Talking Bull

Believe it or not, we are halfway through the year. Also somewhat unbelievable is that there is talk of a new equity bull market being underway. Could it be, given all the uncertainties and macro headwinds?

Bull markets are always born in fear and doubt and grow up climbing a wall of worry. There are always pessimists who say markets are rising too far, too fast. In that sense, the recent rally is completely consistent with past bull markets. The market is forward-looking and does not wait for the economy to bottom out. It rather anticipates the profits companies will generate when the upswing is eventually underway.

Where the current episode is different to past early bull markets is that the recession has not happened yet, at least not in the US, the largest and most important economy. Importantly, central banks are still hiking interest rates.

Economists have been warning about a recession for many months now, so it is possible that the market has discounted it and is moving on, focusing on the post-recession recovery. But that would ascribe a far-sightedness to the market that it normally lacks. Its ability to look forward is usually counted in months, not years. The fact that rates remain high is not trivial. One of the reasons the economy and the equity market can usually quickly recover from a down cycle is that these are associated with a much lower cost of borrowing.

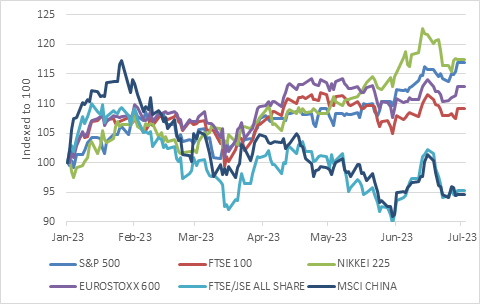

Chart 1: 2023 equity performance, US dollars

Source: Refinitiv Datastream

At any rate, markets have not entirely moved up in unison. For the first six months of the year, the US S&P 500 returned 14%, but it is up 23% from its October 2022 low, hence crossing the rather arbitrary 20% bull market threshold. The Japanese Nikkei 225 has been even livelier this year gaining 27% in yen and 17% in dollars, while the Eurostoxx 600 has returned 9% in euros. Meanwhile, the UK FTSE 100 has returned only 2% this year. Even further behind, Chinese equities are in negative territory in dollar terms year-to-date.

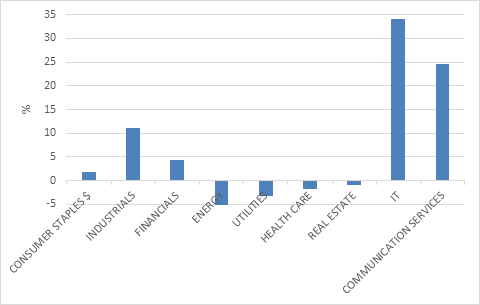

There is also a wide sector dispersion, as chart 2 shows. Artificial Intelligence (AI) excitement has driven IT and Communication Services shares higher, or rather, has driven a few heavy-weights in each sector higher. Other sectors are flat to negative for the year.

Chart 2: MSCI All Country World Index 2023 sector returns, US dollars

Source: Refinitiv Datastream

In contrast to perky equity markets, the Bloomberg Global Aggregate Bond Index is down -0.6% in 2023 to date, after 2022’s record 16% decline. The lacklustre rebound from a historic slump reflects the fact that the bond market is still digesting higher rates, while the equity market is already moving on. The benchmark US 10-year bond yield has moved sideways this year, at 3.8%, but the more policy-sensitive two-year yield has increased from 4.5% to 4.8%. When shorter-dated yields are higher than long-dated yields, there is a so-called inversion of the yield curve. Historically, an inversion of the US yield curve has preceded recessions, though with varying lags.

The equity market is shrugging off recession fears, or at least the headline indices are, reflecting a soft-landing scenario where inflation subsides sufficiently for central banks to start cutting rates while the current resilience of the global economy, particularly the US, means this might happen without a recession. The problem is that the current resilience is precisely what makes it unlikely that inflation will cooperate.

I can’t get no traction

Clearly, interest rates have not had much traction yet, despite rising faster and higher than at any point in the past for decades. There are three broad reasons for that.

Firstly, as we’ve often pointed out, interest rates work with a lag. Consumers and firms adjust to gradually rising borrowing costs, until they cannot anymore. How quickly the breaking point arrives will depend on a number of factors, including debt levels. US household debt has declined over the past few years, and therefore the household sector is not as vulnerable to higher rates as is the case in Canada or Australia, where debt levels surged in line with booming property sectors.

Secondly, there are a number of pandemic-related distortions that make this cycle different form the past. Now, we all know that “this time is different” are the four most dangerous words in finance, and these distortions won’t last forever. But for now, they are making things different. This includes the massive pot of excess savings, which in the US, various estimates put at between $500 billion and $1 trillion. It is also large in Europe and other developed countries. It also includes the fact that the two most important interest-rate sensitive sectors, housing and vehicle sales, saw supply disruptions. For cars, it was the case of the missing microchips, as global semi-conductor shortages saw prices of new and used cars jump. This is already a thing of the past. In the case of housing, the supply of existing homes on the market in the US has largely dried up as few homeowners want to swap a low pre-2022 mortgage for a high 2023 vintage. As a result, new home construction is picking up again. This is very unusual given where mortgage rates are.

