The behavioural gap

What is the cost of responding to your emotions in investing?

We are often our own worst enemy.

This adage is especially true when it comes to investing, as behaviour can be one of the leading causes of investors not reaching their goals.

This is the view of Saleem Sonday, head of Retail Distribution at Allan Gray, who says one of the mistakes many investors make is switching between funds or making withdrawals in an emotional response to short-term market movements.

“Investors are often tempted to sell out of a unit trust that is doing poorly and invest in another that is doing better in an attempt to improve their returns. This is particularly prevalent during times of uncertainty, like we are currently experiencing, when the temptation to move to safety is heightened. But this can erode returns,” says Sonday.

This is illustrated in Graph 1, which shows behaviour and resultant returns in three hypothetical investment scenarios. In all the scenarios, Allan Gray measured the performance of a R100?000 investment initiated in January 2020 over the period to December 2022.

The first scenario represents the investor who stayed invested in the Allan Gray Balanced Fund over the entire period. The second scenario represents an investment in the Allan Gray Money Market Fund over the duration of the period, and the third represents the investor who attempted to time the market and made multiple switches between the funds in reaction to market volatility, which was driven by the start of the pandemic in March 2020 and Russia’s invasion of Ukraine in late February last year.

“The difference in outcomes is notable,” says Sonday.

He says that although measured over a relatively short period of time compared to the average long-term investment horizon, Graph 1 reinforces the point that you will likely earn higher returns by remaining consistently invested over time, whether it is in a low- or medium-risk investment.

“Staying invested allows you to reap the rewards of compound interest – gaining additional returns on the returns already earned from your investments over time. By selling off investments or switching between funds, we limit the compounding effect and growth potential of our investments. We also prevent ourselves from benefiting from any turnaround when it comes.”

He says that this type of behaviour and outcome is very common. Economists call it the “behaviour gap”, which refers to the difference between the long-term returns delivered by a fund and the return an individual investor earns; a gap widened by poor behaviour, particularly trying to time the perfect entrance to and exit from the market (which often leads to buying high and selling low).

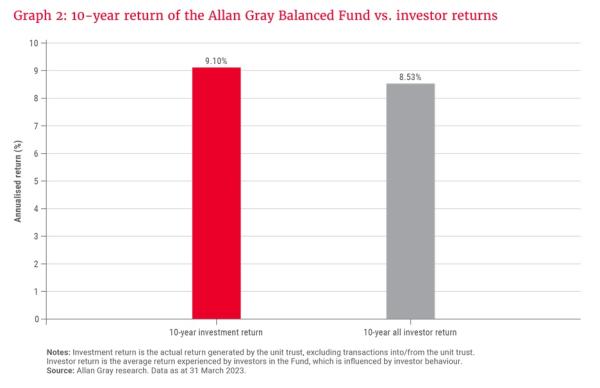

Graph 2 shows the 10-year return of the Allan Gray Balanced Fund – which is the return an investor would earn over the period by staying invested – compared to Allan Gray clients’ investment returns.

“It highlights that, on average, our clients locked in a 0.57% investor behaviour penalty over the period. That may not seem like a big difference, but over time, these small differences compound and can have a significant impact.”

He says that key to enjoying long-term investing success is ensuring that investors keep emotions in check and remain invested. Admittedly, this is easier said than done, in the face of dips in the market and negative sentiment.

“Market volatility is part of investing. Your role as an investor is to pick a unit trust on the basis that it suits your needs and objectives and that you can trust the fund manager – not merely on account of recent performance. And if you can control your emotions, and hold on to that investment through the volatility, you give yourself a better chance of enjoying returns over the long term. Only switch if your goals or needs have changed,” concludes Sonday.