The classic behavioural mistake – trying to time the market

Financial markets without volatility would be unnatural, like an ocean without waves. Markets are constantly churning, and the degree of market volatility varies from small ripples to rolling waves or a financial crisis-sized tsunami.

Big swings in asset prices in either direction will happen from time to time. It is not necessarily a cause for panic. The more volatile markets are said to be, the wider and more regular prices fluctuate. Many investors are uncomfortable with the large vacillations inherent in a volatile investment and thus shun this risk – and potentially higher returns. Instead, they look for more stable investments with predictable but possibly lower returns. Avoiding the risk most likely leaves returns on the table and may result in investors not meeting their financial goals.

How to respond to market volatility

It might sound counter-intuitive, but during periods of market volatility, the correct course of action might be to take no action. This is difficult to do because volatility can leave investors feeling vulnerable and concerned that they have to react. Investors who jump ship after a “big wave” may break the cardinal rule of investing by “selling low”. Consider this – if you own a home whose value went down this year, would you panic and sell your home? Most likely, you would not. You bought your house because you knew it would be there a while, so its day-to-day price movement is not as important. The chances are that the value of your home will rise over time, and that is what you are focused on.

Market timing has its cost

One of the highest market-timing costs is being out when the market unexpectedly surges upward, potentially missing some of the best-performing moments. For example, believing the market would go down, an investor sells off equities and places the proceeds in more conservative investments. Instead, the market enjoys a high-performing period while the money is out of equities. Therefore, the investor incorrectly timed the market and missed those top-performing months.

This table illustrates the potential results from poor market-timing compared with buying and holding. The three columns represent the growth of a $1 000 investment in the S&P 500 Index beginning in 1991, 2001, and 2011 respectively and ending on 31 December 2020.

Source: https://www.merrilledge.com /ChartSource®, DST Retirement Solutions, LLC

The results clearly show the benefit of staying invested. Missing some of the best months in the stock market will significantly impact the value of your investment over the longer term.

Taking a long-term view is important

Here are three reasons why having a longer-time horizon is worth considering:

• It is virtually impossible to predict precisely when the top or bottom of a market will be.

• When investors try to “time the market”, they risk buying high and selling low.

• Bad timing can further exacerbate the losses experienced during volatile times, which is why investors would typically be better off staying the course.

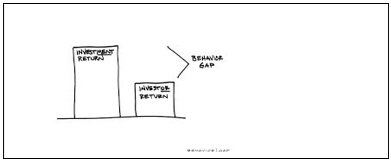

The most apparent evidence is that investment returns and investor returns are almost always different. You earn an investment return if you invest your money and then do not touch it. No buying, no selling, just holding. But real people rarely invest this way. Real people chase performance and invest by looking in the rear-view mirror. The search for the best investment creates a phenomenon called “The Behaviour Gap”, a phrase coined by author Carl Richards. Because of classic behavioural mistakes, average investors almost always do worse than average investments – such as an index like the JSE All Share Index.

Be disciplined

Many investors may have made money by timing the market correctly – predicting market movements and selling or buying shares accordingly – but this was likely due more to luck than skill. For the average investor, the challenge is not to make decisions marked by emotion.

We know that markets do not move up in a straight line and that volatility is inherent in all asset classes. Checking a portfolio too frequently can make investors more susceptible to loss aversion since the probability of seeing a loss in a short period is much greater than over extended periods. True long-term investors are more willing to allocate towards risky assets because they do not care about the short-term ups and downs.

Time is your ally

Although growth assets – such as equity and property – have underperformed lately, growth assets classes have outperformed less volatile asset classes such as money market and income solutions over the long term. High-income funds as classified by the Association for Savings and Investment South Africa returned an annualised 10.7% between 1 July 2000 and 30 June 2022, for instance, compared with 9.6% for a low-equity investment, according to data compiled by Morningstar.

It is imperative to begin your financial-advice process with a clear idea of your client's goals and the time frame needed to accomplish them. Once you do this, it should become clear that the goal is not to “beat the market” but to reach or exceed personal goals. Only then should you assess how your client’s investments performed against the broader market, how this fits into their long-term plans, whether modifications are needed, the costs of switching, pros, cons and risks, and the knowledge that things change. It’s a paradigm shift away from being obsessed with immediate outperformance to being future- focused and riding the waves along the way.

INN8 Invest is a division of STANLIB Wealth Management (Pty) Ltd, an authorised Financial Services Provider, with licence number 590 under the Financial Advisory and Intermediary Services Act (FAIS).