Thirdly, interest rates in many countries are still negative in real terms. A very rough rule of thumb is that interest rates are only truly restrictive when they are positive in real terms. Each economy theoretically has a ‘neutral’ real interest rate where supply and demand are nicely balanced and there is no inflation. This rate is unobservable in practice. You cannot measure it, only its effects on credit growth, inflation and so on. Still, the Fed estimates that this neutral real rate for the US economy is 0.5%. Depending on what inflation measure you use, the Fed only crossed this barrier a few months ago.

Or as Fed chair Jerome Powell told the audience at the annual ECB conference in Sintra, Portugal, last week: “Although policy is restrictive, it may not be restrictive enough and it has not been restrictive for long enough.” The message from other central bank chiefs was similar, Christine Lagarde from the ECB and Andrew Bailey from the Bank of England also agreed. Even the new Bank of Japan governor, Kazuo Ueda said high inflation and accelerating wage growth, meant it was time to start considering moving away from decades of long loose and ultra-loose monetary policy.

In other words, the equity market’s cheeriness stands in contrast to the stated intention of central banks to slow their respective economies to cool inflation. Either the market has not been listening, or more likely, doesn’t believe central banks will follow through.

Back home, the JSE ended the first half of the year positive in rands but in the red in dollar terms. There is definitely no excessive cheer here, though economic news has been a bit better than feared recently.

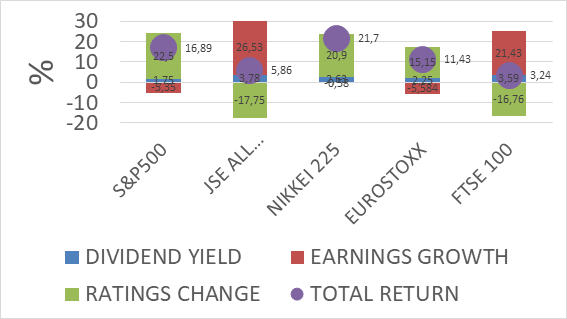

Chart 3 decomposes this year’s equity returns for selected global indices into dividends, earnings growth and the change in the price: earnings multiple. It is notable that returns for the S&P 500 come entirely from a re-rating (increase in the PE multiple) with negative earnings growth, while the JSE has de-rated with positive earnings growth. The PE multiple for the US is above its long-term average, meaning the market is on the expensive side, while for the JSE it is below the long-term average. Ditto for Japan and the UK, while Eurostoxx valuation is close to average.

Chart 3: Local currency year-to-date return decomposition, %

Source: Refinitiv Datastream

Of bulls and bears

To come back to the original question, is this a bull or a bear market rally? We’ll only know with hindsight, unfortunately. Some ingredients of past bull markets are in place, others are definitely not. These things are largely unpredictable. Economies are giant complex systems with millions of moving parts influenced by the decisions of emotional human beings. Financial markets are equally complex and similarly influenced by the decisions of millions of people prone to all manners of behavioural biases. Another layer of complexity is the interplay between the real economy and financial market, with feedback loops in both directions.

There is a plausible scenario where we are indeed in the early innings of a bull market as markets look past a soft patch in the world economy and price in a rosier future. There is also a very reasonable scenario that the global economy, including the US, experiences a sharp growth slowdown or recession in the next year that is not fully discounted in the equity market, perhaps because central banks are forced to hike rates further than current anticipated.

And in truth there is always uncertainty. It is easy to look back to the past and think that history followed a predetermined and obvious path, but at every point, there were always multiple realistic outcomes. The crazy events in Russia last weekend show how quickly things can change, and then change again.

There are questions we can ask to navigate uncertainty. Am I being adequately compensated for the risk I am taking on? In equity investing, there is always risk. But does the potential upside justify taking on the risk? A different way of asking the same question is to ask whether the risks are fully priced in. And if I don’t want to take on the risk, what is the cost of being defensive, of keeping some powder dry? It can be very costly to miss out of the early stages of a bull market sitting in cash, especially when interest rate cuts reduce the returns from cash. For instance, when global markets started rallying in April 2020 after the Covid-crash, money market funds were yielding roughly 0.5% in the US and 4% in South Africa. Today the numbers are 5% and 8% respectively. It is a very different picture.

Fortunately, we don’t have to bet the farm on whether there will or won’t be a global recession or whether the bull market is for real or, well, bull. Diversification across asset classes and regions remains a powerful tool when faced with these unknowns, while valuations remain an important guide.