The 60 000-foot view

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

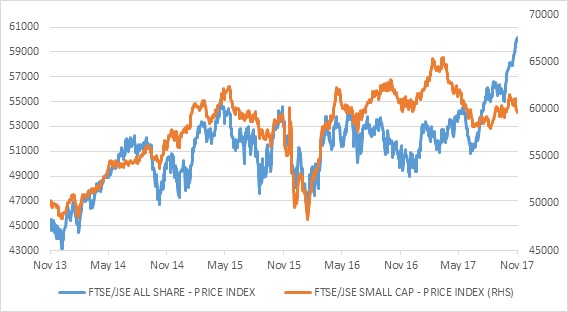

The FTSE/JSE All Share Index, or Alsi as it is widely known, broke through the 60 000 points mark for the first time last week. The Alsi beat its previous record high of 55 188 points (set three years earlier in April 2015) in July.

Is this significant? Yes and no. Humans like round numbers for some reason, and 60 000 is therefore a fairly arbitrary level to celebrate. However, this level reflects price movements only. There is a separate total return index that measures the Alsi with dividends included. This index predictably runs ahead and sets new records well before the price index, since it benefits from compound growth. Also, since the market trends up over time (but never in a straight line), it will obviously set fresh record highs as it goes along. Finally, the index is not adjusted for inflation while investors should ideally think in terms of real returns.

What is significant is that the massive rally since mid-June came without any substantial improvement in domestic political and economic conditions, and after a three-year period of moving sideways. In fact, political uncertainty seems to be increasing the closer we get to the ANC’s December elective conference. The October Medium Term Budget signalled a move away from fiscal consolidation and arguably did further harm to business and consumer confidence, increasing the risk of further credit ratings downgrades. Investors who sat on the side-lines hoping for some clarity on these matters – or who “sold in May and went away” - have missed out, illustrating the extreme difficulty of a market-timing approach. No one could have predicted it, and unfortunately, if you miss out on rallies such as this the long-term return from equities is mediocre. In contrast, maintaining market exposure through the course of a volatile year has been rewarding.

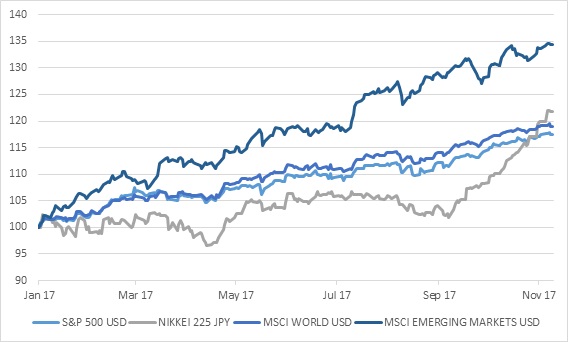

Global factors have been driving the market, and global equities have enjoyed a strong run over the past 20 months, while the JSE was late to the party in some respects. The JSE certainly lags the MSCI Emerging Markets Index, which also outperformed developed markets in US dollar terms this year, rallying 31%. The US S&P 500 is up 15% this year and the tech-heavy NASDAQ up 25% in dollars. The German DAX is up 18% in euros and the Nikkei 225 16% in yen.

