The 2017 investment landscape

Tony Cadle, Fund Manager at Ashburton Investments.

Last year most global equity markets reported single digit returns. The shining light however, was the US equity market where the S&P500 reported a positive return of 12%. In contrast, the FTSE 100 reported a decline of 0.2% in dollar terms, while both the German Dax 30 and French Cac 40 made gains of 3.3% and 5.7% respectively.

Emerging markets did report double digit dollar returns of 11.6% based upon a rebound in commodity prices and strengthening currencies. In local currency terms, the South African FTSE/JSE ALL Share Index produced a below inflation return of 2.63% and the rand-hedge biased Top 40 Index a negative return of -1.52%. The latter negative return resulted from a strengthening rand.

So what is the investment outlook for 2017?

Political uncertainty in the developed world may well continue throughout 2017. The wave of anti-establishment protests have already been demonstrated through the Brexit vote, the election of Donald Trump as the US President and the resignation of Prime Minister Matteo Renzi of Italy following a failed constitutional reform initiative. If anti-establishment views continue to prevail, elections in March in the Netherlands, April/May in France and September/October in Germany may well see changes in government. The question to ask is; will these potential changes in governments be negative or positive for equity markets?

The initial view of a Trump Presidency in the US appears positive for equity markets with his pro-business stance towards taxes, infrastructure spend and lack of concern towards climate change. Trump has indicated his intention to reduce corporate taxes from 35% to 15%. Should these tax cuts be enacted, corporate profits for those companies with a 35% corporate tax rate could increase materially. The ramifications of greater corporate profits are stimulatory in that business confidence increases, creating opportunities for greater capex spend which in turn stimulates greater employment. Moreover, President Trump has announced a $1 trillion infrastructure programme over a 10 year period to spur economic growth and create jobs. Despite the hurdles to be negotiated, the implementation of the infrastructure programme would be positive for economic growth and be supportive of corporate earnings. President Trump has also questioned the validity of climate change and vowed to save the coal industry. Furthermore, he intends reviewing legislation weighing on the coal sector and the oil industry and end US participation in international climate agreements. Thus the fossil fuel industry should benefit from a Trump Presidency.

The commodity producing emerging market economies have been under pressure due to the five year decline in commodity prices which bottomed in January 2016. Since then commodity prices have risen due to supply side discipline in production, short term dollar weakness and renewed fiscal stimulus in China. Oil should also benefit from supply side constraints effective 1 January 2017. OPEC has announced the organisation is to decrease oil production by 1.2 mbbl/day to 32.5 mbbl/day and Russia has announced its intention to cut output by 300,000bbl/day in the first half of 2017. These developments, if enacted, should support the oil price and lend support to commodity prices. Moreover, should current commodity prices prevail over the course of 2017, acceleration in emerging market GDP growth may well take place, underpinning equity market earnings growth.

Has the 30 year bull market in developed market bonds come to an end? On the 8th July 2016 the US ten-year bond yield declined to 1.38% which may reflect the 30 year low in the bond yield. Low bond yields have been driven down in part by thirty years of globalisation allowing excess savings and global capital flows to drive down interest rates. This coupled with post global financial crisis quantitative easing and austerity measures added further downward pressure on inflation and bond yields. This investment regime appears to be changing as the public backlash to these policies becomes evident. An era of nationalism, interventionist government policies potentially leading to higher inflation and interest rates appears to be unfolding. Should these developments occur traditional “safe haven bonds” are likely to offer inferior returns as bond yields slowly increase in the coming years. Under this investment scenario investors should favour bonds with short duration.

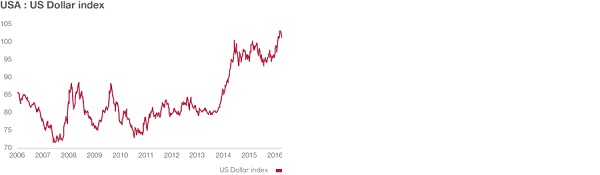

Another important investment decision to make in 2017 is to formulate a view on US dollar strength or weakness. On 3rd January this year, the US dollar index attained its highest level since 2002 at 103.66. In March 2008 the index bottomed at 71, thus the past nine years has seen a 46% strengthening of the index. Presently, investment opinion still favours a strong dollar due to Trump’s pro-business tax initiatives and fiscal stimulus programme. However, should his initiatives not lead to accelerated economic growth the US dollar could be vulnerable to a period of weakness.

Source: I Net BFA

From a South African perspective the lacklustre economy should slowly accelerate over the coming year, supported by higher commodity prices and declining inflation. Many economists are forecasting GDP growth at just over 1% for 2017. The country avoided a rating downgrade to “junk status” in December however, a June “junk status” rating is still a probability should economic growth remain at current low levels. Inflation is at or around peak levels at present due to the base effect of the low oil price a year ago. Inflation should drift lower as maize and wheat production recovers from the 2015/2016 drought. If the inflation rate reduces significantly, the possibility of an interest rate reduction would be supportive of interest-rate sensitive shares.

Compared to 2016 the investment landscape for 2017 appears more positive for growth assets with the expectation of a year-on-year acceleration in global GDP and a switch in economic policy, led by the United States, away from monetary to fiscal policy stimulus. While these developments should be broadly supportive of equity markets, a rising tide of protectionism, rising inflation and rising interest rates could cause some valuation headwinds. This environment would also have a moderating effect on developed market bond returns. Once again, as in 2016, the correct rand view will be an important factor in determining equity market performance.