency to pay for fuel imports. The same is true, unfortunately, of food prices.

In fact, there is a strong correlation between food and energy prices, since energy is a key input into food production. Moreover, the widespread use of ethanol in petrol, particularly in the US, means rising fuel prices tend to drag maize prices higher.

Many developing countries also subsidise fuel prices for consumers, though the numbers have shrunk over the years. Though well-meaning, fuel subsidies mean that at times of high global prices governments face a worsening fiscal situation along with a deteriorating balance of payments. It also means that consumers aren’t incentivised to cut back, in other words prices can’t do their usual job of balancing supply and demand. Inevitably, the government has to face reality and cut the subsidy which leads to a massive jump in fuel prices and widespread unhappiness. Governments have fallen over this issue, with Argentina’s reformist president Macri coming to mind, being voted out in 2019 (and he tried removing subsidies at a time when fuel prices were not nearly as high as today).

South Africa’s benefit

On this score, South Africa’s situation compares well. Fuel prices are regulated, but there is no subsidy that can blow up the budget. The recent fuel levy relief was explicitly temporary and has already expired. Moreover, South Africa earns more than enough hard currency to cover imports of fuel.

The big benefit SA has in the current moment is being a major coal exporter. Coal prices have jumped as utilities have increased demand in the face of rocketing gas prices. High coal prices mean South African export values remain near record levels, and higher than import values. Unfortunately, South Africa has not been able to increase coal export volumes due to Transnet’s inefficiencies. Nonetheless, the fiscus has benefited greatly from higher tax revenues, and the rand has been much more resilient against the dollar than it would have been otherwise. This in turn means that inflation and interest rates are lower. Of course, it helps greatly that we are not reliant on gas.

While consumer inflation at 7.8% in July is nobody’s idea of a picnic, it is still on the low end compared to many other countries, while core inflation remains relatively muted at 4.6%.

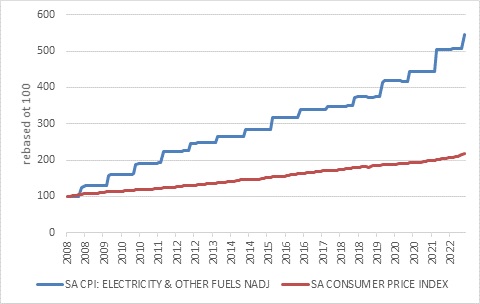

South Africa does have an energy crisis, however, and it is largely home-grown: loadshedding. The recent high global fuel prices have undoubtedly hurt South African consumers, but the lack of reliable electricity supply has been a chronic constraint on economic growth for many years. This year has been by far the worst. On top of that, electricity prices have increased much faster than the overall consumer price index, though electricity is still quite small in the consumer price index with a 3.7% weight. Importantly, since Eskom largely buys coal on long-term contracts from local mines, it is not as exposed to the current surge in global spot coal prices as utilities elsewhere are. It is, however, exposed to diesel prices for the peaking plants it operates.

Chart 3: SA electricity CPI versus headline CPI

Source: Stats SA

Light at the end of the tunnel

Fortunately, there is hope. In true South African fashion, it required a major crisis to effect change, but we are now finally at the early stages of an energy revolution. Private companies and households will be allowed to produce as much electricity as they want for own use, while selling surplus electricity to the grid. The government-run independent renewable energy power producer programme is also being scaled up substantially. Eskom’s monopoly is being dismantled, and not a moment too soon as it will struggle by itself to keep the lights on, given the advanced age of its coal-fired power plants and all its other well-documented internal problems.

Implications

There are at least three things for investors to consider.

Firstly, the root cause of the current energy crisis is arguably the lack of investment over the previous decade, including reduced investment in fossil fuel extraction. Capex spending by listed oil and gas companies has fallen back to 2008 levels. While this is partly due to ESG-related pressures, it also reflects poor returns from the sector over the past decade. Sustained higher prices might be needed to induce increased capital spending by these companies. Government policies are also likely to focus a lot more on energy security. The world will need to invest much more in energy production and storage in the coming years while at the same time shifting the mix of energy sources form fossil fuels to renewables. Indeed, the heatwaves that are compounding the current energy crunch in Europe and China are a warning of how climate change can severely impact economic life. The upshot is that all this spending will be someone else’s income.

Secondly, while some elements of the current energy crisis are temporary, particularly the weather-related ones, other elements could be longer-lasting. For instance, while the oil price tends to decline as the global economy slows, tight supplies mean it could also rise again quickly as the economy starts rebounding. This could lead to more volatile inflation cycles than we’ve had in the past, complicating life for investors and central banks.

Thirdly, when a rubber band is pulled to far, it is bound to snap back. Looking beyond the energy sector itself, one should ask which areas are currently depressed and have the opportunity to rebound once conditions normalise. European large cap equities, for instance, are trading at a near record discount to American stocks. There might be good reasons for this, as outlined above, but the best opportunities usually arise when investors get carried away.

As much as humans like to believe we have tamed nature, we are still extremely dependent on the weather playing along. And even as our economies become increasingly based on digital services, the simple fact remains we are extremely reliant on energy in all facets of economic activity. Even the metaverse won’t work if someone doesn’t keep the servers plugged in. Energy security has not been on the forefront over the past decade or so and was largely taken for granted. This is no longer the case.