The other big five

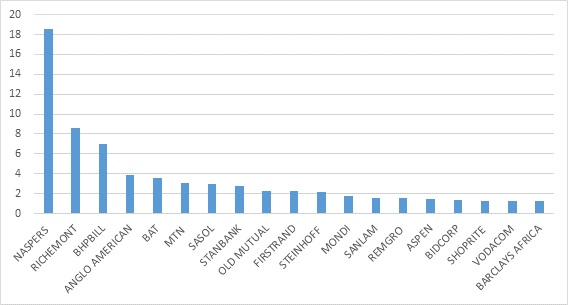

The five biggest companies on the Alsi (accounting for 41% of the index) are all global companies in the sense that only a very small percentage of their revenues are from South Africa (Naspers, Richemont, British American Tobacco) or mining companies dependent on global commodity prices (BHP Billiton and Anglo American). Naspers alone accounts for 19% of the Alsi and has surged an incredible 76% this year due to its stake in the booming Chinese internet giant Tencent. US tech companies have been rallying this year and the so-called FAANG stocks (Facebook, Apple, Amazon, Netflix and Google) have outperformed the S&P 500 by 25% this year. Chinese tech titans Tencent and Alibaba have doubled this year, while Baidu and JD.com are up around 50%. Although all these tech companies trade on very high valuations, they are also generating surging earnings growth with positive cash flows, which is very different to most companies during the 1990s dotcom bubble.

Commodity prices are firmer this year as optimism over global growth has increased and some commodities are running into supply constraints. Aided by a softer rand, this boosted resources shares on the JSE. Palladium is up 48% this year (but platinum is only marginally positive as demand for diesel vehicles has come under some pressure). Aluminium is up 22% and copper 25% (all in US dollars). The gold price has gained and the iron ore price has been the laggard.

Without these global giants - whose prices are set in international markets - the Alsi’s return would have been much lower. The Top 40 Index has returned 25% this year but the mid-cap and small-cap indices are flat. Many - but not all - companies focused on the weak local economy struggling. Clothing retailers are down 5% this year and food producers are flat, but banks are up 7%, while food and drug retailers have gained 19%. It is also not the case that all the global giants are performing well. Steinhoff is down 20% and AB InBev (which acquired SABMiller and is not a member of the Alsi due to its small free float in the local market) is down 10%.

The massive size of Naspers creates a headache for active managers since it is virtually impossible to be overweight even if they have a positive outlook. Index-trackers have therefore beaten active equity managers this year, but are at risk of a huge exposure to a single share.

Local increasingly global

For local investors worried about political uncertainty and the future of the country in general, it is therefore worth remembering that JSE-listed equity and property companies are increasingly internationalising, and therefore exposure to the local economy in a typical balanced fund is declining, offering a natural hedge against an unwelcome surprise in December.

However, it is also possible to sketch a scenario where the rand strengthens if a low global interest rate backdrop coincides with rising commodity prices, greater investor enthusiasm over emerging markets and a positive outcome in December. Therefore, appropriate diversification calls for some exposure to assets that do well in a strong rand environment too. SA government bonds would be one example where yields are currently high as the market digests the likelihood of further ratings downgrades in the coming weeks (S&P and Moody’s are scheduled to make announcements on 24 November). Suggestions that free higher education might be forced through have accelerated the sell-off in bonds and, along with Turkey, and a lesser extent Brazil, our bond yields have risen sharply over the past month.

Will it last?

The final question is: will the rally on markets last? Unfortunately, nobody knows if it will, but it certainly can. The global environment is favourable to equities with good growth, low inflation and the expectation of very gradual interest rate increases in the developed markets. As a result, earnings growth has picked up across markets.

It is very unusual for equity markets to run ahead for long periods of time without experiencing a correction of a few percent. These cannot be foreseen though. A big bear market will probably require a substantial downgrade in market expectations of economic growth (i.e. a looming recession) or a change in the expected path of monetary policy. Neither seem likely now, and in fact the global economy appears to be picking up steam only now after a long period of subpar growth. All the major economies are growing together for the first time in a decade. As long as inflation remains well-behaved, there is no reason for central banks to hike interest rates aggressively. Big bear markets on the JSE have historically coincided with substantial downturns in global markets, rather than local conditions. So instead of only focusing on local politics, also keep your eyes on international developments.

Chart 1: FTSE/JSE All Share and Small Cap indices

Source: Datastream

Chart 2: Major global equity indices in local currency, rebased to 100

Source: Datastream

Chart 3: Weights of the largest shares in the FTSE/JSE All Share Index, %

Source: Statpro